In response to regulatory pressure and the effects of rising interest rates, Wells Fargo is withdrawing from the multitrillion dollar U.S. mortgage industry.

The company will now concentrate on house loans for current bank and wealth management customers as well as borrowers in minority neighborhoods, CNBC has learned, instead of its earlier goal of reaching as many Americans as possible.

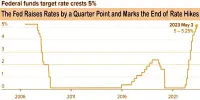

The decision was made as a result of two factors: a loan market that has fallen since the Federal Reserve started rising rates last year, as well as concerns about the company’s long-term profitability, according to consumer lending chief Kleber Santos. Regulators have heightened oversight of mortgage lending in the past decade, and Wells Fargo garnered further scrutiny after its 2016 fake accounts scandal.

“We are acutely aware of Wells Fargo’s history since 2016 and the work we need to do to restore public confidence,” Santos said in a phone interview. “As part of that review, we determined that our home-lending business was too large, both in terms of overall size and its scope.”

It’s the latest, and perhaps most significant, strategic shift that CEO Charlie Scharf has undertaken since joining Wells Fargo in late 2019. Mortgages are by far the biggest category of debt held by Americans, making up 71% of the $16.5 trillion in total household balances. Under Scharf’s predecessors, Wells Fargo took pride in its vast share in home loans it was the country’s top lender as recently as 2019 when it had $201.8 billion in volume, according to industry newsletter Inside Mortgage Finance.

More like rivals

Now, as a result of this and other changes that Scharf is making, including pushing for more revenue from investment banking and credit cards, Wells Fargo will more closely resemble megabank rivals Bank of America and JPMorgan Chase. Both companies ceded mortgage share after the 2008 financial crisis.

The shrinkage of such formerly significant enterprises has an impact on the mortgage market in the United States.

Our priority is to de-risk the place, to focus on serving our own customers and play the role that society expects us to play as it relates to the racial homeownership gap.

Kleber Santos

Following the catastrophe of the early 2000s housing bubble, banks withdrew from the home loan market, but nonbank businesses like Rocket Mortgage swiftly filled the hole. However, industry critics claim that because these emerging firms aren’t as tightly regulated as banks, customers may be at risk. Today, Wells Fargo is the third-biggest mortgage lender after Rocket and United Wholesale Mortgage.

Third-party loans, servicing

As part of its retrenchment, Wells Fargo is also shuttering its correspondent business that buys loans made by third-party lenders and “significantly” shrinking its mortgage-servicing portfolio through asset sales, Santos said.

For San Francisco-based Wells Fargo, the correspondence channel represents a sizable revenue stream that grew greater as total loan activity declined last year. The bank said in October that correspondent loans made up 42% of the $21.5 billion in loans it originated in the third quarter.

The sale of mortgage-servicing rights to other industry players will take at least several quarters to complete, depending on market conditions, Santos said. Wells Fargo is the biggest U.S. mortgage servicer, which involves collecting payments from borrowers, with nearly $1 trillion in loans, or 7.3% of the market, as of the third quarter, according to data from Inside Mortgage Finance.

More layoffs

Executives recognized that the change will result in a new round of layoffs for the bank’s mortgage operations, but they would not specify how many employees would be lost. As sales decreased last year, thousands of mortgage employees were fired or departed the company on their own will.

The news shouldn’t be a complete surprise to investors or employees. Wells Fargo staff have speculated for months about changes coming after Scharf telegraphed his intentions several times in the past year. Bloomberg reported in August that the bank was considering paring back or halting correspondent lending.

“It’s very different today running a mortgage business inside a bank than it was 15 years ago,” Scharf told analysts in June. “We won’t be as large as we were historically” in the industry, he added.

Last changes?

Wells Fargo said it was investing $100 million toward its goal of minority homeownership and placing more mortgage consultants in branches located in minority communities.

“Our priority is to de-risk the place, to focus on serving our own customers and play the role that society expects us to play as it relates to the racial homeownership gap,” Santos said.

Following the creation of a diversity section, the restructuring of the bank’s operations into five divisions, and the addition of 12 new operating committee members, the mortgage shift may be the final significant business reorganization Scharf will carry out.

In a phone interview, Scharf said that he didn’t anticipate making other major changes, with the caveat that the bank will need to adapt to evolving conditions.

“Given the quality of the five major businesses across the franchise, we think we’re positioned to compete against the very best out there and win, whether it’s banks, nonbanks or fintechs,” he said.