Executive Summary

This internship report is prepared as a partial fulfillment for the MBA program of the department of finance under Stamford UniversityBangladesh. This report focuses three month working experiences in Head Office of One Finance MCS Limited. This report will give a clear idea about activities and operational strategies of One Finance MCS Limited. Especially this report focuses on the overall Credit Management of One Finance MCS Limited.

I have divided the whole report into twelve chapters. Those chapters are backdrop of the report, Banking sector in Bangladesh. A short profile of One Finance MCS Limited, Introduction, overview of One Finance MCS Limited, Theoretical concept of the performance, credit policy, fund invested by One Finance MCS Limited, loan disbursement procedure of One Finance MCS Limited, recovery performance of One Finance MCS Limited, classified loans performance, guidelines for Credit Management, findings & and analysis etc.

In first chapter, I have explained about background of the study, objectives, methodology, rationale and scope and limitations of the study.

In second chapter, I have tried to review the, Mission, Objectives and the Management of One Finance MCS Limited.

In the third chapter, I have explained the theoretical concept of the performance, Credit Management, process of Credit Management, policy and program guidelines, tools of Credit Management, Credit Risk Grading, functions of credit risk grading, financial spread sheet in Credit Management.

I have explained credit policy and fund invested by One Finance MCS Limited.

I have explained loan disbursement procedure, recovery performance, classified loans and performance, guidelines for Credit Management of One Finance MCS Limited.

Finally I have explained findings, analysis Conclusion & Recommendation.

In fine, I can say that, I have tried to put my honest and sincere efforts while preparing these report. All my exertion and pains taking efforts will be successful, if it becomes conducive to One Finance MCS Limited.

Background of the study

This report is based on the internship program. One Finance MCS Limited arranges internship program provide practical knowledge about Micro Credit activities for university students as universities conducted with different organization after the completion of theoretical courses of program of Master of Business Administration (MBA). A group of interns must carry out a specific project, which is assigned by One Finance MCS Limited. In this particular report, I am an internee of the previously mentioned program and the concerned organization is One Finance MCS Limited which is a prominent co-operative society of Bangladesh. Hence I am placed in Employment Head Office of One Finance MCS Limited from December 11’ 2010 to till now.

Objectives of the Study

There are mainly two objectives behind the preparation of this report- primary objective and secondary objective.

Primary objective

The primary objective of preparing this report is to fulfill the partial requirement of the MBA program and to represent the “Credit Management” of One Finance MCS Limited.

Secondary objective

The secondary objectives of the report are as below:

To co-ordinate between theory and practice and to make a bridge between theoretical and practical knowledge in fulfillment of the internship program.

To know about the micro credit system.

To identify the formalities maintained by both the co-operative and the client in processing and receiving deposit.

To identify the major problems of the co-operative encounters in handling micro credit activities.

Methodology

The word method comes from the Greek word ‘Meta’ and ‘Hoods’ meaning a way. Broadly, a method or methodology is the underlying rules of a philosophical system of inquiry procedure. A method involves a process or technique in which various stages or steps of collecting data/information are explained and the analytical techniques are defined. In simple a method is the way of doing something.

Sources of data/ Information

I have collected the information/data from both primary and secondary sources.

Primary sources

Primary sources include interviews and conversation with officers and executives of the co-operative of different divisions and departments.

Secondary sources

Secondary sources of information include annual report, general report, project profile, journals, periodicals, co-operative manual, selected books and other publications.

Analysis of data:

Two approaches have been mainly used in this report-

- Conceptual approach

- Empirical approach

Rationale and Scope of the Study

Rationale

One Finance MCS Limited has discovered a new horizon in the field of co-operative area, which offers different Transaction, Investment and co-operation in co-operative system. So I have decided to study on the topic “Credit Management of One Finance MCS Limited”. Because the Internship program of the university is an integral part of the MBA program. So it is obligatory to undertake such task by the students who desirous to complete and successfully end-up their MBA degree. This also provides an opportunity to the students to minimize the gap between theoretical and practical knowledge. Students are required to work on a specific topic based on their theoretical and practical knowledge acquired during the period of the internship program and then submit it to the teacher. That is why I have prepared this report.

Scope

This Internship report covers the overall activities performed by “One Finance MCS Limited”, such as Loans and Advances, Lesage and Trades.

This report has been prepared through extensive discussion with co-operative employees and with the customers. While preparing this report, I had a great opportunity to have an in depth knowledge of all the activities practiced by the “One Finance MCS Limited”. It also helped me to acquire a first hand perspective of a co-operative in Bangladesh.

Limitations of the Study

The time period for this study was short.

The staffs of the office were some times so busy that they could not help us all time.

Preparing internship report is really troublesome.

This type of report preparation is expensive.

Collection of data was not smooth.

Analyzing with financial data is much more confusing and complicated than any other data.

Secrecy of management.

Lack of knowledge and experience among the officials.

Company Overview

One Finance MCS Limited is one of the leading private sector co-operative that started its co-operative operation in Dhaka on July 10’ 2010. It has focused on the established and emerging markets of Bangladesh. Concentrating hard on the activities of its area of specialization, One Finance MCS Limited has been able to achieve excellent market standard with competent customer service. By means of such measures the co-operative intends to grow. One Finance MCS Limited pledges to maximize customer satisfaction through services and build a trusting relationship with customers.

The emergence of One Finance MCS Limited was at the juncture of liberalization of global economic activities. Not only this, it comes forward at a crucial state of affairs when Bangladesh was undergoing through economic reforms and trade liberalization according to the Uruguay Round Agreement, World Bank (WB) and International Monitory Fund (IMF) recommendations. The experience of the prosperous economies of the Asian countries, in particular of South Asia, has been the driving force and the strategic operational policy option of the co-operative. The company philosophy – “Setting a new standard in co-operative” has been precisely an essence of the legend of its success in the Asian countries.

One Finance MCS Limited at a glance

Head Office : 24-25, Dilkusha C/A, Dhaka.

Corporation Set-up : Public Limited Company

Certificate of Incorporation : July 10, 2010

Commercial operation : July 20, 2010

Main operational areas : Dhaka

Vision

To be the co-operative of 1st choice by creating exceptional value for our clients, investors and employees alike

Mission

The mission of the One Finance MCS Limited is to actively participate in the socio- economic development of the nation by operating a commercially sound co-operative organization, providing credit to viable borrowers, efficiently delivered and competitively priced, simultaneously protecting depositor’s funds and providing a satisfactory return on equity to the owners.

History of One Finance MCS Limited

One Finance MCS Limited is a progressive Co-operative. One Finance MCS Limited has been incorporated as a Public Limited Company on July 01’ 2010 vide certificate of incorporation # C 66933 (4425)/07.

One Finance MCS Limited has an authorized capital of Tk. 30 crore paid up capital of Tk. 10 crore and reserve of Tk.11 crore. The co-operative has a total asset of Tk. 50 crore as on 30th April 2011.

The principal activities of the co-operative are providing of all kinds of commercial co-operative services to its customers and the principal activities of its subsidiaries are to carry on the remittance business and to undertake and participate in any or all transaction, and operations commonly carried or undertaken by remittance and exchange houses.

Definition of Credit

Credit is the institutional arrangement of lending funds mainly to the traders and industrial entrepreneurs by the Co-operative society. The major portion of co-operative funds is employed by various ways of loans and advances, which is the most profitable employment of its funds. The major part of co-operative income is earned from interest and discount on the funds so lent. The job in this department starts from the application made by the client; approve the same, which is disbursed to customers.

Credit Management

As One Finance MCS Ltd is providing credit facility out of its total available funds, it has to manage these credits very efficiently. An efficient credit management system comprises many things and this cover the pre-sanction activities to post-sanction activities. Credit management is important as it helps the co-operative and financial institutions to understand various dimensions of risk involved in different credit transactions.

At the pre-sanction stage, credit management helps the sanctioning authority to decide whether to lend or not to lend, what should be the loan price, what should be the extent of exposure, what should be the appropriate credit facility, what are the various facilities, what are the various risk mitigation tools to put a cap on the risk level.

At the post-sanctioning stage, the bank can decide about the depth of the review of renewal, frequency of review, periodicity of the grading, and other precautions to be taken.

Having considered the significance of credit risk, it becomes imperative for the co-operative system to carefully develop credit management. For this reason, the co-operative is maintaining a new division which is well-known as credit division.

PROCESS OF CREDIT MANAGEMENT

Credit Management Policy for any co-operative must have been prepared in accordance with the Policy Guidelines of Directorate of Co-operative Focus Group on Credit and Risk Management with some changes to meet particular co-operative internal needs.

Credit management must be organized in such a process that the co-operative can minimize its losses for payment of expected dividend to the shareholders. The purpose of this process is to provide directional guidelines that will improve the risk management culture, establish minimum standards for segregation of duties and responsibilities, and assist in the ongoing improvement of concerned co-operative.

The guidelines for credit management may be organized into the following sections:

Policy guidelines

a. Lending guidelines: The lending guidelines include the following:

- Industry and Business Segment Focus

- Types of loan facilities

- Single borrowers/ group limits/ syndication

- Lending caps

- Discouraged business types

As a minimum, the followings are discouraged:

- Military equipment/ weapons finance

- Highly leveraged transactions

- Finance of speculative investments

- Logging, mineral extraction/ mining, or other activity that is

- Ethically or environmentally sensitive

- Lending to companies listed on CIB black list or known

- Counter parties in countries subject to UN sanctions

- Lending to holding companies.

b. Credit Assessment and Risk Grading

A thorough credit and risk assessment should be conducted prior to the granting of loans, and at least annually thereafter for all facilities.

Credit Applications should summaries the results of the risk assessment and include, as a minimum, the following details:

- Environment or social risk inputs

- Amount and type of loan (s) proposed

- Purpose of loans

- Loan structure (tenor, covenants, repayment schedule, interest)

- Security arrangement

- Any other risk or issue

- Risk triggers and action plan-condition prudent, etc.

Risk is graded as per Lending Risk Analysis (LRA), Directoriate of Co-operative Guidelines of classification of loans and advances.

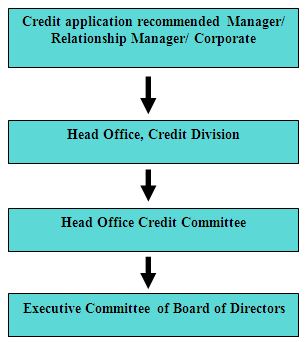

Program guidelines:

a. Approval process: The following diagram illustrates an example of the approval process:

- b. Credit administration: The credit administration function is critical in ensuring that proper documentation and approvals are in place prior to the disbursement of loan facilities.

- c. Credit monitoring: To minimized credit losses, monitoring procedures and systems should be in place that provides an early indication of the deteriorating financial health of borrower.

- d. Credit recovery: The recovery unit of branch should directly manage accounts with sustained deterioration (a risk rating of sub-standard or worse). The primary functions of recovery unit are:

- Determine account action plan/ recovery strategy

- Pursue all options to maximize recovery, including placing customers into receivership or liquidation as appropriate.

- Ensure adequate and timely loan loss provisions are made based on actual and expected losses.

TOOLS OF CREDIT MANAGEMENT

For credit management, a firm may use tools available to them. Such tools include Credit Risk Grading (CRG) and Financial Spread Sheet (FSS). Credit risk grading is an important for credit risk management as it helps the co-operative and financial institutions to understand various dimensions of risk involved in different credit transactions. The aggregation of such grading across the borrowers, activities and the lines of business can provide better assessment of the quality of credit portfolio of a co-operative.

The Lending Risk Analysis (LRA) manual introduced in 1993 by the Directorate of Co-operative has been in practice for mandatory use by the co-operative and financial institutions for loan size of BDT 1.00 crore and above. However, the LRA manual suffers from a lot of subjectivity, sometimes creating confusion to the lending Credit Manager in terms of selection of credit proposals on the basis of risk exposure. Meanwhile in 2003 end, Directorate of Co-operative provided guidelines for credit risk management of co-operative wherein it recommended, interalia. the introduction of Risk Grade Score Card for risk assessment of credit proposals.

Directorate of Co-operative expects all co-operative to have a well defined credit risk management system which delivers accurate and timely grading. In practice, a co-operative credit risk grading system should reflect the complexity of its lending activities and the overall level of risk involved.

Functions of Credit Risk Grading

Well-managed credit risk grading systems promote co-operative safety and soundness by facilitating informed decision-making. Grading systems measure credit risk and differentiate individual credits and groups of credits by the risk they pose. This allows co-operative management and examiners to monitor changes and trends in risk levels. The process also allows co-operative management to manage risk to optimize returns.

Use of Credit Risk Grading

- The Credit Risk Grading matrix allows application of uniform standards to credits to ensure a common standardized approach to assess the quality of individual obligor, credit portfolio of a nit, line of business.

- As evident, the CRG outputs would be relevant for individual credit selection, wherein a borrower or a particular exposure/ facility is rated. The other decisions would be related to pricing (credit-spread) and specific features of credit facility. These would largely constitute obligor level analysis.

- Risk grading also be relevant for surveillance and monitoring, internal MIS and assessing the aggregate risk portfolio level analysis.

CREDIT POLICY

Meaning of Credit Policy

Policy entails projected course of action One Finance MCS Limited has its own policy granting credit although credit is always a matter of judgment applying common sense in the light of one’s experience.

A sound credit policy includes among other things safety of funds invested vis-à-vis profitability of the co-operative. Encouraging maximum number of small loans is better than concentration in a particular type of advances, which ensures sufficient liquidity with least incidence.

Objective of Credit Policy

There are some objectives behind a written credit policy of One Finance MCS Limited that are as follows:

To provide a guideline for giving loan.

Prompt response to the customer need.

Shorten the procedure of giving loan.

Reduce the volume of work from top level management.

Delegation of authority of work from top level of management.

To check and balance the operational activities.

Formulation of Credit Policy

One of questions that should arise in a discussion of credit is who should formulate the policy. Although the ultimate responsibilities lay at the highest level in the organization i.e. the Board of Directors. Yet the actual drafting shall have to be done by the senior lending office in consultations with the chief executive officer and with contribution from senior officers, associates and subordinates. Obviously the level of origin will vary with the size and structure of the organization. The matter then referred to the board for approval after careful examination consideration and discussion.

Essential Components of a Sound Credit Policy There can be some variations based on the needs of a particular organization, but at least the following areas should be covered in any comprehensive statement of credit policy and One Finance MCS Limited policy also covers these areas:

1. Legal consideration: The co-operative legal lending limit and other constraints should be set forth to avoid inadvertent violation of co-operation regulations.

2. Delegation of authority: Each individual authorized to extend credit should know precisely how much and under what conditions he or she may commit the co-operation funds. These authorities should be approved, at least annually, by written resolution of the board of directors and kept current at all times.

3. Types of credit extension: One of the most substances parts of a loan is a delineation of which types of loans are acceptable and which type are not.

4. Pricing: In any profit motivated endeavor, the price to be charged for the goods or services rendered is of paramount without it, individuals have few guidelines for quoting retag or fees, and the variations resulting from human nature will be a source of customer dissatisfaction.

5. Market Area: Each co-operative should establish its proper market area, based upon, among other things, the size and sophistication of its organization its capital standpoint, defining one’s market area is probably more important in the lending function than in any other aspect of co-operation.

6. Loan Standard: This is a definition of the types of credit to be expended, wherein the qualitative standards for acceptable loans are set forth.

7. Credit Granting procedures: This subject may be covered in separate manual, and usually is in larger co-operation. At any rate, it should not be overlooked because proper procedures are essential in loan establishing policy and standards. Without proper procedure for granting credit and constant policing to ensure that these procedures are meticulous carried out, the best conceived loan policy will not function and inevitable, problems will develop.

Lending Guidelines As the co-operative have a high rate of non-performing loans. Co-operative risk taking applied should be contained and our focus should be to maintain a credit portfolio keeping in mind of co-operative capital adequacy and recovery strength. Thus co-operative strategy will be invigorating loan processing steps including identifying, measuring, containing risks as well as maintaining a balance portfolio through minimizing loan concentration, encouraging loan diversification, expanding product range, streamlining security, insurance etc. as buffer again unexpected cash flow.

Industry and business segment focus

Industry segment focuses on textile, pharmaceuticals, agro-based, food and allied, telecommunication, power generation and distribution, health care, entertainment services, chemicals, transport, infrastructure development, linkage industry, IT, ceramics, others as decided from time to time. And business segment focuses on distribution, brick field, rice mill/ flour mill/ oil mill, work order, yarn trading, cloth merchant, industrial spares, hardware, electronic and electrical goods, construction materials, fish trading, grocery, whole sale/ retail, others as dedicated from time to time.

PROGRAMS FOR LOAN RECOVERY

When One Finance MCS Ltd sanctions loans and advances to its customers, they clearly state the repayment pattern in the loan agreement. But some credit holders do not pay their credit in due period. The nationalized and private sector commercial co-operative have to face this sort of problems. This situation is, especially severe in One Finance MCS Ltd. To overcome the problem of overdue loan, the co-operative need take particular loan recovery program.

Recovery Programs to be taken by One Finance MCS Ltd

- To establish credit supervision and monitoring cell in the co-operative

- To re-structure the loan sanctioning and distributing policy of the co-operative

- To sanction loans and advances against sufficient securities as best as possible

- To offer a package of incentives to the sound borrowers

- To give more emphasis on short term loans and advances

- To impose restrictions on loans and advances for sick industries

- To take legal actions quickly against unsound borrowers as best as possible within the period specified by the law of limitations.

RECOVERY PATTERNS AND LOAN AND ADVANCES

Generally One Finance MCS Ltd sanctions loans and advances to every sector of an economy. Before going into details of recovery performance, we have to be familiar with some terms used in recovery performance:

Disbursement: highest outstanding balance on any date during the reporting period minus outstanding balance at the end of the preceding period.

Demand for recovery: overdue at the end of the reporting period plus recovery during the reporting period.

Recovery: highest outstanding balance on any date during the reporting period minus outstanding balance at the end of the recovery period.

Outstanding: Outstanding figures in the ledger at the end of the reporting period.

Overdue: Demand for recovery minus recovery.

PROBLEMS IN LOAN RECOVERY

There are a lot of reasons for which the loan recovery of the co-operative is very defective. In most cases. problems may be raised from sanctioning procedures of loan, investigation of the project, and investigation of the loans etc. that is, the problem in loan recovery proves the outcomes of the default process in loan disbursement. The main reasons of poor loan recovery are categorized in four broad types as follow:

A. Problems created by economic environment

The following problems arise from the effect of economic environment:

Changing in the management pattern: Changing of management patterns may delay the recover of mature loan.

- Changing in industrial patterns: The nationalized banks sometimes sanction loan to the losing concern for further improvement of the respective sector, but in most cases, they fail to achieve progress.

- Operation of open market economy: In our country mainly industries become sick and also close their business on account of emerging of open market economy. The cost of production is high and the quality of goods is not of required of standard. As a result, they become the losing concerns and the amount of bad loan increases.

- Rapid expansion of Business: There are many companies which expand their business rapidly, but the expansion is for short time. In the long run, the amount of classified loan increases.

Problems created by government

The following problems are arisen by the government:

- External pressure: One Finance MCS Ltd has also faced many problems in the loan recovery process as a part of continuous pressure from various interested groups.

2.Loan to government organization: One Finance MCS Ltd is bound to sanction loan to government organization, though these are losing concern. For this reason, co-operative faced problems in loan recovery.

3.Legal problems: Existing rules and regulations are insufficient to cover the legal aspects of loan recovery. As a result, defaulters can get release easily from all charges against them.

4. Frequent changes in government policies in regard to recovery of loan.

Problems created by the Co-operative:

The following problems are created by the co-operative:

- Lack of analysis of business risk: Before lending, One Finance MCS Ltd does not properly analyze the business risk of the borrowers and the co-operative cannot forecast whether the business will succeed or fail. If it fails to run well, the loan becomes classified.

- Lack of proper valuation of security or mortgage property: In most cases, co-operative fails to determine the value of security against the loan. As a result, if the loan becomes classified, the co-operative cannot recover its loan through the sale of mortgage.

Other general causes of poor loan recovery:

Apart from the specific reasons creating problems to recoup loan, there exists some other general causes which have a great impact on creating the problems which are faced by the One Finance MCS Ltd under study in the loan recovery process. These are:

- Early sanction and disbursement of loan to the borrowers without proper inspection of the project by the co-operative on account of pressure from lobbying group.

- Lack evaluation of technical and economic feasibility of the program.

- Delay in disbursement of credit.

- Credit is not allowed to actual entrepreneurs.

- Lack of proper supervision.

- Illiteracy of borrowers.

- Negative attitude of borrowers to repay the loan.

- Deterioration of the value system of the borrowers.

10. Money borrowers use their loan-money other than specified project, i.e., if the loan is sanctioned for industrial purpose; they use the money in house building or purchase of land for their own purpose.

11. Sometimes borrowers invest their money outside the country.

12. Many borrowers transfer loan money to abroad where they deposited this money in their own account or spent some other purpose.

13. Sometimes local borrowers are found to be so much compelled to grant them loan without proper study due to some unexpected reasons. Since these borrowers are capable of getting loan by exercising their influence, they can also escape the repayment liability.

14. Problems responsible for non-implementation and delayed implementation of project for which the entrepreneurs of the project cannot repay the loan. The causes of failure may be:

- Failure to ascertain the economic availability of the projects

- Time lag between approval and sanctioning of the projects

- Import of machinery and raw materials both are the problems of paucity of foreign exchange and procedures of licensing.

Discussions and Findings

Every co-operative has its own credit procedure. Co-operative under study possesses a standard credit procedure. As the objective of my study is to make a comment on the Credit Management of One Finance MCS Limited, I try my best to collect data for the study and find out the reality. Based on the data generated during my study period I will sum up my findings here and I think this will help me to achieve my objectives.

If we look at historical background of One Finance MCS Limited, we can see that, the objective of One Finance MCS Limited is to earn profit as well as to improve the economic welfare of the people as a whole.

One Finance MCS Limited has a significant role in long term project financing in both agriculture and industrial sectors. Again One Finance MCS Limited has a deep concern for rural farmers. Private sector usually concentrates in the urban areas where as public sector i.e. One Finance MCS Limited spread their co-operative network all over the world.

With a view to implementing government policies, One Finance MCS Limited has been maintaining its position in extending credit to government bodies, sector corporations and private enterprises.

According to the standard and co-operative credit procedure, credit operation is started from the customer application for the loan. But in most cases, many customers go directly to the directors of the co-operative and directors send them with his/her reference. In these cases, proper appraisal is not possible as directors the most powerful persons and co-operative management must give priority towards the decision of the directors. This phenomenon is very common in the co-operative which hampers the spontaneous procedure of credit appraisal.

According to the co-operative strategy, all co-operative must possess the standard policies which are designed by the Directorate of Co-operative One Finance MCS Limited also possesses a standard credit proposal form. In that form all necessary information are required to fill up. But in practice credit officers do not fill up the proposal form properly. Most of the cases, they use assumption rather than exact figure. This practice might end up with bad or classified one.

A standard policy starts from the customer’s direct application for the loan in the Head Office. But it’s a common phenomenon that most of the customers directly contact with Head office and Head office choose to disburse the loan. It hampers the normal procedure.

Every bank has its own budget and plan regarding loan portfolio. This loan portfolio must be diversified so that co-operative could diversify its risk. A proper and preplanned portfolio can eliminate the risk of huge classified loan or bad loans as this aspect is very much sensitive toward many external and internal factors. The co-operative under study i.e. One Finance MCS Limited does not have any proper guide line where to invest; moreover they do not do any future plan to maintain a well structured portfolio to decrease the possibility of classified loan. This type of practice is working as an obstacle in smooth credit disbursement as well as in credit appraisal system.

One Finance MCS Limited distributes loans without sufficient security in some cases. This is violation of the Directorate of Co-operative order.

In many cases co-operative face this problem because co-operative credit officer fails to value collateral property. Proper valuation means collateral will exactly cover the risk of bad loan. Officials must do it with due care.

The recovery performance of One Finance MCS Limited is not in a satisfactory level at all and the position of those in that respect deteriorated heavily during last two phases. The recovery performance in agriculture is worse than in other sectors. On the other hand, as private sector banks distribute more loans on short term basis and relatively better than public sector. But if we compare it from the efficiency point, then it is clear that they are not still efficient in credit management as they are unable to recover half of their distributed loan in different sectors.

One Finance MCS Limited does not keep enough provisions against classified loans and advances.

Private sector co-operative are relatively efficient in processing and executing legal actions against defaulters for their nonpayment of loans and advances in due time that of co-operative sector.

SWOT analysis

SWOT analysis is planning exercise in which managers identify organizational strengths (S), Weakness (W), Opportunities (O), and Threats (T). The SWOT analysis of One Finance MCS Limited are discussed below-

Strength

Strong base in reserve

Strong base in equity

Strong base in deposit

Goodwill in market

Modern Technology & Equipment

Stable source of fund

Largest network among co-operative

Strong liquidity position

Low cost of fund

The employee more than 30(Thirty) persons.

Weakness

In the organization, decision-making is more or less centralized at the top of the organization. The organization’s long centralized structure slowed decision making and its conservative orientation made managers reluctant to change

Lack of skilled manpower

There is no proper money market in the country and for that idle fund can not be utilized in the market

Lack of proper Rules & regulations for the governance of this co-operative

Lacks of modern money market instrument

Opportunities

As a Nationalized co-operative it get a lot of opportunities to serve co-operative activities. In the organization, one opportunity is sufficient fund management

Most of our people want to be risk free. They want to deposit their fund with interest in risk free organization. For this reason people initiate to deposit in One Finance MCS Ltd, which can help to achieve more profit and poverty elevation.

Increasing awareness of financing

Opportunities to develop Investment Instruments

Being large co-operative it can provide large investment.

Threats

In the Co-operative sector, the main threats for an organization is the rise of global organizations, that operate and compete in more than one country, has put severe pressure on many organizations to improve their performance and to identify better ways to use their resources

Market pressure for lowering the profit /interest rate

Dissatisfaction Pay-package of One Finance MCS Ltd employees is less enough in comparison to other Co-operative efficient manpower may switchover from the Co-operative which is also a threat for the Co-operative.

Conclusion

I have discussed so far about the different aspects of credit management One Finance MCS Ltd. For my report, I have selected One Finance MCS Ltd plays an important role in the Co-operative sector as well as in our economy. The success of a co-operative depends largely on the efficient credit management. A successful credit management is not only need for a co-operative own performance but also it is needed for the smooth development of an economy. In any strategy of economic development, therefore, it is essential to emphasize the evaluation of a sound and well integrated credit management system from the view point of both resources mobilization and efficient allocation of funds. In conclusion it can be suggested a number of recommendations in order to overcome the problems and how to remove the causes of problem in credit management.

Recommendations

The recommendation given are not decisions rather they are only suggestions to improve the default rate. The recommendations are made on the basis of survey findings.

- Directorate of Co-operative should take proper actions for ensuring equivalent distribution of loans and advances

- Lending policies in our country should be geared to growth potential rather than being determined by the pre-existing collateral

- Changes in lending policies will not suffice the purposes unless it is followed by a change in the attitude and out look of both the borrowers and the employee.

- Improvement of credit management depends on the development of relevant, adequate, proper and reliable data base at the co-operative as well as co-operative in Bangladesh

- For developing a reliable credit management system for the One Finance MCS Ltd, it should require to introduce as improved information system within co-operative as well as among the borrowers. Because ultimately it is what a borrower does with money that should guide the credit plan, the borrowers also have to know exactly where they are going, what their opportunities and how fast they can move

- Prompt legal actions be taken against willful loan defaulter

- The new entrepreneurs should be encouraged in disturbing loans and those who have the records of regular payment, should be given preference.

- Steps should be taken so that guarantors cannot avoid their responsibility

- It is observed that the defaulters generally get various sorts of exemptions as declared by the government from time to time. Government must not show any kind of mercy to the defaulters in any way which may encourage the default culture. This type of action may discourse the borrowers to become willful defaulters

- The attempt to encourage co-operative to require borrowers comply with co-operative laws and regulations and clear up industrial properties prior to granting a loan

- The attempt to encourage co-operative to require borrowers comply with co-operative laws and regulations and clear up industrial properties prior to granting a loan

- One Finance MCS Ltd should follow some straight ward mechanical procedures in assessing the risk of a borrower

- The formulation of a sound credit policy in the possibility of default loans.