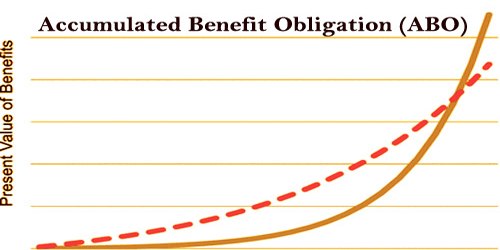

An accumulated benefit obligation (ABO) is an estimation of the present value of pensions or retirement benefits to which an individual is entitled when the current amount of compensation is used. ABO is calculated on the basis of the presumption that the pension scheme is to be discontinued immediately; no future wage increases are contemplated. ABO essentially calculates what quantity money the corporate would wish to pay currently retired employees in pension benefits. This varies from the projected benefit obligation (PBO), which implies that the scheme is continuing and thus accounts for potential rises in wages.

ABO is really used when a retirement or retirement savings account is to be terminated or when an employee stops working for the organization. Additionally, it calculates the number of advantages earned by current employees. In addition, it also takes account of their wages and time working for the company with existing employees. An accumulative benefit commitment is calculated purely at the existing level of compensation without taking into account any possible improvement that could arise. When used for a corporation, ABO is that the company’s amount of pension (retirement) plan liability at a specific time.

Accumulated Benefit Obligation (ABO)

An accumulated benefit obligation (ABO) is the present value of the sums agreed to be paid to workers after retirement by the pension scheme on the basis of cumulative work experience and existing wage levels (i.e. no possible pay increases) at the time of the calculation of pension liability. It does not take future wage raises into account. In comparison, the impact of potential wage increases is included in the Projected Profit Obligation (PBO). As at the time of calculation, ABO is also calculated by interest expenses, cost of services, and other factors prevalent in the sector.

Actually, ABO could be a measurement of pension liability taking under consideration the advantages for vested and non-vested employees at current salaries. ABO however doesn’t account for future increases, the worth of ABO and planned asset is compared at the time of valuation. PBO, on the other hand, takes into account compensation, including any potential wage rises, for vested and non-vested workers. Changes in the annual ABO are mostly due to changes in service rates, interest costs and plan participant payments, actuarial gains or losses, benefits accrued during the year, and where applicable, foreign exchange gains or losses. In situations where the planned asset is not exactly funded by the ABO or where the planned asset exceeds the ABO, the pension plan can be re-selected.

The assets of the plan can either be overfunded or underfunded by comparing the ABO to the value of the plan’s assets. An accumulated benefit obligation (ABO) calculates a company’s pension plan’s liability, assuming that the plan will end immediately. If ABO is more than the plan’s assets, then there’s a shortfall and also the program is underfunded. If the plan’s assets exceed ABO, then the pension account is overfunded. The value used for the employee’s benefits is the only discrepancy between the projected benefit obligation (PBO) of the company and its accumulated benefit obligation (ABO).

As ABO could be a present value calculation, there are two major drivers that determine if a thought is underfunded or overfunded. The discount rate used in the present value estimate and the estimated long-term rate of return on the assets of the plan are the two assumptions. While the ABO measure uses the current compensation of the employee, the PBO uses the expected retirement compensation of the employee.

Information Sources: