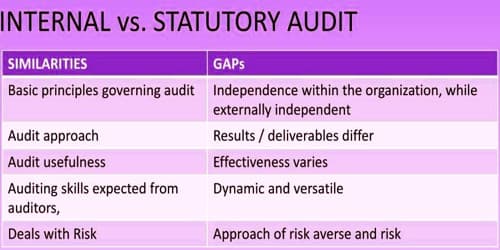

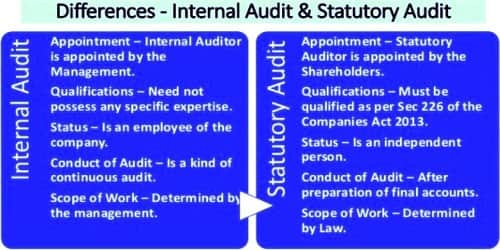

Differences between Internal Audit and Statutory Audit

An internal audit refers to an ongoing audit function performed within an organization by a separate internal auditing department. It is conducted by the permanent staff of the same office to detect weakness in system, procedures and for the improvement. But statutory audit is an audit function performed by the independent body which is not a part of the organization. It is the act of checking books of accounts as per the provision of company act. Remuneration of the internal auditor is fixed by the management while for the statutory auditor the remuneration is fixed by the shareholders.

Both of them checkbooks of account detect errors and frauds even though they have certain differences which are as follows:

- Objective

Internal Audit reviews the routine activities and provides a suggestion for the improvement. Statutory Audit analyze and verify the financial statement of the company.

- Appointment

Internal Audit Report is submitted to the management. However, the External Audit Report is handed over to the stakeholders like shareholders, debenture holders, creditors, suppliers, government, etc.

- Opinion

Internal Audit provides an opinion on the effectiveness of operational activities of the organization. On the other hand, the External Audit gives an opinion of the true and fair view of the financial statement.

- Qualification

An internal auditor does not require specific qualification as per the provision of law but the qualification of statutory auditor is specified. form example, Internal auditor need not possess the qualification as are laid down under section 226 o the companies act while a statutory auditor must have those qualifications.

- Scope of Work

The scope of work by the internal auditor is determined by the management while the scope of the work and responsibilities of the statutory auditor are determined by law.

- Remuneration

An internal auditor is appointed by the management, so remuneration is fixed by the management but remuneration of statutory auditor is fixed by the shareholders. So, Remuneration of the internal auditor is fixed by the management while for the statutory auditor the remuneration is fixed by the shareholders.

- Duration

Internal Audit is a continuous process while the External Audit is conducted on a yearly basis.

Information Source: