Deferred compensation applies to the portion of one’s contribution at a future date that is postponed and compensated. It is an agreement in which a percentage of the salary of an employee is paid out at a later date after the income has been received. The taxes on this salary are postponed in most situations before it is paid out. Types of conceded pay in corporate retirement plans, benefits plans, and investment opportunity plans. Retirement plans and representative annuities are instances of conceded pay. Employers normally withhold a percentage of the wages of workers each month, collect it over time, and pay the lump sum balance on a date previously agreed in the contract of employment.

As it offers future tax benefits, an employee may opt for deferred compensation. In most situations, before payment of the bonus, income tax is postponed, usually until the employee retires. In view of the fact that the compensation is received at a later date, the sum withheld for payment is not included in the computing levy. Subsequently, it decreases the measure of available pay in the current year. Notwithstanding, the essential measure of duty is deducted at the time the worker gets this installment. Although “deferred compensation” is theoretically any system under which an employee earns salaries after receiving them, the more common usage of the term applies to “non-qualified” deferred compensation and a particular section of the tax code that provides chief executives and other highly paid corporate workers with a special gain.

As a rule, the personal expense is conceded until the pay is paid out, generally when the representative resigns. On the off chance that the worker hopes to be in a lower charge section subsequent to resigning than when they at first acquired the remuneration, they get an opportunity to lessen their taxation rate. Deferred compensation is a contractual arrangement between an employer and an employee where the employee willingly decides to have part of their compensation deferred, invested on their behalf by the company and offered to them in the future at some pre-specified stage. Since the remuneration is paid sometime in the not too distant future, the sum conceded for installment is excluded while processing the charge. Hence, it lessens the measure of available pay in the current year.

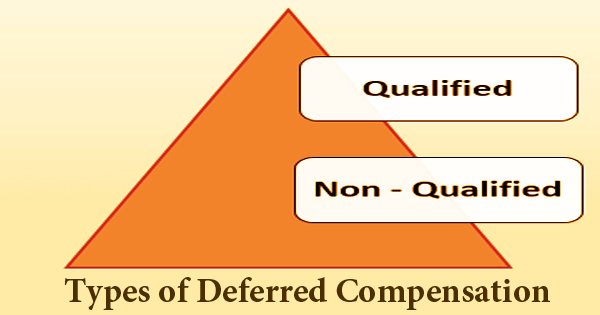

There are two different types of deferred compensation: eligible and unqualified. These differ greatly in their legal treatment, and from the viewpoint of an employer, the position they represent. Often deferred compensation is used to refer to unskilled plans, but both are legally encompassed by the term.

Qualified Deferred Compensation: The Employee Retirement Income Security Act (ERISA), which was acquainted with guarantee assurance to retirement resources, sets the standards for qualified conceded pay. Under such principles, workers reserve an option to full data about their retirement designs liberated from cost. The legislation requires the retention of employee retirement savings in a trust account. All workers must be given the plans, and they are for an employee’s sole benefit. It ensures that in the event the company fails to pay its obligations, creditors will not demand the funds. The 401(k) and 403(b) programs provide some examples of eligible deferred compensation. ERISA also restricts the amount of money that can be deposited into a qualified plan. For example, the 401(k) plan limits the contribution of employees into the pension account at $19,500.

In general, eligible deferred compensation programs are regulated by more stringent regulations, as the ERISA also sets out the minimum requirements to be met by an employee in order to apply for the scheme and provides detailed rules on how employers can provide appropriate funding for the scheme.

Non-Qualifying Deferred Compensation: Non-qualified conceded compensation (NQDC) plans, otherwise called 409(a) plans and “brilliant binds,” give managers an approach to draw in and hold particularly significant workers, since they don’t need to be offered to all representatives and have no covers on commitments. Furthermore, for NQDC plans, independent contractors are liable. For certain firms, they provide a way to attract costly talent without actually having to pay their full salary, which means they can delay funding these commitments. However, the plan may be a gamble.

Plans are generally set up either in line with chiefs or as a motivator by the Board of Directors. They’re drafted by legal advisors, recorded in the Board minutes with boundaries characterized. Workers account for their checks by allowances, and they will likewise get their rewards. Employers choose to have an investment return fixed or to invest the money in the desired fund of the employee. The deferred compensation arrangements offer members the following benefits:

- Security after retirement: Deferred compensation plans provide persons with a guaranteed income after they retire. Financial security is provided by the money earned from retirement programs. In order to gain interest income, beneficiaries can also invest their money in mutual funds or other investment options later.

- Tax benefits: The part of one’s earnings withheld for payment on a future date decreases current earnings and is not charged until payment is obtained by the receiver. Individuals who plan to fall under a lower income tax bracket will benefit immensely from the system in the future. Also, on the off chance that future assessment rates fall in the country, recipients of conceded pay plans will, at last, make good on less in expenses.

- Capital gains: The funds deposited in deferred compensation accounts are invested by several workers in mutual funds or other stable investment strategies that provide steady interest payments. Daily payments of interest add to the value of the post-retirement payout. Furthermore, if the value of the investment increases over time, the recipient is therefore obliged to make capital gains.

The vast majority of the arrangements around conceded compare identified with conditions the worker controls, (for example, intentional end), anyway conceded comp regularly has a provision that says on account of the representative’s passing or lasting inability, the arrangement will promptly vest and the worker (or home) can get the cash. When the employee retires, compensation is usually paid out, but payment may also begin on a set date, upon a change of the company’s ownership, or due to injury, death, or a (strictly defined) emergency. Deferred payments could be maintained by the employer depending on the terms of the contract whether the employee is dismissed, defects to a competitor, or otherwise forfeits the profit.

Information Sources: