Classification of Cost:

Classification of Cost is variety,it Costs may be classified on different bases. They can be classified as follows:

By time (historical, predetermined)

By nature of elements (material, labour, overhead)

By association (product or period)

By traceability (direct, indirect)

By changes in activities or volume (fixed, variable, semi-variable)

By function (manufacturing, administration, selling, research and development)

Controllability (controllable, non-controllable)

Analytical and decision-making (marginal, uniform, opportunity, sunk, differential etc.)

By nature of expense (capital, revenue)

Miscellaneous (conversion, traceable, normal, total)

Classification on the Basis of Time

Costs can be classified into historical costs and predetermined costs.

Historical costs: Historical costs are determined after they are incurred actually. When production is completed, i.e., products reached their final stage of finished status, costs are available and on that basis costs are ascertained. Only on the basis of actual operations, costs are accumulated. Hence they are objective in nature.

Predetermined costs: Costs are calculated before they are incurred, i.e., before the production process is completed.

These predetermined costs may further be classified into estimated costs and standard costs:

Estimated costs: Costs are estimated before goods are produced. As these are purely estimates, they lack accuracy.

Standard costs: These costs are also predetermined. But certain factors are analysed with care before setting up costs. Standard cost is not only a concept of cost but a technique or method of costing also.

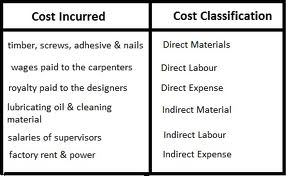

Classification by Nature or Elements:

Elements of costs may be broadly divided into material, labour and expenses.

Direct costs: In general, production is carried on in different cost centres. Costs which can be directly identifiable with cost centres, processes or production units are known as direct costs.

Indirect costs: If costs cannot be identifiable with cost centres or cost units, they are termed as “indirect costs”. Such costs that cannot be easily identifiable with cost centres have to be apportioned on some equitable basis. These terms should be understood properly, as the same will be applied in case of materials, labour and wages.

Material Costs:

Commodities or substances from which products are produced are called materials. They may be further divided into direct and indirect. The term “direct” means that which can be identified with and allocated to cost centres and cost units. The term “indirect” means that which cannot be allocated but can be apportioned to, or absorbed by, cost centres and cost units.

Direct materials:

Direct materials are those materials which enter into and form part of the product, e.g., wood in furniture, chemicals in drugs, leather in shoes. Direct materials include:

All materials specially purchased or requisitioned for a particular process or job or order

All components—purchased or produced

All materials passing from one process to another

All primary packing materials

Other Costs:

Normal cost:

This cost is incurred at a given level of output in the conditions that level of output is achieved.

Traceable cost:

This cost can be easily identified with a product or job or process.

Total costs:

It denotes the sum of all costs in respect of a particular process or unit or job or department or even the entire organization.