Bank credit is an important catalyst for bringing about economic development in a country because without adequate finance, there can be no growth or maintenance of a stable economy. Prime Bank Ltd. provides different types of credit facilities to its customers like Overdraft (against work order), Cash Credit (Hypothecation), Cash credit (Pledge), Loan Against Trust Receipt (LTR), Loan Against Imported Merchandise(LIM), Demand Draft Purchase(DDP), IBP(Inland Bill Purchase), Consumer Credit Scheme, Small and Medium Enterprise Credit Scheme, House Building/ Apartment Loan Scheme, Lease Finance, Hire Purchase in the main spring of the credit operation and also some special loan schemes. Day by day the bank is extending its credit operation remarkably. The credit of the bank increased by Tk. 18094 million during 2010 registering a growth of 42.46 percent against the previous year. Through its credit operation Prime Bank is playing a vital role in the micro and macro economic development of Bangladesh.

The Credit Operations Department will primarily service the lending teams in Shanghai and also serve as the repository of best practices and act as a consultant to all branches for any queries they may have on credit operations matters. These include ensuring effective delivery of credit services and products to customers, monitoring credit limits, providing proper mechanism for document tracking and capturing and maintaining credit-related information in the recording systems.

OBJECTIVES OF THE REPORT:

The main objective of the study is to analysis the credit operations of Prime Bank Limited.

To achieve this, the following are the specific objectives:

- To identify different services of Credit operation in Prime Bank Limited.

- To identify different Type of Loans and its amounts.

- To know about the Credit operation functions of Prime Bank Limited.

METHODOLOGY OF THE REPORT:

Research Design:

Exploratory research has been conducted for gathering better information that will give a better understanding on credit department. Both primary and secondary sources of data collection procedure have been used in the report. Primary data has been collected mainly through the writer’s observation of the approval process and monitoring techniques, informal interviews of executives, officers and employees of Prime Bank Limited.

Sources of Data Collection

To make the Report more meaningful and presentable, two sources of data and information have been used widely.

The “Primary sources” are as follows

* Face-to-face conversation with the respective officers and staffs of Prime Bank.

* Informal conversation with the clients.

* Practical work exposures from the different desks of the departments of the department.

* Study of the relevant files as instructed as instructed by the officers concerned.

The “Secondary Sources” of data and information are–

* Annual reports of PBL and other Banks.

* Training materials available at the Internet.

LIMITATIONS OF THE STUDY

The limitations of the study are as follows:

i) The credit policies and manuals of PBL are of confidential nature and thus it is difficult to collect the necessary literature and documents within this short time.

ii) The bank officials though helpful in every respect do not have much time to explain the internal procedures.

iii) Many operations relating to the credit extension run simultaneously by different credit officials and it is difficult to capture the sequence of any particular credit proposal.

iv) A structured filing procedure is often neglected which also poses difficulty in understanding the sequential procedure.

v) Borrowers do not often have the time to cooperate in the information gathering process.

Evolution of the Word ‘Bank’:

The word bank is originated from Italian word ‘Banca’. Banca means long tool. In ancient time Italian Jews merchant used to do business of lending money by sitting on the tools. To meet the expense of war of 1171 one type credit certificate was launched in Italy at an interest rate of 5% which was called as Monte in Italian language and Banke in German language. Then the German language was widely used in Italy. As a result the word ‘Banke’ gradually changed to the word ‘Banca’ from which the word ‘Bank’ originated.

Walkway of Banking:

The linguistics and etymology suggest an interesting story about banking origins. Both the old French word ‘Banque’ and the Italian word ‘Banca’ were used centuries ago to mean a bench or moneychangers table. The historians have identified the first bankers who lived more than 2000 years ago. They were money changers seated usually at tables or in a small shop in the commercial district, aiding travellers who came to the town by exchanging foreign coins for local money or discounting commercial notes for a fee in order to supply merchants with working capital.

The first bankers probably used their own capital to fund their activities but it was not long before the idea of attracting deposit and securing temporary loans from wealthy customers. Loans were then made to merchants’ shippers and landowners at rates of interests low as 6 percent per annum to as high as 48 percent a month for the riskiest ventures. Most of the early bank was Greek in origin.

The banking industry gradually spread outward from the classical civilizations of Greece and Rome into northern and western Europe. The early bank in Europe was placed for safe keeping of valuable items (such as gold and silver bullion) as people came to fear the loss of their asset due to war, theft, or expropriation by government. When colonies were established in North and South America, the old world banking practice was transferred to the new world.

Development of Bank in Bangladesh:

Bank system was practiced in Indian subcontinent by the Indian subcontinent merchants; Goldsmith Moneylenders were the primary bankers. During the mughal period banking and credit business was enchanted rapidly.

Indigenous banking in Bangladesh is as old as banking in other parts of the world. During mughal period, indigenous banking flourished. The Subarna Banik, the bullion trading community used to do banking in the then Bengal.

Banking in Bangladesh was gradually taken over by the upcountry bankers who were known as Seth, Shah etc. But Subarna Banik continued to operate in rural Bengal. The British gradually came to Bengal and operated banking in the form of agency house and exchanging houses started to flourish in Calcutta. Entry of the Bengalese into banking started in the part of this century especially in the period of the Swadeshi movement.

In 1700 AD “Hindustan bank” was established as the first joint stock bank. In 1784 “Bengal bank” and in 1786 “general bank of India “were launched. Then both the banks absolved respectively in 1793 and 1832.

During the early period of nineteenth century the three banks “Bank of Bombay”, “Bank of Madras” and “Bank of Bengal” merged to “Imperial bank of India”.

In 1947 after the separation of Bengal, bank business faced a severe disaster as non-Muslim bankers migrated to India. In order to rebuild the bank business State bank of Pakistan was established as a central bank of Pakistan in 1948.

In 1971 Bangladesh became independent. After liberation ‘Bangladesh bank’ was automated with the assets and liabilities of former “State bank of Pakistan

Background of Prime Bank Limited:

The Prime Bank Limited (PBL) is a national banking group that is incorporated on February 12, 1995 as a consequence of persistent efforts of a group of entrepreneurs having excellence of experience exposure in the different fields of industry, trade and commerce of the country. It started operation as a commercial bank on April 17, 1995 with a branch at Motijheel. At present, the bank has 110 branches spread all over the country. It renders all types of commercial banking services to the customers of all strata in the society within the stipulations laid down the bank company act 1991 and rules and regulations formed by Bangladesh Government from time to time. Diversification of products and services and innovation of products suited to the needs of the customers in keeping with relevant rules and laws have made it different from other commercial banks of the country.

PBL’s national business in personal banking, corporate banking and its markets are its special strengths. It maintains correspondent relationship with all over the banks in countries. Prime Bank Limited is a forward looking and modern local bank with a record of sound performance. It is discarding its erstwhile conservative mould and in response to the current dynamic trends in locally financial activities, adopting an aggressive customer focused system. The effort that Prime Bank makes in order to portray the bank as a brand image is very strong and successful. The general image is that it is “trustworthy, efficient, helpful and committed”. The logo of the bank depicts the merger of confidence.

Prime Bank Ltd. has already made significant progress within a very short period of its existences. The bank has been graded as a top class bank in the country through internationally accepted CAMEL rating. The bank made satisfactory progress in all areas of business operation in 2010.

Prime Bank Limited was designed to provide commercial and investment banking services to all types of customer ranging from small entrepreneur to big business firms. Besides investment in trade and commerce, the bank participates in the socioeconomic development through the participation in priority sectors like agriculture, industry, housing, and self-employment. Prime Bank Limited wants to establish, maintain, and conduct all types of banking, investments and businesses in Bangladesh and abroad with superior service quality and performance.

General Statement of Prime Bank Ltd.:

Prime Bank Ltd. has pursued pragmatic policies and strategies depending on the prevailing business scenario. It focuses on the emerging needs of the market and has positioned itself accordingly. High quality customer service through competent workforce remains uppermost in Prime Bank’s thinking and action plan. Integration of technology in business functions is an important strategy for PBL (Prime Bank Ltd.) to attain opportunities and to provide value-added services to the customers.

Prime Bank Ltd. has had consistent growth over the years. Management of PBL has put in place the necessary business initiatives, which are to ensure success as Prime Bank Ltd. moves towards the new millennium. Its guiding principles are rendering of service to customers more efficiently and effectively than other competitors, concentrating on core business and building self-strengths. Customer services of Prime Bank Ltd. are acknowledged to be one of the best in the industry and for this high quality Prime Bank Ltd. is rated as a top-performing bank.

Prime Bank Ltd. has planned to improve its customer services further through diversity in products and services. Offering customers a variety of options to fulfill their banking needs will remain an important component of PBL’s long-term business plans. Exercise will continue to reform the systems and to develop back-office support capabilities. Management has decided to focus more on small and medium sized enterprises by providing a broad range of financial options. PBL has further deepened its stack in retail banking by introducing new products. Efforts in Merchant banking are further intensified to generate more profits as Prime Bank Ltd. has acquired Merchant-banking license.

Prime Bank Ltd. is able to remain competitive and enjoyed continued growth, which in some extent depends on financial sector reforms of the government. Prime Bank Ltd. is in complete agreement with Bangladesh Bank’s plans to review and to asses thoroughly the financial sector and to set the future framework for the industry. Prime Bank Ltd. is willing to support all constructive reforms that are in the national interest and encourage more competition and choice for the people. This Bank always stays tuned to the realities of rapidly changing markets.

Management of PBL strongly believes that this bank will grow and prosper in the days to come. Ongoing researches to innovate products and to fine-tune the existing products will lead to advantageous position. MasterCard credit cards business and newly introduced ONLINE banking have opened up new possibilities not only for improved customer service but several windows for profit generation. Installation of SWIFT and integration of treasury functions in both local money market and international foreign exchange market are expected to yield better growth in volume and earnings.

While banking is undergoing changes to accommodate increasing needs of customers, technology is considered as a key element for achieving competency based on reliability. PBL is working to further improve its computer system in order to provide clients with new IT products and services such as ATM, Online Banking and Point of Sales transactions. From PBL’s perspective, Technology will help Prime Bank Ltd. to operate more efficiently and improve its productivity. Therefore, investment in technology infrastructure receives highest priority. While technology takes care of much of the routine functions, employees will have more time to spend with their customers providing greater range of advice and services.

At present Prime Bank Ltd. has a small network of branches and therefore manages these branches in a manner, which maximizes profit and brings added values for shareholders.

Goals & Objectives of Prime Bank Ltd.

- To build up strong pillar of capital.

- To promote trade, commerce and industry.

- To discover strategies for achieving systematic growth.

- To improve and broaden the range of product and services.

- To develop human resource by increasing employment opportunities.

- To enhance asset of shareholders.

- To offer standard financial services to the people.

- To create congenial atmosphere so that the clients become interested to deal in with the prime bank limited.

- To keep business morality.

- To develop welfare oriented banking service.

- To offer highest possible benefit to customers.

- To let the viewers cast their very first look at it.

- To carry on the business of discounting and dealing in exchange of securities and all kinds of mercantile banking.

- To provide for safe-deposit vaults and the safe custody of valuables of all kinds.

- To carry on business as financiers, promoters, capitalists, financial and monitory agents, concessionaires and brokers.

- To act as agents for sale and purchase of any stock, shares or securities or for any other monetary or mercantile transaction.

- To establish and open offices and branches to carry on all or any of the business abroad and within the country.

Operation:

Prime Bank Limited, since its inception, is a fully focused Bank depending on technology. The bank has now a network of 52 branches strategically located in different cities. All the branches are functioning in computerized environment and integrated through Wide Area Network (WAN) .The branches are full-fledged units and can provide all commercial and investment banking service ranging from small and medium enterprises to big conglomerates and houses.

The Bank will try to reduce its dependence on interest earnings by giving more emphasis on the fee-based income through introduction of capital market operation and leasing. The Capital Market operation will include Portfolio Management, Investors Account, and Underwriting Mutual Fund Management etc.

The Bank will introduce modern system of Leasing Operation same as in practice with Banks in all other countries of the world. The lease finance portfolio of the bank will be the first of its kind in a Commercial Bank in Bangladesh.

A warehousing system will be developed in the country through private entrepreneurs. The conventional go down system of the Banks will gradually be done and a modern system of warehousing will be encouraged for pledge of goods of the clients. Investment Counsellors of PBL will give all sorts of advice to their Customers as they may require from time to time for protecting their assets and safeguard to their interest.

Entrepreneurship Development Training will be arranged to impart operational skill and modern technique of management to introduce new entrepreneurs in the field of industrialization on the basis of participating finance.

Prime Bank Limited is one of first few Bangladeshi Banks who have become members of SWIFT (Society for Worldwide Inter-Bank Financial Telecommunication) in 1999. SWIFT is a member owned co-operative which provides a fast and accurate communication network for financial transactions such as letters of credit, fund transfer etc. By becoming a member of SWIFT, the bank has opened up possibilities for uninterrupted connectivity with over 8,700 user institutions in 160 countries around the world.

Prime Bank Limited is operating branches on both conformist interest based Banking and Islamic Sariah Principle based Banking. The Islamic Sariah Principle Banking is completely different from the conventional banking.

The Bank is Maintaining separate set of accounts for Islamic Banking branches according to the standard adopted by financial Accounting and Auditing organization for Islamic Financial Institution.

Prime Bank Training Institute (PBTI) was set up in July 22, 1998 with an aim to create a strong and skilled work force.

The Institute had played a significant role in making skilled and efficient human resource. It is constantly working on improvement of training methods and materials. During 2010 it had conducted 4 Foundation Training Courses, 4 short, courses, and 24 workshops for new recruits, junior level management, mid level management, and senior executives. The Training Institute also provided a Foundation course for 30 trainee officers of Jamuna Bank Limited at their cost.

Prime Bank Limited will try to achieve excellence in customer service. The customer is most important for them. Their policy is customer driven. The Bank will introduce Inland Travellers Cheque and launch Special Savings Schemes; Special Credit Scheme will also be devised for the benefit of the low-income group, especially for the self -employment of the educated youth.

Mission and vision of Prime Bank Limited:

The efforts of Prime bank Limited are focused on delivery of quality service in all areas of banking activities with the aim to add increased value to shareholders’ investment and offer highest possible benefits to the customers. There must have the mission as well as vision what should back every efforts of the organization as it is said, “A mission without any vision is a daydream and a vision without any mission is a nightmare”.

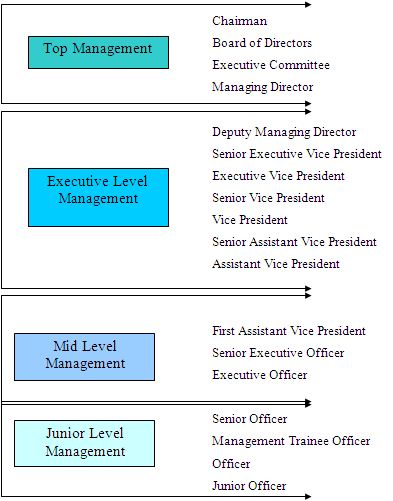

Managerial Hierarchy of PBL:

Products & Services of Prime Bank Ltd.

Since commencement of banking operation, prime bank Limited has not only gained enormous popularity but also been successful in mobilizing deposit and loan products. The bank has made significant progress within a very short time period due to its dynamic management and introduction of various consumer-friendly loan and deposit products. All the products and services offered by the bank can be classified under three major heads:

i) Multi Currency Account

ii) Deposit Products:

- Contributory Savings Scheme

- Monthly Benefit Deposit Scheme

- Special Deposit Scheme

- Education Savings Scheme

- Fixed Deposit Scheme

- Prime Bank Money Scheme

- Prime Bank Insured Fixed Deposit Scheme

- Saving Deposit Account

- STD Account

- Foreign Currency Deposit Account

- Non Resident Taka Account

- NFCD Account

- NITA

iii) Loan Products:

- Consumers’ Credit Scheme

- Lease Finance

- Hire Purchase

- Small and Medium Enterprise Credit Scheme

- Loan Against Shares and Securities

- House Building Financing Scheme

- Financing Scheme For Contractors

- Computer Software Financing Scheme

- Prime Bank Maser Card Credit Card

- Prime Bank VISA Credit Card

- Working Capital Financing

- Import Financing

- Export Financing

- Industrial Financing

Other Services:

Consistent with the modern edge and competing in a perfectly competitive market, Prime Bank Limited has introduced some innovative banking services that are remarkable in a country like Bangladesh. The services offered by the bank are as follows

On-line Banking:

The bank has set up Wide Area Network (WAN) across the country within its all branches to provide on-line branch banking facility to tits valued customers. The service named “PRIMELINE” has opened up several possibilities of improved customer services. Under this facility client of one branch are able to do banking transaction at any other branch of the bank. The bank hosted its Web Site. to facilitate dissemination of information about the banking services and facilities of Prime Bank Limited all over the world.

Information Technology in Banking Operation:

Prime Bank Limited has adopted automation in banking operation from the first day of its business. The main objective of this automation is to provide efficient and prompt services to its valued clients. At present all the branches of the bank are computerized under UNIX operating system to provide best security to the information. Prime Bank Limited is providing comprehensive range of banking services with utmost care and efficiency to its customers. ATM is used to count money properly to save client’s valuable time as well. The customer can draw money/cash from their account within a minute. Very recently the bank has launched the world famous banking software T24 which is very user friendly. It will no doubt help the bank to attain the objectives more efficiently.

SWIFT Service:

Prime Bank Limited is one of the first few Bangladeshi Banks to obtain membership of SWIFT (Society for Worldwide Inter-bank Telecommunication). SWIFT is a members’ owned cooperative which provide a first and accurate communication network for financial transactions such as Letter of Credit, Fund Transfer etc. By being a member of SWIFT, the bank has opened up possibilities for uninterrupted connectivity with over 8700 user institutions in 160 countries all over the world.

Loans or credits comprise the most important asset as well as the primary source of earning for the banking institutions. On the other hand, loan/credit is also the major source of risk for the bank management. A prudent bank management should always try to make an appropriate balance between its return and risk involved with the loan portfolio. Credit appraisal process is the tool which helps the bank to predict the risk and return on the proposed project for credit disbursement. Therefore, from the above definition it is clear that credit appraisal is a very important factor for banks. To get a clear idea about credit appraisal process, we need to know the key factors of credit appraisal procedures. In this chapter, we will have a brief idea on the key factors of standard credit appraisal procedures.

Credit:

The word credit is derived from the Latin word “credo” which means “I believe” and is usually defined as the ability to buy with a promise to pay. It consists of actual transfer and delivery of goods and services in exchange for a promise to pay in future. It is simply the opposite of debt. Diversification of banking service has accelerated the use of credit in the expansion of business operation. It is a fundamental precept of banking everywhere that advances are made to customers in reliance on his promise to pay rather than the security held by the banker.

According to the Encyclopaedia of Banking & Finance by Charles J. Woelfel, Bank credit is “ the earning asset of the commercial banks, including the variety of short and long term loans made to individuals, partnership, corporation, other business firms, banks, and governmental units and agencies; the banks’ holdings of investments.”

One of the two primary functions of a commercial bank is to extend credit to the deficit economic unit that comprises borrowers of all types. Bank credit is a catalyst of economic development. Without adequate finance, there can be no growth in the economy. Bank lending is important for the economy in the sense that it can simultaneously finance all of the sub-sectors of financial arena, which comprises agricultural, commercial and industrial activities of a nation. Therefore, a bank is supposed to distribute its loan able fund among economic agent-in-deficit in a manner that it will generate sufficient income for it and at the same time benefit the borrower to overcome his/her deficit.

Components of Bank Credit:

Banks use to lend two ways- discounting bills and advances. Hence, Bank credit can be classified in two broad categories-

- Advances

- Bills discounted and purchased

1. Advances:

As the Encyclopaedia of Banking & Finance by Charles J. Woelfel states, an advance is, “In general a loan although an advance may be an open account as well as being evidenced by a note, with or without collateral.”

Again according to Radhaswami and Vasudevan (1985), “Advances are lending of money by banks against promissory notes executed by the customer with or without collateral security.”

Advances may be in the form of –

i) Loans

ii) Overdrafts

iii) Cash Credit

Whatever the form, advances are primary types of bank lending and major sources of income for banks. In Bangladesh, amount of advances (excluding the inter-bank) by the scheduled bank is about 97 percent of total credit.

Loans:

When an advance is made, with or without security, in a lump sum repayable either in fixed monthly instalment or in lump sum and no subsequent debit is ordinarily allowed except by the way of interest, incidental charges etc, it is called a loan. A loan once repaid in full or in part, cannot be drawn again by the borrower. It is given for a fixed period at an agreed rate of interest. The whole amount of loan is debited to the customer’s name on a loan account to be opened in the ledger and, is paid to the borrower either in the form of cash or by the way of credit to his current or savings account.

Overdrafts:

The overdraft is a kind of advance always allowed on a current account operated upon by cheques. The customer may be sanctioned a certain limit upon which, he/she can overdraw his current account within a stipulated period. Here, withdrawals or deposit can be made any number of times at the convenience of the borrower, provided that the total amount of overdrawn does not, at any time, exceed the agreed limit. Interest is calculated and charged only on the actual debit balance on daily product basis.

Cash credit:

A cash credit is an arrangement by which a banker allows his customer to borrow money up to a certain limit. Cash credit arrangements are usually made against the security of commodities hypothecated or pledged with the bank.

Hypothecation: In case of hypothecation the possession of goods remain at the disposal and in the go down of the borrower. The borrower is given access to goods whenever it so desires. The borrower furnishes periodical return of stock with the bank.

Pledge: In case of pledge, the goods are placed in custody of the bank with its name on the go down where they are stored. The borrower has no right to deal with them.

2. Bills Discounted and Purchased :

According to the Encyclopaedia of Banking & Finance by Charles J. Woelfel, bill discounted is “The aggregate of notes, acceptances and bill of exchanges which a bank has discounted for its customers, as distinguished from loans.”

The banks also give advances to their customers by discounting or purchasing their bills of exchange. Such bills of exchange arise out of commercial transactions both in inland trade and foreign trade. Bills are classified as i) Clean bills and ii) Documentary bills.

When the drawer of a bill encloses with the bill the documents of title to the goods, such as, Bill of Lading, Railway Receipt, Steamer Receipt, to be delivered to the

Drawee of the bill on payment against acceptance of bill, as the case may be, the bill is called a documentary bill. In the absence of such document it is termed as a clean bill. By the nature of payment, bills can also be classified into two categories named i) Demand bills and ii) Usance bills

Where a bill is payable ‘at sight’ or ‘on demand’ or ‘on presentation’ it is called a demand bill. If a bill matures for payment after a certain period of time, like 30, 60, or 90 days after the date, it is called a usance bill.

In case of purchase or discounting of bills, the banker credits the customer’s account with the amount of the bill after deducting his charges or discount. Bankers purchase the demand bills but discount the usance bills. In purchasing the income is interest but in discounting the income is discount.

Principles of Credit:

A prudent Banker should always adhere to the following general principles of lending funds to his customers.

- Background, Character and ability of the borrowers

- Purpose of the facility,

Term of facility,

- Safety,

- Security,

- Profitability,

- Source of repayment,

- Diversity.

Bank should never put “all its eggs in one basket”. It should be noted that selection of appropriate borrowers, proper follow-up and end-use supervision through constant close contact with the borrowers, are the corner stone’s for timely recovery of credit.

Factors of Credit Policy:

Credit policy of all banks cannot be developed on same lines because of differences in their operational needs and resource structures. In designing a credit policy, considerations should be given to following:

1) Total deposit resources of the bank and rate of fluctuation of resources.

2) Deposit structure.

3) Trend of growth in deposit and economic growth rate of the country.

4) Capital fund and other reserves. Large bank’s capital fund and secondary reserve in investment can permit its loan policy to be liberal in respect of its limit of lending in high risk-high returns loans while a relatively new small bank would stress more on liquid and highly secured loans at lower interest in its policy.

5) Capability of loan administration shall have to be given due weight in the credit policy. A large bank is able to hire numbers of highly skilled specialists/experts in different areas to advise the bank in loan making but smaller banks relying on usual credit managers cannot venture into sectors that require expert appraisal of loan applications and also that requires intensive post implementation monitoring of large and complex industrial loans.

6) Investment size of the bank and its nature.

Loan Documentation:

The minimum requirements for loan or other facility documentation of a Bank are:

a) Copies of the relative sanction letter indicating that the transaction has been approved by properly authorized officers of the Bank.

b) A copy of the letter of sanction addressed to the customer and his acceptance thereof.

c) All necessary documentation required to meet the terms and conditions of the facility in the manner in which it was approved.

d) Before disbursement, it should be satisfied that all legal formalities have been completed.

e) Disbursement of all facilities shall be made on an Offering Sheet basis to ensure that all additional requests are duly approved by two authorized Officers one of which must be the Manager or Sub-Manager.

f) Securities offered should also be thoroughly verified / inspected once in a month and stock report prepared.

g) Where the loan agreement calls for restrictive covenants and ongoing conditions, the Manager must not only satisfy himself that these are adhered to at the outset of the transaction (i.e. date of initial takedown) but assure himself, at regular intervals, that these are not being violated.

h) Since the Manager together with the Credit Officer is fully responsible for documentation, they will formally sign a check list. Under no circumstances may anyone permit drawings under any facilities, until they have signed off the check list.

I) The Manager/Sub-Manager should ensure that appropriate steps are being taken to keep loan documentation current for all assets Of the Bank. The loan documentation check-list, should, therefore, be reviewed at regular intervals.

J) Lines of credit should, as a rule, be confirmed in writing to the borrower. A Specific expiration date for the line should be included. Moreover every letter of sanction must contain the Bank’s standard clauses.

K) The borrower must explicitly undertake that all information supplied by him to Bank in connection with the approved lines Of credit is correct.

L) Any material or adverse change in business conditions will cause the amount due to Bank from the client immediately repayable. The Bank reserves the right to call back the facilities extended at any time without assigning any reason whatsoever.

Standard Procedure of Credit:

The Standard Procedure of Credit of a Bank is completed through the following Steps:

A) Any request for credit facilities, must be made by the borrower in the Bank’s prescribedstandard form properly filled in and completed in all respect and duly signed by the prospective borrower.

B) Submission of past 3 Years financial statement: For all credit proposals, the borrowers and guarantors (if any) should, wherever Possible submit past 3 years Profit & Loss A/C and Balance sheet duly audited by a recognized and competent Chartered Accountant containing unqualified opinions. Some borrowers may not have audited financial statements at all. In either case, the lending officer must interview the potential borrower or Guarantor and obtain satisfactory, accurate and complete financial information supporting any prior financial statements either audited or not audited. In the case of an individual borrower or guarantor, the financial statements must be signed by competent authority and must contain legend to the signatory, all assets and liabilities both direct and contingent and all sources of income and items of expenses. For all un-audited statements provided by a Company, financial Officer of the Company must execute such legend.

C) On all new credit arrangements an analysis of the credit worthiness of the borrower and guarantor (if any) should be prepared by the Credit Department at the Branch where credit monitoring responsibility lies and a copy thereof forwarded to the Head of Credit Division at ‘Head Office for pre-factor or post-factor review as the case may be. In case such credit originates in the Head Office, it will be forwarded to the Branch Manager for record and action.

Credit Analysis:

When a customer requests for a loan, bank officers analyse all available information to determine whether the loan meets the bank’s risk-return objectives. Credit analysis is essentially default risk analysis in which a loan officer attempts to evaluate a borrower’s ability and willingness to repay. The banker has to identify three distinct areas of commercial risk analysis related to the following questions:

1. What risks are inherent in the operations of the business?

2. What have managers done or failed to do in mitigating those risks?

3. How can a lender structure and control its own risks in supplying funds?

The first question forces the banker to generate a list of factors that indicate what could harm a borrower’s ability to repay. The second recognizes that repayment is largely a function of decision made by a borrower. Is management aware of the important risks and has it responded? The last question forces the banker to specify how risks can be controlled so that bank can structure an acceptable loan agreement.

Therefore, Bankers look into key risk factors or qualitative analysis which has been classified according to the five Cs of credit:

1. Character:

Character refers to the borrower’s honesty and trustworthiness. A banker must asses the borrower’s integrity and subsequent intent to repay. If there are any serious doubts, the loan should be rejected.

2. Capital:

Capital refers to the borrower’s wealth position measured by financial soundness and market standing. It helps cushion loses and reduces the likelihood of bankruptcy.

3. Capacity:

Capacity involves both borrower’s legal standing and management’s expertise in maintaining operations so the firm or individual can repay its debt obligations. Under capacity an individual must be able to generate income to repay the cash.

4. Condition:

A condition refers to the economic environment or industry specific supply, production and distribution factors influencing a firm’s operations. Repayment sources of cash often vary with the business cycle or consumer demand.

5. Collateral:

Collateral is the lender’s secondary source of repayment or security in the case of default. Having an asset that the bank can seize and liquidate when a borrower defaults reduces loss, but does not justify lending proceeds when the credit decision is originally made.

Under credit analysis Bank also does quantitative analysis which refers to the analysis of financial statement ratios to know the past performance of a company. Some of the key ratios which serve as a tool for financial analysis are classified as

1) Financial Ratio

2) Turnover Ratio

3) Profitability Ratio

Lending Risk Analysis:

Lending Risk Analysis (LRA) is simply a loan processing manual and has done when the amount of loan is above 1 core. By going through this manual the lending bankers can asses the creditworthiness of their prospective borrowers.

Therefore, LRA is such an instrument which is definitely and directly related with lending information to analyze the borrower’s financial, marketing, managerial and organisational aspects subjectively and objectively. It also facilitates the analyst to know the security risk of the credit. Lending risk Analysis involves assessing the likelihood of repayment of loans to the bank as per agreement on the basis of analysis of certain risks. To analyze these risks bankers will need to fill-up a 16-page LRA form. The form leads to scoring various risk factors involved in lending. LRA has divided the various risks into two groups namely, Business Risk and Security Risk.

Business Risk:

Business Risk is concerned with whatever the borrowing company would fail to generate sufficient cash out of business to repay the loan Business Risk, the main component of lending risk, consists of the Industry Risk and the company Risk

A. Industry Risk:

Due to some external reasons a business may fail and the risk which arrives from external reasons of the business is called Industry Risk. It has two components:

i) Supplies Risk:

When the business fails due to disruption in the supply of inputs, the consequent risk which would arise is known as Supply Risk

ii) Sales Risk:

When the business fails for disruption in sales, this type of risk would generate.

B. Company Risk:

Company Risk is shown for some internal reasons of the business. It has also two main components and four sub-components

i) Company position Risk:

Each and every company holds a position within an industry. This position is very much competitive. Due to weakness in the company’s position in its industry, a company may fail and the risk of failure is called Company Position Risk. It depends on-

(a) Performance Risk:

If a company fails to perform well enough to repay the loan because of its weakness under given expected external conditions, the company is said to suffer from performance risk.

(b) Resilience Risk:

When a company fails due to lack of its resilience to unexpected external conditions, the resilience risk is generated.

ii) Management Risk:

If the management of a company fails to exploit the company’s position effectively, the company can fail and this risk of failure is called management Risk. It can be subdivided further-

(a) Management Competence Risk:

Management competence risk is the risk that the company fails because the management is incomplete

(b) Management Integrity Risk:

Management integrity risk is the risk that the company fails to repay its loan due to lack of management integrity.

Security Risk:

Security risk is the risk that the realised value of the security does not cover the exposure of loan. Exposure means principal plus outstanding interest. Security risk can be divided

Into two parts

(a) Security Control Risk:

Security control Risk is the Risk that the bank fails to realise the security because of lack of bank’s control over the security offered by the borrowers.

(b) Security Cover Risk:

Security cover risk is the risk that the realised security value may not cover the full exposure of loans.

Collateral:

Collateral is the lender’s secondary source of repayment or security in the case of default. Having an asset that the bank can seize and liquidate when a borrower defaults reduces loss, but does not justify lending proceeds when the credit decision is originally made.

Characteristics of Good Collateral:

The following five items determine the suitability of items for use as collateral. The suitability depends in varying on standardisation, durability, identification, marketability and stability of value.

Standardization:

The standardisation leaves no ambiguity between the borrower and the lender as to the nature of the asset that is being used as collateral.

Durability:

Durability refers to the ability of the assets to withstand wear. Or it can refer to its useful life. Durable goods make better collateral than non-durable. Stated otherwise crushed rocks make better collateral than fresh flowers.

Identification:

Certain types of assets are readily identified because they have definite characteristics or serial numbers that cannot be removed. Two examples are a large office building and an automobile that can be identified y make, model and serial number.

Marketability:

In order for collateral to be of value to the bank, the collateral must be marketable. That is the borrower must be able to sell it. Specialised equipment is not as good as collateral as are dump trucks, which have multiple uses.

Stability of value:

Bankers prefer collateral whose market values are not likely to decline dramatically during the period of the loan such as common stock.

Different Types of Collateral:

Secure loans have a pledge of some of the borrower’s property behind them (such as home or an automobile) as collateral that may have to be sold if the borrowers have no other way to repay the bank. Some of the most popular collaterals are:

1. Account Receivable: The banks take a security in the form of a stated percentage of the borrower’s balance sheet. When the borrower’s credit customers send in cash to retire their debts this cash payments are applied to the balance of borrowers loans. The bank may agree to lend more money as new receivable arise from the borrowers sells to its customers thus allowing the loan to continue as long as the borrower has need for credit and continuous to generate and adequate volume of sales.

2. Factoring: bank can purchase a borrowers account receivable based upon some percentage of the book value because the bank takes over the ownership of the receivable, it will inform the borrowers customers that hey should send their payments to the purchasing bank.

3. Inventory: A bank will lend only a percentage of the estimated market value of a borrower’s inventory in order to leave a substantial cushion in case the inventories value begins to decline. The inventory pledged may be controlled completely by the borrower using a so-called floating line approach.

4. Real Property:A bank may take a security interest in land and / or improvements on land own by the borrower and records its clime-a mortgage-with a government agency in order to define against successful claim by others.

5. Personal Property:Bank takes a security in jewellery, securities and other forms of personal property owned by a borrower.

6. Personal Guarantees: A pledge of the stock deposits or other personal assets held by the major stock holders or owners of a company may be required as collateral to secure a business loan.

Loan Review:

In a bank the purpose of loan review is to minimize loan losses by reviewing outstanding loans in order to –

1. Identify potential problems with specific loans.

2. Identify weaknesses in procedures or personnel in general

- Quantify the repayment risk in the loan portfolio by estimating how much cash borrowers can generate under current market conditions from operations and collateral.

Loan Classification as per Bangladesh Bank:

The classification of loan provided by different commercial banks can be shown through the following table.

| Classification | Types of loan | ||||

| Agricultural short term | Continuous | Demand | Term (Up to 5 years) | Term (> 5 years) | |

| Unclassified | 12 months or below | Less than 6 months | Less than 6 months | Less than 6 months | Less than 12 months |

| Substandard | Overdue more than 12 months but less than 36 months | Overdue 6 months to 9 months | 6 months to 9 months | If defaulted amount of installment is equal to 6 months payables | If defaulted amount of installment is equal to 12 months payables |

| Doubtful | Overdue more than 36 months but less than 60 months | Overdue 9 months to 12 months | 9 months to 12 months | If defaulted amount of installment is equal to 12 months payables | 18 months or more |

| Bad loan | Overdue more than 60 months | Overdue 12 months or more | 12 months or more | Overdue of 18 months payables | Overdue of 24 months payables |

Source: BRPD circular no: 09 dated 14th May, 2010

Qualitative Judgment Criteria:

- Unclassified: Repayment is regular.

- Substandard: Repayment is irregular but has reasonable prospect of improvement.

- Doubtful Debt: Unlikely to be repaid but special collection efforts may result in partial recovery.

- Bad/Loss: Very little chance of recovery.

Other Loan Provisions from Bangladesh Bank:

1. Necessary CL forms on Loan Classification, Provisioning and Interest Suspense Account were forwarded through the said circular letter. It needs to be mentioned that policy on maintaining general provision @ 5% on “Special Mention Account” has been circulated vide BRPD Circular No. 09 dated 20-08-2008. Furthermore, banks have already been advised to maintain general provision @ 2% on Small Enterprise Financing and Consumer Financing.

2. As per existing interest rate policy, banks are empowered to determine interest rate on lending (except export credit) by themselves. In order to inform their clients, banks announce information relating to interest rate. It may be mentioned that banks can differentiate on interest rate not more than 3% in the same sector considering comparative risk among the borrowers.

3. In order to establish more transparency in determining interest rate and also to make it easily understandable and clear to their clients, it has been decided that henceforth banks will announce mid rate of interest rate band (if any) on respective sector while declaring interest rate on lending. Banks may charge interest rate 1.5% lower or higher than the declared rate considering comparative risk from client to client.

4. Refer to our BRPD Circular No. 02, dated 15 February, 2005 on the captioned subject. In order to strengthen credit discipline and bring classification policy in line with international standards, Bangladesh Bank has from time to time revised its prudential norms for loan classification and provisioning. As part of the process, Bangladesh Bank has already introduced ‘Special Mention Account’ vide the above circular so that banks can raise early warning signals for accounts showing first signs of weakness. As a further move towards this end, Bangladesh Bank feels that appropriate provisioning against such accounts is necessary.

Accordingly, the following amendments have been made to the above circular:

(1) Banks will be required to make General Provision @ 5% on the outstanding amount of loans kept in the ‘Special Mention Account’ after netting off the amount of Interest Suspense.

(2) The status of the loan should be reported to the Credit Information Bureau (CIB) of Bangladesh Bank. As such, there will be five categories of loan classification status instead of existing four for reporting to CIB. However, it is reiterated that loans in the ‘Special Mention Account’ will not be treated as defaulted loan for the purpose of Section 27KaKa(3) Of the Bank Company Act, 1991

5. Banks had been instructed to conduct loan classification activities and also to maintain provisions on quarterly basis vide BRPD circular no.16, dated 06, December 2008.

It has been observed that though banks are conducting loan classification activities on quarterly basis, some banks are not maintaining provision on quarterly basis which is not consistent with the instructions given in the said circular.

Under the circumstances, banks are again instructed to maintain provision on quarterly basis as per existing policies while conducting loan classification activities on the said basis.

6. Bank Companies are hereby advised to submit a Statement of loans extended to the Directors of the Financial Institutions as per Annexure “A” to the Financial Institutions Department of Bangladesh Bank at the end of each quarter within next 15(Fifteen) days of the following month of the quarter to which the statement relates. The first statement will be based on 30th June, 2010. To this end, up to date list of the Directors of Financial

Institutions may be collected from the Financial Institutions Department of Bangladesh Bank.

Types of Loans & Advances of PBL:

Prime Bank has been offering all types of credit products available in the Bangladesh financial market. Under the corporate credit portfolio, it has two basic types of products. These are

(i) Funded Credit and

(ii) Non-funded Credit.

(i) Funded Facilities: Funded credit facilities are divided into three types namely

(a) Continuous Loan,

(b) Demand Loan,

(c) Term Loan

a) Continuous Loan:

The loan Accounts in which transactions may be made within certain limit and have an expiry date for full adjustment will be treated as Continuous Loans. Examples are:

a) Cash Credit (Hypothecation)

b) Cash Credit (Pledge)

c) Loan against imported merchandise (LIM)

d) Loan against trust receipts (LTR)

e) SOD (FO)

f) SOD (Special Scheme)

g) SOD (Earnest Money)

h) SOD (Work Order)

i) SOD (General)

j) Packing Credit

k) Forced loan

l) Others

b) Demand Loan:

The loans that become repayable on demand by the bank will be treated as Demand Loans. If any contingent or any other liabilities are turned to forced loans (i.e. without any prior approval as regular loan) those too will be treated as Demand Loans:

b) PAD (Payment Against Documents)

c) IDBP (Inland Documentary Bill Purchased)

d) FDBP (Foreign Document Bill Purchased)

e) SOD (Export)

f) TOD (Temporary Overdraft)

g) Bridge Loan

h) Loan (Against EDF)

i) Factoring

j) Others

a) Short-term Agricultural and Micro Credit:

Short-term Agricultural and Micro credit will include the short-term credits as listed under the Annual Credit Program issued by the Agricultural Credit Department of Bangladesh Bank. Credits in the agricultural sector repayable within less than 12 months will also be included herein. Short-term Micro-Credits will include any micro-credits for less than Tk.10, 0007 and repayable within less than 12 months, be those termed in any names such as Non-agricultural credit, Self-reliant Credit, Weaver’s Credit or Bank’s individual project credit. L/C (Sight)

(ii) Non-funded Facilities:

a) L/C (Sight)

b) L/C (Differed Payment)

c) Back To Back L/C

d) Inland L/C

e) Bid Bond

f) Retention Bond

g) Performance Guarantee

h) Payment Guarantee

i) Advance Payment Guarantee

j) Guarantee against Counter Guarantee

k) Others

Letter of Credit (L/C):This product is within the purview of the “Trade Service’”. Details about it are available in the “Wish List” provided by the “Trade Service Group”.

Letter of Guarantee (L/G): There are basically two types of Guarantee: (a) L/G (Local), and (b) L/G (Foreign). Besides Guarantees may be in the following forms:

- Bid Bond

- Retention Bond

- Performance Bond

- Payment Guarantee

- Advance Payment Guarantee

- Admiralty Bond

- Others

Features of L/G (Local):

- Usually, L/G (Local) is issued against margin, collateral security. However, there might be some deviation approved by the competent authority.

- Commission is charged on quarterly basis at an approved rate.

Features of L/G (Foreign):

It is issued against Counter Guarantee of a Foreign Bank having correspondent banking relationship with Prime Bank Ltd. Commission is charged on quarterly basis.

Salient features of Credit Policy of PBL:

- Assets are built based on customer’s deposit, which should not exceed 80% of customers based deposit

- Rate of interest is variable based on customers’ integrity and risks associated

- Type of security varies on the basis of risks associated in credit.

- Diversification of credit on the basis of geographical location, size of credit, sectors and sub-sectors etc

- Credit operations are carried out in branch through branch credit committee as per authority delegated to head of branch and through Head Office Credit Committee in respect of credit sanction authority delegated to the CEO.

- No credit should be allowed for a period not exceeding 5 years

- Aggregate long-term credit facilities shall not exceed 20% of total credit portfolio.

- Single customer’s exposure should not exceed 50% of the Bank’s Capital Funds.

- LRA is done in most cases.

- Assessment of volume or amount of credit properly.

- Utmost care is taken in providing loans to directors.

- Funded facility is 25% of paid up capital.

Different Loan Schemes of PBL:

- General Loan Scheme

- Lease Finance

- House Building/ Apartment Loan Scheme

- Small and Medium Enterprise Credit Scheme

- Hire Purchase

- Consumer Credit Scheme

General Loan Scheme :

Depending on the various nature of financing, all the lending activities have been brought under the following General Loan:

- Short term Loan

- Medium term Loan

- Long term Loan

The loans allowed to individual/firm/industries for a specific purpose but for a definite period and generally repayable by installments fall under this head. This type of lending are mainly allowed accommodating financing under the categories (i) Large & Medium Scale Industry and (ii) Small & Cottage Industry and very often term financing for (1) Agriculture (ii) others.

Lease Finance:

Lease financing is one of the most convenient long term sources of acquiring capital machinery and equipment. It is a very popular scheme whereby a client is given the opportunity to have an exclusive right to use an asset, usually for an agreed period of time, against payment of rent. Of late, the lease finance has become very popular in almost all the countries of the world. An obvious advantage of the lease is to use an asset without buying it. The lessee is obligated to make lease payments until the expiration of the lease agreement, which corresponds to the useful life of the asset.

In a capital scarce economy like ours, Lease Financing is suitable for firms to acquire Capital Machinery, Equipments, Medical Instruments, and Automobiles etc. And thereby they employ their own resources more advantageously in some other investments. Lease financing also helps a firm to reap significant economic benefit through tax saving and by reducing the risk of the equipments becoming obsolete due to the technological advancement.

Objectives:

Prime Bank Ltd. has introduced the lease finance with the following objectives:

- To assist the genuine and capable entrepreneurs for acquiring capital machinery and equipments to undertake enterprises without equity.

- To encourage the new and educated young entrepreneurs to undertake productive venture and demonstrate their creativity and thereby participate in the national development.

- To participate in the industrial development of the country.

Lease Items / Equipments:

Prime Bank Limited offers lease finance for acquiring the use of capital machinery, equipments, medical instruments, etc. The customers are entitled to decide the specification, price and model of the lease item/equipment. Bank will purchase the item (s) in accordance with the specifications given by the clients. However, the suppliers of the items must ensure after sales services and warranties. The price should be competitive and acceptable to the Bank.

Eligibility for Availing Lease Finance:

All genuine entrepreneurs having adequate experience and expertise are eligible to apply for Lease Finance under the scheme. The amount of Lease Finance will not generally exceed Tk. 1.00 core, but in exceptionally good cases, the limit can reasonably be exceeded on condition that the Bank will depute an officer for close and intensive supervision of the project.

Documents & Security:

The entrepreneur will be required to provide the following securities:

- The lease items will remain in the name of the Bank i.e., Bank will be the sole owner of the leased items. Collateral securities having liquidation value covering at least 100% of the amount of finance. Deposit of listed Shares, National Savings Certificates, ICB Unit Certificates, Assignment of Life Insurance Policies, Bank Guarantee, and Insurance Guarantee etc. will also be acceptable as collateral securities.

- In case of existing industrial units requiring BMRE, charge may be created on the existing fixed assets as collateral securities for the finance. In case of existing Automobile enterprises, creation of charge on the existing vehicles will also be acceptable as collateral securities.

- In case of default in payment of lease rental for consecutive 2 (two) months, the Bank will take over the lease items without giving any prior notice. ii) In case of taking over the lease items by the Bank before maturity, the lessee will be liable for the loss, if any, caused to the Bank of such premature taking over. iii) the Bank will exercise close and intensive supervision of such projects. An Officer of the Bank will be engaged separately for supervision of such projects to ensure proper utilization of the lease items and timely repayment of the monthly rentals.

House Building / Apartment Loan Scheme :

Loans allowed to individual/enterprises for construction of house (residential or commercial) fall under this type of advance. The amount is repayable by monthly installment within a specified period. Such advances are known as Loan (HBL-GEN).

Loans allowed to our Bank Employees for purchase /construction of house shall be headed Staff Loan (HBL-STAFF).

Small & Medium Enterprise (SME):

Bangladesh is a densely populated country. Job opportunity here is very scanty; unemployment rate is approximately 40%. Population below poverty line is 36%. Therefore, it is the prime concern for the nation to generate income through creation of job opportunity & employment. Creation of job opportunity at large scale by us is not possible. What can be done better is to help self-employment through financial support. There are many small and medium entrepreneurs in the country that have innovative idea, spirit and potentiality to do something productive for local consumers as well as export abroad.

They can generate income and contribute to the GDP. They may also provide employment to other people. Development and growth of Small and Medium Enterprise is vital for national development. Such type of beneficial enterprise borrowers can not go a long way for want of financial support because they have no access to institutional credit facilities, as they cannot provide collateral security as demanded for such credit facility.

Prime Bank Limited is committed to play positive role in the overall socioeconomic development of the country. There is also a statement in the objective clause of Memorandum of Association of Prime Bank Limited as under:

- To advance or lend money to the unemployed persons for self-employment and rehabilitation in the Society.

- To finance the Small and Cottage Industries for Industrialization and also to create employment opportunities.

It may be mentioned here that as per decision of the Board of Directors in its 78th meeting held on 17.11.1999 a “Small & Medium Enterprise (SME) Cell” has already been established at Head Office under the Credit Division.

If we look at South East Asia, China, Taiwan, Hong Kong, South Korea etc we will find that small and Medium Businesses are the real engine of growth in those countries.

In view of the above a credit scheme titled “Small and Medium Enterprise Credit Scheme” has been formulated as follows. It may also be mentioned that USAID has approved our bank to receive their guarantee facility to lend money to Small and Medium business Houses. 50% of losses, if any, are paid by USAID.

Objectives :

- To provide credit facilities to the small and medium size entrepreneurs located in Urban & Sub-urban areas and easily accessible by the branches.

- To encourage the new and educated young entrepreneurs to undertake productive venture and demonstrate their creativity and thereby participate in the national development.

- To flow credit for creation of employment and generation of income on a sustainable basis through development of small & medium enterprises.

- To assist potential entrepreneurs to take part in economic activities so that they can improve their living standard.

- To reduce dependence on money lenders

- To make the small & medium enterprises self-reliant;

- To develop saving habit and making acquaintance with banking facilities.

- To inspire for undertaking small projects for creation employment through income generating activities.

Consumer Credit Scheme (CCS):

.Prime bank is committed to play a vital role in overall socio economy development of our country. As per its commitment, it launched “Consumer Credit Scheme” in the year 1995 to enhance the living standard of the people of limited and fixed income group.

Objectives of the Scheme:

- Prime Bank Limited started the Consumer Credit Scheme program with a view to fulfil its benevolent institutional objectives through financing the middle class limited income group.

- To ensure the credit facility to the both middle class limited income group and upper class income group.

- To improve the living standard of limited income group through financing in purchasing necessary goods.

- To participate in the socio-economic development of the country.

Eligibility of the customer:

Any interested person within the range of 25 to 60 and having a permanent job or the permanent employees of the following organization can apply for the CCS loan of Prime Bank.

- Government Organizations.

- Semi-Government and Autonomous Bodies.

- Banks, Insurances Companies or any other financial institutions.

- Armed Forces, B.D.R, Police and Anwar.

- Private Organizations having corporate structure.

- Teachers of Universities, Colleges and Schools.

- Permanent employees of locally established and renounced Public Limited Companies.

- Permanent employees of Multinational Companies.

- Permanent employees of Bank acceptable companies

- Professionals such as Doctors, Engineers, Lawyers, Architects, Chartered Accountants, Journalists, and self employed person etc.

Discourage list of the customer:

The following are the people who should be discouraged in extending credit facilities under this scheme:

- The employees of frequently transferable services.

- The employees of enterprises which are not of good reputation.

- Employees having take home salary less than taka 10,000 per month.

Credit Limit, Period of Loan & Down payment:

Under CCS program of Prime Bank Limited a borrower can get maximum of taka 40, 00,000 and minimum taka 10,000. The down payment is 13% of the loan for each product.

Interest and other charges:

The interest rate is 15% for the all products. And Prime Bank charges 1% service charge and 1% risk fund for all products other than for Car loan, Doctor’s loan, Advance against salary and CNG conversion loan.

Application procedure:

The intending client will have to apply for the credit in Bank’s printed application form, which is available in respective branch on payment of Taka 10 only. Customers will submit the application form dully filed-in with 2(two) photographs and sign along with quotation for purchase of desired article or any other relevant documents.

The customers’ name/other name(s) including nickname, if any should be mentioned in every loan application.

Processing of applications:

On proper scrutiny of the application, branch will inform the initial decision (acceptable for processing /decline) to the applicant within 3(three) working days from the date of receiving application. Applicant will submit the above dully filed-in with the following additional papers:

- Salary certificate for service holders.

- Trade license and TIN Certificate (if any) for businessperson.

- TIN Certificate of applicants for vehicle loan (compulsory)

- Bank statement of last six months.

- Attested photocopies of current tax receipt, electric bill etc & lease agreement (if any) when the source of income is house rent as a land lord.

Branch will inspect the given information with respect to eligibility, feasibility and security. After completion of all necessary formalities, the branch shall disburse the loan or refuse the proposal within 7(seven) working days from receiving the additional papers. Price of the items (down payment + loan amount) should be given to the respective supplier through Payment order (PO) after completion of necessary documentation.

Monitoring and Recovery under CCS:

The credit under this scheme is fully supervised and as such, the success of the scheme depends on proper and persistent supervision, follow up, persuasion and monitoring of the credits by the Branches. Branches shall maintain proper records of the applications received, loan sanctioned, disbursement and recovery made. It is worthwhile to mention here that optimum recovery can be ensured by developing relationship with the customers and the beneficiaries and maintaining supervision thereon without filing any suit/case. The mechanism of supervision and monitoring are as follows:

- Regular checking of the balance of the clients account

- Regular communication with the defaulting customer and guarantors physically/over telephone.

- Issuance of letter to customers immediately after dishonor of cheque.

- Issuance of letter to defaulting customers and respective guarantors.

- Contacting the employers of the defaulting customers (after three overdue installments)

- Issuance of legal notice to the customers and guarantors prior classification of loans.

- Issuance of application/greeting letter to the regular customers.

- Periodical visit to the customer to maintain relationship and supervision of supplied goods/items.

- Legal actions to be taken after all possible efforts to recover the Bank’s dues go in vain.

Steps against Defaulters under CCS:

If a borrower fails to pay 3(three) installments consecutively he/she is considered as a defaulter. Prime Bank Limited usually follows the following guidelines for treatment of its overdue installments.

- Telephone contact

- Cheque bounce Letter

- Overdue recover Letter

- Letter of guarantors

- Letter to authority

- Legal notice to borrower and guarantor

- Suit notice

Loan Amortization under CCS:

Prime Bank uses the most common loan amortization method that is “Capital Recovery Method”. Under this method constant monthly payment is calculated on an original loan amount at affixed interest for a given term.

Example:

Loan Amount: BDT 100,000 (PV)

Interest rate: 15%

Number of Installments (monthly): 24

So monthly install will be: PV/MPVIFA* (15%, 24months)

So Monthly installment: 100,000/20.62423451=BDT 4848.66

*MPVIFA=Monthly Present Value Annuity Factor.

Prepayment:

Customer can repay the loan before the maturity of the loan. Prime usually welcomes the early payment of loan and no prepayment penalty is to be charged. Prime bank always tries to avoid classified loan even at a cost of losing profit and receiving risk just to maintain its credit history and good CAMEL rating.

Products under Consumer Credit Scheme:

The products of Prime Bank with their financing items under CCS loan are given below:

- Household Durable Loan: Motor Cycle, Personal Computer, Photocopier, Fax machine, Small PABX system, Television, Mobile Phone set, Refrigerator, Audio-video equipment, Other home electric appliances, Furniture and any other household items.

- Doctors Loan: For the doctors only

- Any Purpose Loan: For emergency need

- CNG Conversion Loan: To convert into CNG

- Car Loan: Car, Jeep, Station Jeep, Pick up Van, Cover Van, Bus, Truck, Ambulance and any other vehicle for own use.

- Advance Against Salary: Any qualified person

- Education Loan: For Study purpose only

- Marriage loan: For wedding only.

- Hospitalization Loan: For treatment in hospital

a. Household Durable Loan:

Household durable loan will be sanctioned against guarantee of third parties acceptable to the bank or pledge of FDR, Saving instrument of Banks and assignment of salary where applicable.

Eligible Items / Articles

- Motor Cycle

- Personal Computer

- Photocopier / Fax Machine

- Small PABX System

- Television

- Mobile Phone Set

- Refrigerator

- Audio-Video Equipment

- Other Home Electric Appliance

- Furniture

- Any Other Household Durables

Loan Limit and Period of Loans:

| Name of the Item | Loan Limit | Duration of the Loan |

| Motor Cycle | Tk. 1,00,000 | 2-yrs |

| PC/Lap Top | Tk. 1,00,000 | 2-yrs |

| Photocopier/Fax | Tk. 1,00,000 | 2-yrs |

| Other Item/Furniture | Tk. 5,00,000 | 3-yrs |

Required Documents:

Employer Certificate for Service Holders

Photocopy of Trade License for Businessmen

Photocopy of Tin Certificate, if any

Bank Account Statement of last six months

Photocopy of Passport, Telephone (T&T) Bill, if any

Security:

Two Personal Guarantees

Undated Cheques

b) Doctors Loan:

Any Bangladesh citizen who is a graduate in Medical Science / Dentist / Eye / Allopathic / General Practioners desiring to set up chamber, medical store with necessary medical equipments and to become self-employed have the opportunity to take this loan.

Required Document:

- Employer Certificate for Service Holders

- Photocopy of Tin Certificate, if any

- Bank Account Statement of last six months

- Photocopy of Passport, Telephone (T&T) Bill, if any

- Attested Photocopy of the Certificates of the last degree and BMA membership certificate

Security:

The ownership of medical equipments to be purchased must be hypothecated to the Bank under hire purchase mode:

- Two personal guarantees

- Undated cheques

c) Any Purpose Loan:

This scheme is to meet the emergency need for fund by fixed income group of salaried person in Govt./Semi govt. /Autonomous bodies/ Multinational Co./ Banks/Insurance/Financial Inst./Educational Inst. with confirmed 3-years service ahead. Letter of introduction including name, fathers name, designation, date of birth, date of joining, place of posting, date of last promotion, date of retirement, basic salary, total emolument, take home salary etc. will be required. This scheme is only for service holder.

Loan Limit and Period of Loans:

| Type of Customer | Loan Limit | Duration of the Loan |

| Salaried Person | Tk. 200,000 | 3-yrs |

Required Documents:

- Employer Certificate

- Photocopy of Tin Certificate, if any

- Bank Account Statement of last six months

- Photocopy of Passport, Telephone (T&T) Bill, if any

Security:

- Undated Cheques

- Lien on Service benefit of the concerned employee from the employer

d) CNG Conversion Loan:

This scheme is to meet the funds requirement for CNG conversion of vehicles for those who are salaried person in Govt./Semi govt. /Autonomous bodies/ Multinational Co./Banks/Insurance/Financial Inst./Educational Inst. with confirmed 3-years service ahead, businessman having adequate cash flow and corporate Bodies

Loan Limit and Period of Loan:

| Type of Customer | Loan Limit | Duration of the Loan |

| Owner / Valid user of the vehicle

| Tk. 60,000 | 1.5-yrs |

| Owner / Valid user of the vehicle

| Tk. 1,00,000 | 1.5-yrs |

Required Documents:

- Employer Certificate for Service Holders

- Photocopy of Trade License for Businessmen

- Photocopy of Tin Certificate, if any

- Bank Account Statement of last six months

- Photocopy of Passport, Telephone (T&T) Bill, if any

- Photocopy of the Blue Book etc

- Photocopy of the registration of the Vehicle

Security:

- One or two personal guarantee from family member (effective member i.e. spouse / father / mother / brother / earning son, Corporate guarantee in the case of Company or as the case may be acceptable in the bank).

- Undated cheques in favors of the Bank covering the whole amount.

Recommendations :

From the findings of the report we can expose the following recommendations for the betterment and further success of the credit division of Prime Bank Ltd.:

- The down payment paid by CCS customers is very high with PBL. Besides, others bank such as- Dhaka Bank Limited, AB bank Limited, And Eastern Bank Limited are not taking any down payment. So I think PBL should not take any down payment or reduce the down payment percentage to make its CCS more competitive.

- Interest rate and payback period are very important criteria for any kind of loan but most of the clients are not satisfied to PBL Consumer Credit interest rate and loan payment period. They want lower interest rate and more payment period and reduce interest rate. Therefore I suggest for increasing payment period. It will make the installment more attractive and convenient for customers to pay. At the same time it will help reduce outstanding for the bank.

- All the lending and savings packages offered to the Premium customers are same as offered to the general customers, excepting the waiver of service charges for premium ones. Prime Bank Limited should try to introduce more attractive lending and savings scheme to its Premium customers to create more business for the Bank. The Bank can pay more attention to this segment of customers, as it is the most solvent group from which income can be generated if the package is designed properly.

- Premium Customer should be offered occasional gifts and discounts, which can make the premium service more attractive and keep consumer delighted. The interest rates on several loan and deposit schemes should be differentiated for the premium customers.

Conclusion :

Prime Bank Limited is a potential and promising bank in the banking sector of Bangladesh. Credit Management policies and techniques used in the bank at present is comparable to international standards. The officials follow the policy very strictly. They are very much sincere and conservative in sanctioning loan. The proposal is thoroughly scrutinized by the loan sanctioning authority. The total function of the credit division is monitored periodically. From overall findings it is transparent that the credit division of Prime Bank Ltd is one of the most efficient and well operated divisions.