Where subsidiary books are being maintained in the organization, Cash and Bank transactions are recorded at the same place in a book called “Cash Book”. The Cash Book is maintained in a ledger account format. It has got a debit side as well as a credit side. Recording in this book is done exactly in the same manner as posting the journal entry into the ledger.

A Cash Book is a subsidiary book. It has the peculiarity of being both a journal as well as a ledger. If a transaction is entered in the Cash Book, both the recording aspect as well as the posting aspect are complete, i.e. it amounts to writing the journal entry as well as posting into the ledger.

We know that posting is to be done into two ledger accounts. Writing in the Cash book amounts to completion of posting in the ledger accounts within the cash book i.e. the Cash a/c and Bank a/c. Posting into the other account involved in the transaction has to be done and that cannot be assumed to be complete.

Bank Book

The handbook says forests “provide a tremendous source of natural capital that can be used to alleviate poverty.” It describes the pluses and minuses of Bank-supported community programs in countries like India and Mexico that seek to promote a balanced use of forest resources while improving the livelihoods of local people.

The General Ledger

The general ledger is a collection of the firm’s accounts. While the general journal is organized as a chronological record of transactions, the ledger is organized by account. In casual use the accounts of the general ledger often take the form of simple two-column T-accounts. In the formal records of the company they may contain a third or fourth column to display the account balance after each posting.

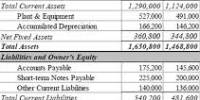

Balance sheet

A balance sheet summarizes an organization or individual’s asset, equity and liabilities at a specific point in time. Individuals and small businesses tend to have simple balance sheets. Larger businesses tend to have more complex balance sheets, and these are presented in the organization’s annual report. Large businesses also may prepare balance sheets for segments of their businesses. A balance sheet is often presented alongside one for a different point in time (typically the previous year) for comparison.

Income & Expenditure

This publication presents information about Canada’s National Economic and Financial Accounts (NEFA). These accounts portray the evolution of the Canadian economy on a quarterly basis. They record the components of income and expenditure, saving and investment, and borrowing and lending of each of four broad sectors of the economy: (i) persons and unincorporated businesses, (ii) corporate and government business enterprises, (iii) government and (iv) non-residents. Some information is also provided for sub-sectors of the second and third sectors. The sum of the final (non-transfer) income or the final (non-intermediate) expenditure of all domestic sectors equals gross domestic product at market prices, the market value of total production in Canada

Receipt for payment

A rent receipt is the only way that tenants can prove that they have paid the rent in case of a dispute. Several states also mandate that landlords must provide rent receipts for payments made by check or credit cards if requested by the tenant. You can accomplish this easily using the convenient and customizable Socrates Receipt for Payment of Rent for Alabama.

The profit and loss

The Balance Sheet is a snap shot in time of a company’s overall worth. The Profit & Loss Account (P&L) is a report of the company’s profit on the sale of their goods or the provision of their service over a trading period, normally one year.

Trade blance

Trade balance is usually decomposed by product and by country (bilateral trade balances). Relevant is the degree of concentration of the imbalance in trade caused by one or few commodities. If concentration is high, a targeted industrial policy could improve the balance (e.g. reduce the imbalance).On the other hand, if a deficit is due only to few partners, proactive and consensus-based trade negotiations with them could fairly quickly set the problem. Although less general than trade balance, which includes both goods and services, the “merchandise balance“, which includes only goods and not services, is sometime used because of better data availability.

The cash book is the final record of all the money that comes into and goes out of your business – often referred to as cashflow.

To complete your cash book, you’ll need to collect and hold on to:

- cheque book stubs

- cancelled cheques

- bank paying-in books

- bank statements

- copies of your own invoices

- receipts and delivery notes

- your suppliers’ invoices

- receipts for all cash purchases, till roles, etc

- remittance advices from customers

- copies of payments made or received using online banking systems

In both sections you should record the following:

Recording the type of expense will help you when filling in your annual tax return. Whether as a self-employed individual, or as a company, you will need to be able to distinguish between “allowable” expenses and “non-allowable” expenses. See our guide on business expenses and dispensations.

It is important to check the individual entries in your cash book with the bank statement to pick up items such as bank charges or credit transfers paid directly into your bank account for sales. If you pay by cheque, you should also check that these have been properly credited by your suppliers.

Small, simply structured businesses may find this cash book sufficient. However, keeping a sales ledger and purchase ledger will enable you to record sales, purchases on credit, and keep track of amounts owed to you from sales and by you for purchases. This will make it easier to monitor your cashflow.