INTRODUCTION:The Bangladesh during the year 2002 faced the challenge of sustained while addressing the budget deficit and accommodative monetary policy. This resulted in erosion of foreign exchange reserve to an uncomfortably low level. The foreign exchange reserve held by Bangladesh Bank stood at US $1509.9 million at the end of November 2002 as against US $1788.6 million at the end of October 2002. During the month of December, the foreign exchange reserve had shown some improvements due to higher remittance from expatriates working in different countries of the world. During July to October 2002, the workers remittance increased by US $240.8 million or 32.94% and reached to a level of US $971.76 million as compared to US $730.99 million during July-October 2001.

To contain deterioration of foreign exchange reserves, Bangladesh Bank tightened its monetary policy and also temporarily imposed mandatory margin requirement on many importable items for domestic consumption. The Bank rate was lowered from 7% to 6% towards easing the high borrowing cost of investors in a low inflation environment. As a result, the commercial Banks in the country reduced their lending rates in a competitive market scenario. These measures enabled a higher credit growth of 13.90% in the private sector and 10.51% in the public sector of the country.

Broad Money (M-2) increased by Tk.5,679 million to 0.56% to Tk.1,021,548 million during October, 2002. During July to October 2002, the broad money increased by Tk.35,388 million or 3.59% with increase in the net foreign assets by Tk.9,237 million. Inflation measured in 12 months average increased the consumer price index which stood at 2.92% on September 30, 2002 compared to 2.35% in June, 2002. Domestic credit increased by 2.93% from July to October 2002. The increase was mainly on account of the private sector which contributed 3.76%.

According to Bangladesh Bureau of Statistics estimation, the real GDP growth slowed down from 5.3% of the financial year 2001 to 4.8% during the financial year 2002. The decline is mainly in agricultural sector contributing about a quarter of the GDP. In the industrial sector particularly in the small scale industries, there had been some gains in growth rate but large and medium scale manufacturing industries and other sub-sectors experienced lower growth. The weakness mainly arose from poor export performance.

The banking sector more particularly the private sector banks of 1st to 3rd generation made significant progress and growth in terms of specialized services through introduction of new products and switching over to electronic banking keeping pace with developed countries of the world. The 30 banks in the private sector made a total operating profit of Tk.13,140 million and growth rate was around 5% which might be termed ad encouraging in the backdrop of worldwide recession.

Bangladesh bank has been playing the all important role for bringing out the discipline and dynamism in the banking sector of the country. It has remarkably strengthened its supervision over the Banks. Reform programs to stamp out ills from the banking are also being implemented. Default-culture is seriously retarding the growth of the national economy. Due to stringent supervision and control being exercised by Bangladesh Bank, there had been a significant reduction in the percentage of classified loans in the banking sector.

1.2 OBJECTIVE

The primary objective of this part of the report is to make the reader familiar with the overall scenario of the banking sector as well as the organization itself. One of the major objectives of this part is to give an extensive view about the financial performance of the Southeast Bank Limited (SBL).

1.3 METHODOLOGY

In order to get he information about the organizational part, the main source that has been used is the primary source. In depth interview with the staff of different divisions regarding their job, their service, the products that they offer and various other things were gathered from them. Frequent visit and close interaction with the various divisions was very much helpful for the preparation of this report.

Some secondary sources were also used for the completion of this part. These includes

- Annual Reports of Southeast Bank Limited, Dhaka Bank, Prime bank, National bank.

- Different Magazines

- Papers

- Schedule banks’ Statistics

- Internet

- Other necessary books and materials

- Publishing of Ministry of Finance

1.4 SCOPE

The scope of this part is limited to the overall scenario of the organization. This part has covered the different divisions of Southeast Bank, the products offered by Southeast Bank Limited and the major functional areas of the bank. The present scenario of the banking industry is also covered in this part. A financial analysis of Southeast Bank Limited is also covered in this part.

1.5 LIMITATIONS

Like most of the banks, SBL also does not provide access to all kinds of information for secrecy purposes. Moreover, officials and officers are very much busy with their work to give required time. So, in some cases, observation and some extent of assumptions were needed.

Due to lack of job experience, faults may have arisen in the report though maximum effort has been given to avoid any kind of mistake or uncertainty in preparing this report.

Making a comparative study needs information from different leading banks of the country and getting those information from different banks is a very tough job in reality, because most of the banks do not provide information for study purposes to the students from different organizations and institutions.

Some of the information that were used are not recent as the latest information regarding those issues were not accessible and open to all. Only authorized person can get those information.

Time constrain was also one of the major limitations while preparing this part as the total report is quiet a long one so allocation of time to the organizational part was really short.

1.6 SIGNIFICANCE

The significance of this part is that it gives a good idea about the overall knowledge about the Banking sector. It also provides extensive idea about the organizational part of SBL and its performance in comparison with the industry performance and also to the private commercial banking sector of Bangladesh.

COMPANY OVERVIEW

2.1 COMPANY BACKGROUND

The emergence of Southeast Bank Limited (SBL) was at the juncture of liberalization of global economic activities. The experience of the prosperous economies of the Asian countries and in particular of South Asia has been the driving force and the strategic operational policy option of the Bank. The company philosophy – “A Bank with Vision” has been precisely an essence of the legend of success in the Asian countries.

Southeast Bank Limited, “A Bank with a Vision”, emerged as a 2nd Generation Commercial Banking Industry of Bangladesh in the year 1995. It was incorporated on March 12, 1995 as a public limited company according to the Companies Act 1994. The commencement of its banking business occurred on May 25, 1995 by the Principal Branch located at the Annex Building, 1Dilkusha Commercial Area, Motijheel, Dhaka. The Head Office of the Bank is also located at the same address on the 3rd floor of AnnexBuilding.

The Bank started with an authorized capital of Tk. 500 million and paid up capital of Tk. 100 million. Southeast Bank Limited started its business with the inaugural Chairman Mr. Mohammad Abul Kashem, Vice Chairman Mr. Ragib Ali and the first and former President and Managing Director of the Bank Mr. Syed Anisul Haq.

Southeast Bank Limited is a scheduled commercial bank in the private sector, which is focused on the established and emerging markets of Bangladesh. Southeast Bank Limited has 21 branches throughout Bangladesh and its aim is to be the leading bank in the country’s principal markets. The branches are situated in the prime business locations of Bangladesh. Among the 21 branches, 10 branches are in the capital city Dhaka, 4 in the port city Chittagong, 3 in Sylhet, 1 in Khulna, 1 in Moulvibazar. The other 2 branches are opened in 2003 and with Islami banking concept which are operating in Feni and Cox’s Bazar. The bank by concentrating on the activities in its area of specialization has achieved good market reputation with efficient customer service. The Bank is committed to providing continuous training to its staff to keep them up to date with modern practices in their respective fields of work. The Bank also tries to fulfill its share in community responsibilities. By such measures, the Bank intends to grow and increase shareholders’ earning per share. Southeast Bank Limited pledges to maximize customer satisfaction through services and build a trusting relationship with customers, which has stood the test of time for the last eight years.

SLOGAN:

“A BANK WITH VISION”

VISION:

To stand out as a pioneer banking institution in Bangladesh and contribute significantly to the national economy.

MISSION:

The missions of Southeast Bank Limited are as follows:

v High quality financial services with the help of latest technology

v Fast and accurate customer service

v Balanced growth strategy

v High standard business ethics

v Steady return on shareholder’s equity

v Innovative banking at a competitive price

v Deep commitment to the society and the growth of national economy

v Attract and retain quality human resources

2.2 STRATEGIES

Management Strategies: The deposit schemes of SBL include current, savings and fixed deposits. In line with other banks in the peer group, this Bank has also introduced several attractive savings packages like pension savings scheme, education scheme and savers benefit deposit scheme. SBL has a wide cluster of lending packages, which include commercial lending, working capital, house building loan, small medium and large scale industry loan, loan against export and other consumer loans. SBL has always been one of the major players in the country in promoting diversified banking services. Over the years it has provided sincere and timely services through the innovation of multifarious modern banking products. The major areas where SBL provides financing facilities are corporate banking, micro credit financing, investment in house building financing companies and various loan syndication. SBL has introduced SWIFT to facilitate quick fund transfer and Reuter to facilitate foreign exchange trading. With eight other banks this bank gives its customers the facilities of shared ATM services throughout day and night i.e. 24 hours banking.

The business strategy of SBL is to strengthen its traditional lending in small retail business, following a conservative lending approach in the areas of large and medium industrial ventures. The management approach of maintaining loan quality is also appreciable. Although Bangladesh economy is led by garments sector, it is worth nothing that he exposure of the Bank in this sector is negligible. Therefore, the existing depressed scenario of garments will have little impact on the Bank. The Bank is constrained by limited branch network. Realizing the importance of this network for its entity to low cost saving deposits, the Bank has taken a dynamic step for opening additional branches. Till such time having adequate branch network, the Bank needs effective communication system including advance online banking with the existing branch network for information flow as a part of its management strategy.

Marketing Strategies: As the bank has expertise in loan and club financing, SBL management wants to attract more corporate clients to avail their financing facilities of this nature in the years to come and thereby system the growth of the loans of this type. SBL also targeted small and medium scale entrepreneur (SMEs) in the coming years is in the process of signing with SEDF (South Asian Entrepreneur Development Fund) in collaboration with the World Bank and few other donor agencies for technical and training assistance. The Bank has a plan to explore the market in future through exposing several loan schemes in IT sectors and various SMEs. SBL’s export, import and guarantee businesses have been growing at a good pace since its inception. Although the figures shows that SBL has been doing pretty well compared to the peers, but it have to go a long way in the future to keep pace with the like banks.

2.3 ORGANIZATIONAL STRUCTURE

2.3.1 THE BOARD OF DIRECTORS

Southeast Bank Limited currently consists of 13 members and these are the people who have taken initiative to start the Bank in 1995. A brief introduction of each of the member is given below:

Mr. Azim Uddin Ahmed – Chairman

Mr. Azim Uddin Ahmed, a prominent businessperson and industrialist is the Vice Chairman of the Board of Directors of Southeast Bank Limited. He is the Chairman of Mutual group of Companies and firms and sole agent of “Dano” and “Horlicks” brand milk food in the country. He is founder Life Member and former Chairman of North South University, founder of Azimia Islamia Senior Madrasha, DulumaAzimHigh School, AliAkbarHigh School and also associated with different social organizations as founder and donor. He has contributed a lot for development of educational institutions in his village home. He was an active member of Executive Committee of FBCCI & DCCI for many terms and founder President of Bangladesh Indenting Agents Association. He is the Past President of Gulshan Club, Rotary Club (Dhaka North) and also an active member of other social service organizations.

Mr. Ragib Ali – Vice Chairman

Mr. Ragib Ali, a prominent industrialist, business entrepreneur and philanthropist is the present Chairman of the Board of Directors of Southeast Bank Limited. Mr. Ali is the pioneer in tea plantation in Bangladesh having more than seven tea gardens in Sylhet, Chittagong and Tetulia, North Bengal and he is one of the largest producers of tealeaves in the country. He is also the Chairman and Managing Director of Kohinoor Silicate Industries Ltd. and Kohinoor Detergent Factory, producer of JET Washing Powder known by its name throughout the country. He has contributed significantly for various social services and founded a MedicalCollege and 500-bed hospital and a University named as LeadingUniversity in Sylhet, constructed numerous Roads, Schools, Colleges, Madrashas and Mosques. He is the Founder President of Moulvibazar Chamber of Commerce and Industries and Founder of Sylhet Muktijoddha Kallyan Trust and also associated with NorthSouthUniversity, AsiaPacificUniversity, ContinentalHospital and other social services organizations in the country.

Mr. M.A. Kashem – Director

Mr. M.A. Kashem is a renowned industrialist and business entrepreneur of the country and is the founder Chairman of Southeast Bank Ltd. He is the Chairman and Managing Director of Mutual Jute Spinners Ltd. and JK Group of Companies. He is the former President of the Federation of Bangladesh Chamber of Commerce & Industry. He is a very successful exporter of the country and was awarded “The President’s Export Gold Trophy” consecutively twice for his contributions towards boosting export trade. For his valuable services in the field of industry, he was awarded CR Das Gold Medal. Mr. Kashem headed several Government, FBCCI, UNDP and EEC Trade Delegations to various countries of Europe, USA, Canada and Far Eastern region including China.

He is the Chairman of North South University Foundation and one of the Founder Members of North South University that is the first private university in the country. Mr. M.A. Kashem is associated with various social and philanthropic organizations and established many religious and educational institutions.

Mr. Yussuf Abdullah Harun – Director

Mr. Yussuf Abdullah Harun, a prominent industrialist and business entrepreneur of the country. He has a brilliant academic career and is a Chartered Accountant from England and Wales (FCA). Mr. Harun is the Vice President of SAARC Chamber of Commerce and Industry and Former President of the Federation of Bangladesh Chamber of Commerce and Industry, Director of Infrastructure Development Company Ltd. and Member, Board of Governors of North South University. Recently Government of Bangladesh has selected him to head the organization “Matching Grant Facility Management Board” as its Chairman to accelerate the pace of industrialization in the country. He is associated also with a host of companies in the country – manufacturing cement, edible Oil, PP Bag, particle board, C.R. coils, etc. as Chairman, Managing Director and Director. Besides, he is involved with many social and charitable organizations as donor and life member.

Mr. Mohammad Abu Tayub – Director

Mr. Mohammad Abu Tayub is a graduate from ChittagongUniversity and started his career as an importer and general merchant. After liberation when there was a crying need for setting up of industries in the country he took initiative to set up industrial projects in Chtitagong area and so far established 32 industrial units where about 6,000 people are employed. He has established industries for production of edible oil, particle board, polypropylene products, polytex yarn products, garments, leather, vanaspati, chemical sacks, containers, timber, beverage, tea, cement etc. He has established the biggest paper mill in private sector named as T.K. Chemical Complex Ltd. situated in Boalkhali, Chittagong. He is the Chairman and Managing Director of Chittagong Cement Clinker Grinding Co. Ltd., the largest and renowned cement factory in Bangladesh. He is the Chairman of T.K. Group of Industries at Chittagong. He is a well-known philanthropist of his area and has established schools, madrashas and hospitals at his village Mansha in Chittagong district. He is associated with numerous social and benevolent organizations as donor and life member.

Mr. Jalalur Rahman – Director

Mr. Jalalur Rahman is one of the leading shipping business entrepreneurs of the country. He is the Chairman of Dynamic Shipping Lines Limited, Orient Maritime Limited and Chairman and Managing Director of Magnet Associates Limited. Dynamic Shipping Lines Ltd. is involved in shipping agency, ship brokerage and stevedoring in the ChittagongPort. Magnet Associates Limited is in the business of trading of bulk commodities and industrial raw materials and specially in providing various turn-key industrial projects. Mr. Rahman is the Chairman of SSA Bangladesh Limited, a joint venture company between Orient Maritime Limited and Stevedoring Services of America (SSA) Inc, USA. Dhaka. Mr. Jalalur Rahman is a graduate from DhakaUniversity. He has established many schools, colleges and madrasas and is a regular donor to various educational institutions.

Mr. Md. Akikur Rahman – Director

Mr. Md. Akikur Rahman is the Vice Chairman of Bangla German Latex Company Ltd., a joint venture industrial enterprise for production of latex with German Collaboration having factory at EPZ, Savar. He comes of a respectable Muslim family of Sylhet and settled in England for business some thirty years back. He is engaged in catering and real estate business in London. An Indian Food Restaurant named Curry House Cottage in Surrey, U.K. wholly owned by him is in operation since 1982. He has shopping and housing complex in Bridge Street, Surrey, U.K. and also in Shibganj Bazar, Sylhet named as Moushami Shopping Complex.

Mr. Syed Shahid Ali – Director

Mr. Syed Shahid Ali is in catering business for more than three decades. He left for the United Kingdom 35 years back and had his early general education in London. He is the Managing Director of Mark International Ltd. of Hems Street, London doing import business with reputation. The company was established in the year 1985. He is also the owner of Freehold Commercial Properties at Golders Green, South Ever Banks, Contra Nitin Road, London. Besides hotel business, he is also in import, export and real estate business in London as well as in Sylhet.

Mr. M. A. Ahad – Director

Mr. M. A. Ahad comes of a respectable Muslim family of Roynagar, Rajbari, Sylhet. He left for England more than four decades back and had general education in London. He is British citizen by naturalization and is engaged in real estate business in London since 1963. He has commercial property at Cobham and Byfleet Surrey, London.

Mr. Mostori Miah – Directo

Mr. Mostori Miah hails from a respectable Muslim family of Sylhet. In his early years he went abroad and settled in U.K. and had his general education in London. He is engaged in catering, travel agency and real estate business in London and Bangladesh. He is the Chairman and Managing Director of Hotel Hill Town Ltd., Telli Haor, Sylhet. He has real estate in HighCroftGardens and Hanbury Street, London. He has a travel agency in London in the name of Janata Travel Agency.

Mrs. Jusna Ara Kashem – Director

Mrs. Jusna Ara Kashem is a Director of Mutual Jute Spinners Ltd. and Rose Corner Pvt. Ltd. She is also holding appreciable shares in associated companies, firms, and business establishments under the JK Group of Companies. She is a great exponent of education and is associated with a number of schools, educational institutions in her locality as donor and life member.

Mrs. Duluma Ahmed – Director

Mrs. Duluma Ahmed is the Director of Mutual Foods Products Ltd. and Mutual Trading Co. Ltd. She is also holding major shares of its associate companies. She is actively associated with a number of socio-cultural organizations in the country holding different positions of importance. She is the founder of DulumaAzimHigh School at Feni. Besides this, her contributions are spread out in many other institutions, mosques, madrashas, maktabs and schools of the area.

Mrs. Rehana Rahman – Director

Mrs. Rehana Rahman is the Chairperson of Knitex Dyeing and Printing Ltd., a 100% export oriented knitting, dyeing and printing factory. She is also the Managing Director of Bengal Tradeways Ltd, a concern engaged in deep tubewell drilling and real estate. She is the Vice-Chairperson of the Board of Governors of North South University. She is an active member of a number of social service organizations.

2.3.2 THE MANAGEMENT TEAM

The management of an organization is usually the main body that runs the business or operates an organization. The Management of Southeast Bank Limited is formed with executives with vast knowledge and banking experience. The hierarchy of the executive team of Southeast Bank Limited is as follows:

PRESIDENT AND MANAGING DIRECTOR

DEPUTY MANAGING DIRECTOR

SENIOR EXECUTIVE VICE PRESIDENT

EXECUTIVE VICE PRESIDENT

SENIOR VICE PRESIDENT

VICE PRESIDENT

FIRST VICE PRESIDENT

SENIOR ASSISTANT VICE PRESIDENT

ASSISTANT VICE PRESIDENT

A brief introduction of some of the members of the top management of Southeast Bank Limited are given below:

Syed Abu Naser Bukhtear Ahmed, President and Managing Director

Syed Abu Naser Bukhtear Ahmed joined Southeast Bank Limited as President and Managing Director on 30 May 2002. Prior to his joining Southeast Bank Limited Mr. Ahmed was with Prime Bank Limited as acting Managing Director since 22 November 2001. Mr. Ahmed had played a significant role in the growth and profitability of Prime Bank Limited during the last three years of his tenure with the Bank since 10 April 1999 and led Prime Bank Limited as a dynamic and progressive institution in the banking industry in Bangladesh.

Mr. Ahmed obtained his Masters degree in Business Administration (MBA) from the Institute of the Business Administration, University of Dhaka in 1969. He graduated from Notre DameCollege, University of Dhaka with a Bachelor of Science degree in 1967. Mr. Ahmed joined the State Bank of Pakistan, Central Directorate in Karachi as a Grade-1 Officer where he worked in numerous division viz. Policy, Implementation, and Inspection Wing of Banking Control Department. After the Independence of Bangladesh, he joined the Bangladesh Bank in Dhaka where he worked in the Banking Control Department and in the Board Secretariat Department.

Mr. Ahmed left the Bangladesh Bank, Dhaka in September 1974 and joined the U.A.E. Central Bank in Abu Dhabi. He held various positions in the Foreign Exchange Department, Internal Audit Department and Bank Supervision and Inspection Department in Abu Dhabi, Dubai and Sharjah. He was a member of Banking Supervision Committee, which was composed of the Senior Staff Members of the Banking Supervision and Examination Department and chaired by H.E. the Governor of the U.A.E. Central Bank. Responsibilities of the Committee included advising the Board of Directors in formulating policies and guidelines with regards to supervision of Banks and other financial institutions operating in the U.A.E. and promulgating laws relating to Banking Operations in the U.A.E. Central Bank. He left the U.A.E. Central Bank in September 1995, after completing 21 years of service with the organization.

Mr. Ahmed has had over 32 years of diversified Banking and Auditing experience including positions at the Central Banks of 3 countries viz. Pakistan, Bangladesh and the United Arab Emirates and two leading private Commercial Banks in Bangladesh viz. Arab Bangladesh Bank Limited and Prime Bank Limited. He has attended many Seminars, Workshops and Training courses in Bangladesh and abroad including programs such as Capital Adequacy and Solvency, Asset Liability Management Function, Evaluation of Management, Measurement of profitability System, Evaluation of Credit Risks.

Mr. Ahmed is the Vice President of the Institute of Business Administration Alumnae Association and a life member of a professional body – MBA Association and also member of various social and cultural organizations and clubs.

Mr. M. A. Muhith, Deputy Managing Director

Mr. M. A. Muhith started his career October 22, 1970 in United Bank Limited (later converted into Janata Bank, Bangladesh) as Grade II Officer. In the year 1983, he joined National Bank Limited at the initial stage of the Bank as Assistant Vice President and held various responsible positions. He was promoted to the position of Vice President in 1986 with the assignment of Regional Head, Sylhet Region. Subsequenty, upon promotion to the post of Senior Vice President, he was made the Manager, Foreign Exchange Branch, Dhaka. Mr. Muhith has joined Southeast Bank Limited as Senior Executive Vice President on September 01, 1998 and promoted as Deputy Managing Director with effect from January 01,2002.

Syed Imtiaz Hasib, Senior Executive Vice President

Syed Imtiaz Hasib obtained his Masters degree in Political Science from the University of Dhaka in the year 1975 and started his Banking career with the Bank of Credit and Commerce International (Overseas) Limited (BCCI) in September 1976. He was promoted as a Senior Manager Grade III in September 1989 and was holding the charge of the Main Branch of BCCI until its closure in July 1991. Mr.Hasib joined Eastern Bank Ltd. as First Vice President (later redesignated as Senior Vice President) since it’s opening and was posted as the Manager of its Principal Branch. In 1994, he took over the charge of the International Division. Mr. Imtiaz Hasib joined Southeast Bank Limited on May 15, 1995 as Senior Vice President and was subsequently promoted as Executive Vice President and Senior Executive Vice President effective from January 01, 1999 and January 01, 2002 respectively. Presently he is the Head of International Division of the bank.

Mr. Md. Mosharraf Hossain, Senior Executive Vice President

Mr. Md. Mosharraf Hossain, after obtaining a degree in Commerce from NazimuddinCollege in Madaripur in the year 1968, joined Eastern Banking Corporation Limited (renamed as Uttara Bank Limited after independence of Bangladesh) as a Development Officer. In 1983, he joined National Bank Limited as a Grade III Officer.

He joined National Credit and Commerce Bank Ltd. (NCCBL) in 1985 as Senior Principal Officer and was promoted to the position of Vice President and posted as the Manager, Agrabad Branch as well as the Area In-Charge.

He left NCCBL in 1996 and joined Southeast Bank Limited as Senior Vice President and Head of Agrabad Branch. He was promoted as Executive Vice President in January 1999 and Senior Executive Vice President effective from January 01, 2002. He is still serving in the same Branch.

Mr. A.K. Qureshi – Senior Executive Vice President & Company Secretary

Graduated from DhakaUniversity in the year 1961, Mr. A.K. Qureshi joined the then Commerce Bank Ltd. of Pakistan as Probationary Officer in the year 1964. He was absorbed in Agrani Bank after liberation when Commerce Bank Ltd. and Habib Bank Ltd. merged and was renamed as Agrani Bank. He worked in Agrani Bank for nineteen years in different areas of commercial banking activities. He joined the United Commercial Bank Ltd. as Assistant Vice President during the formative stage of the Bank in the month of March 1983 and held different responsible positions at Head Office and Branches. Joined Al-Baraka Bank Bangladesh Ltd. as Senior Assistant Vice President in the month of January, 1988 and was assigned with the responsibility to work as Secretary to the Board of Directors since joining. He was promoted to the position of Vice President in the month of January 1989. He joined the Southeast Bank Limited in January 1995 and all preliminary activities for establishment of the bank was entirely under his supervision. He was promoted to the position of Senior Vice President in August 08, 1996. In January 1999, he was promoted to the rank of Executive Vice President. He is the Company Secretary of the Bank since 1995.

Mr. Mahbubur Rashid, Senior Executive Vice President

Mr. Mahbubur Rashid, after obtaining an Honours degree in Commerce from DhakaUniversity in the year 1968, joined First National Bank of New York in Karachi on March 31, 1969 as an Executive Trainee. On resigning from FNCB, he joined Habib Bank Limited, Karachi as a Senior Officer on September 1, 1970. Worked in various branches at Karachi, Chittagong and Dhaka in different capacities including that of Manager of a number of Branches. After liberation, worked in Computer Division and International Division, Agrani Bank, Dhaka.

On September 16, 1976 he joined BCCI and worked at Chittagong, Dhaka and Hong Kong for fifteen years. He joined Southeast Bank Limited on May 25, 1995 as Senior Vice President. He was subsequently promoted as Senior Executive Vice President and is presently working as Head of Financial Control and Accounts Division, Head Office, Dhaka. He has been a guest speaker at different business schools and is an occasional contributor to national dailies.

HIERARCHY OF SOUTHEAST BANK LIMITED

PRESIDENT AND MANAGING DIRECTOR

DEPUTY MANAGING DIRECTOR

SENIOR EXECUTIVE VICE PRESIDENT

EXECUTIVE VICE PRESIDENT

SENIOR VICE PRESIDENT

VICE PRESIDENT

FIRST VICE PRESIDENT

SENIOR ASSISTANT VICE PRESIDENT

ASSISTANT VICE PRESIDENT

SENIOR PRINCIPAL OFFICER

PRINCIPAL OFFICER

EXECUTIVE OFFICER

PROBATIONARY OFFICER / MANAGEMENT TRAINEE

OFFICER

JUNIOR OFFICER

ASSISTANT OFFICER

TRAINEE ASSISTANT OFFICER

OFFICER (COMPUTER)

JUNIOR OFFICER (COMPUTER)

ASSISTANT OFFICER (COMPUTER)

COMPUTER TRAINEE

HEAD CASHIER

OFFICER (CASH)

JUNIOR OFFICER (CASH)

ASSISTANT OFFICER (CASH)

CASHIER TRAINEE

CASUAL STAFF (MESSENGER, TEA-BOY, HYGIENE, DRIVER, ETC.)

2.4 DESCRIPTION OF BUSINESS

Southeast Bank Limited offers full-fledged banking service including general banking service, foreign exchange business, investment service etc. The general banking service includes taking deposits. The different deposit accounts are:

Fixed deposit account

Savings deposit account

Special saving deposit account

Short term deposit account

Term deposit account

Current account

These account are mainly opened by middle and lower income groups, sole-proprietorships, partnerships, limited companies, clubs, societies and associates. There are other deposits that are offered by Southeast Bank Limited in order to expand its product range so that it can compete with the other banks. These deposits are as follows:

Pension savings scheme

Education savings scheme

Marriage savings scheme

Savers beneficial deposit scheme

General loan scheme

Consumer credit scheme

House building loan/Apartment loan scheme

The foreign exchange business includes issuance of Letter of Credit (L/C), Foreign Demand Draft (DD), Foreign Telegraphic Transfer (TT), Inward Remittance, Import and Export Financing etc. Investment services of the Bank includes Small Business Investment Scheme, Housing Investment Scheme, Small Transport Scheme, Transport Investment Scheme, Car Loan Scheme, Rural development Scheme and etc.

Major functions of the Bank are as follows:

Deposit: The prime function of the Bank is to collect money from the clients in the form of deposits. Different types of deposits accounts are open by clients to get different types of benefits from the account. In the deposit mix, the Bank earns most from fixed deposit. The other deposits that are performing well are savings deposit and current deposit.

Loans and Advances: The other major function of the Bank is to give loans and advances to the clients from the money that they collect as deposits. The main income of the Bank comes from the interest income that they earn from these loans and advances. The Bank offers different types of loans and advances to the clients from different purpose. Detail function of loan and advances are described in the project part of this report.

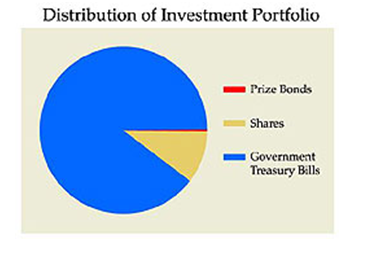

Investments: Investment is one of the other functions of the Bank that is common to all the Banking institutions. The investment portfolio of the Bank includes Government Treasury Bills, Prize Bonds and shares in Public Limited companies etc. The bank has always given emphasis on investment of Funds in highly yield areas simultaneously maintaining Statutory Liquidity Requirement (SLR) as fixed by Bangladesh Bank.

Treasury Operations: The treasury operations had long been considered as an important avenue of income generation for the Bank. The foreign banks operating in Bangladesh earn a considerable amount of their profit through treasury operations. With automated Reuters Terminal, the Bank has been able to develop its infrastructure capabilities for treasury dealings. The Bank has taken necessary steps for treasury dealings more adequately for meeting the demands of the customers.

FUNCTIONAL DEPARTMENTS

Southeast bank currently have 12 divisions that are functioning in full-fledged manner. Among these 12 divisions, recently the Bank has opened its new Islamic Wing that is working on the Islamic Banking of the Bank. The Bank has already started two Islamic Banking branches in July 2003 that are already doing business. The Bank also plans to introduce one new divisions namely Legal Affairs division. This new division will handle all the legal issues regarding the bank. Each of the division of the bank and their functions are discussed below:

6.1 Financial Control and Accounts Division (FCADs): One of the most important department of Bank or any institution is the Finance and Accounts Department. The main functions of this department are discussed below in a very brief manner.

- Budgeting

- Payment of salary

- Financial Analysis

- Disbursement of Bills

- Reconciliation:

- Provident Fund (PF), Gratuity, Superannuation Fund (SF):

6.2 Credit Division: The Credit Division of Southeast Bank limited is divided in two parts. (i) General Credit (ii) Corporate Finance.

General Credit: The functions of this division are given below:

- Analysis and appraisal/ evaluation of credit proposals for approval of Credit Committee

- Preparation of Board Memo

- Communication of Sanction Advice

- Preparation & Submission of periodical returns to Bangladesh Bank.

Corporate Finance: Under this division all the corporate credit like industrial credit, long-term project credits etc. are taken into account. SBL recently is trying to increase the amount of corporate loan portfolio although it has been seen that most of the other banks are concentrating mainly on consumer loans. The main functions of corporate credit division are

- Analysis, appraisal / evaluation of credit proposals

- Processing Credit proposals for approval of Credit Committee

- Preparation of Credit Information Memo (CIM) for Board

- Communication of Sanction Advice

6.3 Loan Administration Division (LAD): The major function of this department is to monitor the activities of the credit that are already disbursed. The functions of this department are

- Post Sanction documentation

- Monthly review and Follow up of Loan and Advances (LDO’s)

- Development of Early Warning System (EWS)

- Follow up for recovery of over dues.

- Classification of Loans

- Legal affairs/ Litigation

6.4 International Division (ID): One of the most important divisions of a bank is the International division. This is the department where the foreign exchange of the bank is maintained. Important works like L/C advising, collection of remittances are also done in this division. The functions of this department are

- To set up Agency Arrangement with correspondent Bank and to facilitate mutual exchange of business, document and information

- Remittance, for payment to beneficiaries.

- Letters of Credit, Advising, Confirmation, Negotiation, Acceptance, Payment, Bill, Cheque Collection.

- Guarantees, issuance of, including performance bonds, etc.

- Reconciliation of Nostro Accounts (Accounts with other foreign banks)

- Test keys / Specimen Signature Books for authentication of messages.

- Credit Lines.

- Extending and granting credit lines to correspondent banks for confirmation of their L/Cs, issuance of Guarantees, Money Market, FX Dealings etc.

- Obtaining credit lines from Correspondent Banks as above.

- Maintaining / monitoring record of credit lines obtained / utilized.

- Compile and circulate the foreign exchange circulars to the branches.

6.5 Human Resources Division (HRD): One of the most important departments of any organization is the Human Resources division because it has to deal with the whole manpower planning of an organization. The need of manpower, excess manpower, training to the staff and other works are all organized by this division. The functions carried out by the HRD of SBL are

- Recruitment, Selection of Manpower and Manpower Planning.

- Arranging and imparting training for Human Resources Development.

- Placement, Performance Evaluation, Increment, Promotion, Incentive Schemes etc.

- Processing of Leave.

- Disciplinary Action.

- Formulation / Implementation of Administrative Rules / Policies

- Preparation of Board Memo and Implementation of Board Decisions.

- Employees Service Benefits.

6.6 Information Technology Division (IT): Information Technology nowadays is a very critical part of any organization. To have upgrade knowledge about the world, advanced computer system in order to make the job more efficient and effective it is very important to have a good IT division. The functions of the IT division of SBL are

- Monitoring / Supervision of overall computerized banking operations.

- System Administration Data processing and Data Entry.

- Software Development and Maintenance.

- Maintenance of Hardware.

6.7 Logistic and General Services Division: The functions of the logistics division of SBL are very basic jobs. They are

- To arrange Printing & Purchase of Security / General stationery.

- To arrange efficient Utility Services.

- Maintenance of Premises

- Transport pool, Protocol etc.

6.8 Marketing and Outreach Division: One of the basic divisions of any organization is the marketing department. The world today is totally dominated by marketing. The stronger marketing strategy of an organization, the more successful is the organization. The functions of this division of SBL are

- Cost Benefit Analysis of existing banking products and development of new products.

- Liability Marketing.

- Branch Expansion.

- Mass Media and Event Management.

- To compile analyze and interpret key Management Information (MIS)

6.9 Branches Control Division (BCD): The functions of this division are as follows

- Internal Audit and Inspection.

- Compliance / follow up and monitoring of internal inspection.

- Monitoring of General Bank’s Inspection / External Audit Report.

6.10 Card Division: The card division of SBL is pretty new and small in the sense that not too many services by this division is offered to the customers. So the work of the card division is very much limited. The functions of the card division are:

- Managing debit card account and also credit card which is going to be introduced soon

- All the works that are related to the ATM card like managing the credit and debit balance of a client.

- Maintaining correspondence with the branches regarding different clients of ATM card.

- Works related to customer and vendor management.

6.11 Board and Share Division: The functions of this division are

- Arranging / conducting of Board, EC meeting.

- Preparations of minutes and implementation of Board decisions.

- Company affairs.

- Issuance of Bank’s share etc.

2.6 SWOT ANALYSIS

Internal Environment of Southeast Bank Limited

STRENGTH

Sound Profitability and growth with good internal capital generation.

High quality of asset.

Quality products.

Experienced and effective Management Team.

Better infrastructure facilities.

Good corporate culture and friendly working environment.

Board with financial flexibility

Very good reputation as a local bank

WEAKNESS

Small market share.

High concentration of fixed deposits.

Marginal capital adequacy.

Lack of effective marketing / promotional activities.

Lack of full-scale automation.

High concentration of large loans.

7.2 External Environment

OPPORTUNITIES

Scope of market penetration through diversified products.

Regulatory environment favoring private sector development.

Increasing trend in international business.

Introduction of credit card and Tele-banking.

Value addition in products and services.

THREATS

Increased competition for market share in the common banking arena.

Market pressure for lowering the lending rate.

Global and local unstable political situation.

Vulnerable Government regulations.

Multinational banks with good services.

Default culture all over the country.

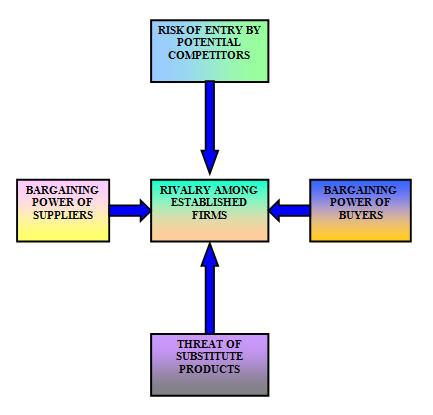

2.7 PORTER’S FIVE FORCES MODEL

Risk of entry by potential competitors: The financial sector of Bangladesh nowadays is growing more and more with the introduction of new financial institutions like leasing company, insurance companies and other. These companies may diversify into banks. So there is always an element of risk that potential competitors may enter into the banking sector.

Threat of substitute products: As it has been mentioned that the financial sector of Bangladesh is growing rapidly because of the new institutions that are coming up and creating an impact in the banking arena. These institutions like leasing companies, insurance companies ant others are performing the tasks of banks and offering the products and services that banks use to provide to their clients. As a result, these companies are working as a substitute in place of banks. So, in a way these companies are a threat to Southeast Bank Limited.

Bargaining power of suppliers: The suppliers of SBL are the people who provide different types of office equipment, furniture and other things that are required by the banks. The bargaining powers of the suppliers are in the lower end because there are lots of suppliers present in the market who supplies these types of products to different organizations. As a result the buyers that the bank have enough choice to compare between suppliers regarding price and quality.

Bargaining powers of buyers: The buyers of SBL are its clients who use to take loan, deposit their money and others. The bargaining power of the buyers here is quiet high as more and more banks are coming up and this has created excess supplies in the market and so the buyers have lots of option to choose from. So in order to attract and retain customers the banks have to compromise with the buyers.

Rivalry among established firms: There are lots of private commercial banks that are doing quiet well in this banking sector. 1st Generation banks like National Bank, City Bank, Al-Baraka Bank and etc., then 2nd Generation banks like Dhaka Bank, Dutch-Bangla Bank, National Credit and commerce Bank, Southeast bank which are already established in good reputed commercial banks along with other multinational banks and 3rd and 4th Generation banks have a rivalry among themselves. Southeast Bank Limited had to face this intense rivalry among these banks.

2.8 Future Prospects

Amid many challenges, adverse economic conditions and market scenario during the year 2002, the Bank maintained its growth trend through the indicators like profitability, asset utilization, network expansion and etc. Basing on convincing reasons, it is strongly believed that in the coming years also, the Bank would be able to sustain its earnings capacity and maintain a steady profit growth as profit iss the main thing at the end of the day.

To gain strength, the Bank has purchased a total floor space of 23403 sft. at Eunoos Trade center at Motijheel for its Corporate Branch. The Bank has also purchased other spaces at other places over Bangladesh in order to expand its network and business as well as making a strong customer base.

Southeast bank has already started its new product of Islami Banking which is supposed to better and the Bank aims to expand its Islami Banking to some to the other places over Bangladesh very soon. SBL is the first Bank in the country to use VSAT (Satellite Based Communication System) at all its branches over the country and thereby introduced the new product of “Realtime Online Any Branch Banking Service” for cash withdrawals, deposits, electronic fund transfer, balance inquiry, account statement etc. by customers. Bank is also making headway for introduction of credit card operations for clients. Bank intends to enter into agreement with reputed Exchange Companies in USA, UK and UAE for safe flow of foreign remittances into the country from Bangladesh expatriates working to those places.

Chapter-3 INDUSTRY ANALYSIS

3.1 COMPOSITION AND RECENT TRENDS:

There are currently 4 NCBs (Nationalized Commercial Banks), 7 Specialized Banks, 15 Multinational Banks, 20 PCBs (Private Commercial banks) (including 5 Islamic banks) and 21 Non-banking financial institutions operating in Bangladesh. The 20 PCBs hold 30% of the loans, and 28% of the deposits of the banking system.

A moderately expansionary monetary policy was pursued in 2000/2001 by the government of Bangladesh, with the objective of achieving a thrust in the economic activities, with controls on the price inflation.

With a significant increase in the overall agricultural production (mainly food crops) for the last three years at a low rate of inflation, effective demand has increased, especially in the rural economy. This was reflected in the substantial rise in the private sector credit, by 7.4% in the first half of 2001, and then by 16.9% in the second half of the year. Overall, domestic credit went up by 17.7% during 2000/2001.

To keep money and credit expansion within planned levels, the supply of reserve money was regulated during the year with auctions of government treasury bills of different maturities. Reserve money increased by 10.9% during the year. The faster expansion in domestic credit, with simultaneous slower growth of reserve money, was mainly due to the 14.9% decline of net foreign assets. The continued erosion of foreign assets has been a source of worry for the government, which has been attempting to control expansion of domestic credit, in order to arrest the erosion.

In order to arrest the declining trend of net foreign assets and gross foreign exchange reserves, a 50% LC margin requirement on all imports other than industrial raw materials and inputs was imposed, to discourage nonessential imports.

3.2 GENERAL PROBLEMS IN THE BANKING SECTOR:

- Random Govt. Policy Changes: Bangladesh Govt. time to time changes policies regarding banking operations and impose restrictions on different trade issues relating to banking business. Commercial banks have to readjust their policies in the changing environments. The problem of recent call money crisis can be mentioned as such an example

- Default Culture: This is the most common problem in our banking sector. This is practiced by some of the corrupted businessmen, which in turn creates liquidity problems. For the PCBs.

- Bureaucratic Red Tape: Banking sectors face this problem rigorously due to delay decision making on the part of central bank or relevant ministry of Government.. This hinders banks from taking quick decisions regarding any sort of policy applications.

- Failure to gain confidence among mass people: Most of our compatriots are not well educated. In the grass route level, they rely on the nationalized commercial banks despite of their poor services. The mass people still rely heavily on the NCBs not only for their wide networks compared to PCBs but also from the phobia that the PCBs may collapse.

- Government hostile policies towards newly establish banks: Government policies towards the 3rd and 4th generation banks are not congenial to their operations. Governemnt decisions for withdrawing funds from these banks is such an example for this.

- Foreign bank’s strong financial and operational base: this is no doubt that the foreign banks are performing well in terms of their service quality due to their sound financial strength, market research and variety of product offerings. PCBs with their limited strength and capabilities working hard to compete side by side.

- Nepotism: As a part of overall financial system, PCBs are not out of this trend. This is sometimes reflected in their poor service quality.

- Director’s undue influence: This is such a problem, which is always overlooked. The directors very often intervene in the activities of the management, which in turns results in the delay implementation of decisions.

- Liquidity problems: Many of PCBs, mainly the recent ones faces liquidity crisis time to time in their daily operations. This is happened not only due to their unsound financial structure, but also for the fluctuating applications of monetary and fiscal policies.

- Lack of two-way communication system: In fact, most of the PCBs are too conservative. The creativity is not encouraged in many cases. For this reason, the PCBs are confined in the circle of conservatism. The new ways of thinking are discouraged very often.

- Delay in decision making in terms of loan sanction and selection of customers: Still now, the process of selection of appropriate clients and loan sanction process, is so lengthy. This Discourage the potential clients very often. It should be smoothen.

- Lack of freedom in operational activities: the operations of PCBs are very tightly monitored by the Bangladesh bank. It imposes restrictions on the free movements of the sector.

- Growth of Leasing Sector: Govt. recent policies encourage the massive growth of leasing sectors that pose threat to the leasing operations performed by some of the banks. The leasing companies urge Govt. to allow them to perform general banking activities plus to put restrictions of leasing services performed by the banks.

- Disorganized Capital / Share market: Share market of Bangladesh is not fully organized yet and subject to undue fluctuations. The banks operating in the capital market faces real problems due to massive fluctuations in terms of share prices and which in turn reflected in their dividend declarations

- Lack of Govt Support: Govt plays a dual role in this case. Govt is talking about financial sector reform in one side, and poses various restrictive policies on the operation of commercial banks on the other.

3.3 BANKING SECTOR FOCUS:

Some modifications in loan classification and loan default criteria were brought about during the year.

The overdue accounts that were previously termed as “adversely classified” were changed to the status of simply being “overdue”. This step was taken by the after the last elections, where many of the overdue account clients were listed as defaulters. As per the revised criteria, continuous, demand and term loans would be overdue from the day immediately after the repayment date of the loan/installment. Term loans for over five years, short-term agricultural loans and micro credit will be overdue after six months from the repayment date.

The period after which an overdue loan would be adversely classified, was extended by three months, when it would become “substandard”.

In all the above cases, the borrower will be treated as being on loan default after six months from the date on which the date on which the loans became overdue. This means that they will be considered loan losses after twelve months from the repayment date.

In order to ensure integrity in the determination of net profit and value of assets shown in the balance sheets of scheduled banks, the government placed certain regulations. Policies were issued requiring treatment of the difference between the book and market value of shares and debentures of private enterprises. Banks were asked to create provision against investment-related losses, as other assets.

The gross proportion of defaulted loans of scheduled banks as percentage of total loans declined from 39.7% to 33.7% over 2000/2001, as a result of constant attention to portfolio management and credit discipline.

Net investments in different government saving schemes by the public increased by 30.4%, reflecting increased demand for financial assets.

As per the Bangladesh Bureau of Statistics (BBS), gross domestic savings increased by 6.94%, and gross investment increased by 7.24%.

To summarize the monetary and credit situation, domestic credit rose by 17.65%, exceeding the expectations of growth of 14.44%. Private sector rose by 16.87%, compared to expectations of 13.08%. Time deposits also rose, by a substantial 18.12%. In the reserve money situation, loan reserves went up by only 1.85 %, compared to expectations of 7.27%. Bank credit went up by 18.1%, compared to previous year’s increase of only 10.3%. Of the components of credit, advances went up by 16.5%, while bills purchased and discounted went up by 55.2%.

The credit/deposit ratio of scheduled banks went up from 0.72 to 0.76, at the end of 2001. Scheduled banks’ borrowing from Bangladesh Bank went up by 1.8%, while their balance with Bangladesh Bank went up by 13,6%, in the fiscal year 2000/2001.

The Cash Reserve Ratio (CRR) was held constant at 4.00% of total demand and time deposits. The Statutory Liquidity Reserve (SLR) of the scheduled banks remained unchanged at 20% of total demand and time deposits. The remaining 16% was assigned to investment in liquid securities, held mostly by the Bangladesh Bank in the form of T-bonds, at relatively low yields. The Bank Rate remained unchanged at 7.0% throughout the year. In order to discourage concentration of a major share of the bank’s credit with a small number of individuals/groups and limit risk exposure, ceilings on disbursement of large loans were prescribed, from October 2000.

A comparative analysis of changes in market shares are shown below:

| Bank Category | Percentage share in deposits | Percentage share in credits | ||

| 2000 | 2001 | 2000 | 2001 | |

| NCBs | 54.50 | 52.66 | 47.55 | 45.47 |

| PCBs | 31.43 | 33.60 | 30.34 | 34.90 |

| Foreign Banks | 7.76 | 7.15 | 6.11 | 5.80 |

| Specialized Banks | 6.31 | 6.59 | 16.00 | 13.83 |

PERFORMANCE ANALYSIS OF PCBs

In the process of preparing the material as we could locate very few studies as of now have been made on the role of: Private Commercial Banks in Bangladesh. In this situation – attempts have been made to compile and interpret data on the basis of the available information

10.1 Deposit, Advance, Capital and Reserve: From the study of a publication of the Ministry of Finance (MoF), Government of Bangladesh (GoB), this is observed that the PCBs made sizeable contributions towards registering positive growths in the key performance indicators. In course of review and to elaborate – PCBs in 1996 recorded a Capital and Reserve position of Tk.6,768 million, Deposit Tk.1,33,997 million, and advances Tk.97,627 million the corresponding figures of these in 1999 reached to Tk.15,100 million, Tk.2,19,660

million and Tk.1,56,136 million registering Capital and Reserve growth of 32%, Deposit growth of 18% and Advance growth of 17% during the period. In 1996 the PCBs handled Foreign Exchange Business of Tk.160,274 million that doubled in 1999 to Tk.324,149 million showing the average growth of 27% in Foreign Trade Business.

This may be observed that the second generation PCBs, on an average, has relatively higher performance growth records in respect of key indicators compared to the first generation PCBs. The main reason may be attributed to higher operational returns from investments and also that the first generation PCBs required increasing quantum of bad debt provisioning from the operational revenue. The newly set up (Third generation) PCBs, however, are yet to come up with reasonable performance standard excepting a few of these Banks.

In consultation from the similar study, this is revealed that the deposit base of PCBs in 1990 was Tk.59,880 million that stood at Tk.163,360 million in 1998 as against total Bank deposit of Tk.232,580 million in 1990 and Tk.592,310 million in 1998. The PCBs reached an advances (LDOs) figure of Tk.48,670 million in 1990 and Tk.136,520 million in 1998 as against the aggregate Bank advances (LDOs) of Tk.222,510 million in 1990 and Tk.508,740 million in 1998.

In the entire period 1990-98, PCBs recorded an annual average deposit growth of 13.49% and advance growth of 14.05%, the corresponding figures of these are 12.42% and 11.06% for the entire Banks. The percentage growth is 11.83% and 10.67% in case of NCBs and 15.18% and 11.74% in case of FCBs. The above position explains comparative intermediation edge of PCBs on NCBs in respect of deposit and advance growth rates. The PCBs have better advance (LDOs) growth rates compared to FCBs. In the periods of 1996-99, the average funding / deposit utilization ratio (Advance / Deposit ratio) of first and second generation PCBs are found to be 73% and this indicates that there still exists further scope for optimum utilization of funds towards profitably channelising in investment pursuits. The 3rd generation PCBs, being newly set up, have underutilization of fund to a greater extent. The comparative study, however, shows that PCBs and FCBs have better utilization of funds compared to the NCBs.

In 1990, PCBs share in the aggregate deposit and total advance were 26% and 22% respectively, these in 1998, increased to 28% and 27% representing gradual increase in market share of PCBs in deposits and advances (LDOs).

10.2 Geographical Distribution of Deposits and Advances: The share of Dhaka and Chittagong divisions in total deposits of PCBs was 79% (Dhaka 58%, Chittagong 21%) in October ’99 and other 4 (Four) administrative Divisions contributed only 21% (Khulna 4%, Rajshahi 5%, Barisal 2% and Sylhet 10%). The share of first 2 (Two) divisions in total advances of PCBs was 89% (Dhaka 68% and Chittagong 21%) and only 11% by the rest 4 (Four) divisions (Khulna 5%, Rajshahi 3%, Barisal 1% and Sylhet 2%) as on 30-09-1999. These indicate that mobilization of deposits and disbursement of loans by PCBs have in effect been concentrated in Dhaka and Chittagong divisions and the remaining 4 (Four) divisions are having less access to credit compared to the respective shares in deposits that speaks of regional weaknesses of business / investments and economic activities. The similar scenario prevails in case of NCBs and FCBs.

In the year 1999, the PCBs accumulated around 9.5% of the total deposits from rural areas (29.4% for NCBs) out of that extended credits of a negligible portion of deposits that is 2.2% (18.5% for NCBs), indicating that of nature of flow of resources from the rural to the urban areas of the country. The segmentation of markets for Banks have been made clear, that is, NCBs have developed better strength in the non-urban and rural segments of the economy over the PCBs.

10.3 Deposit Mix: The Fixed / Time deposits constitute 45% for the PCBs’ total deposit whereas current deposit constitutes 19%, savings deposits 27% and short term deposits (STD) 9% as on September 30, 1999. The similar picture prevails in case of NCBs and, FCBs comparatively mobilized higher quantum of deposit in current accounts (26%) and lower volume in fixed deposits (FDRs) (39%) that in other words explains the base for lower cost deposit mix for FCBs compared to that of the NCBs and PCBs.

10.4 Network of Branches: The PCBs had a total of 1,153 Branches in 1998 representing 19% share in total branch network in the country as against 61% share held by NCBs, 19.60% by SFIs and 0.48% by FCBs. In 1988, the PCBs share in branch network was around 14.14%, that was 65% in case of NCBs. The NCBs have the largest branch network and nevertheless the PCBs branch expansion has taken place at a faster rate.

10.5 Sectoral Distributions of Advances: In analysis, covering the sectoral distribution of advances (LDOs) – PCBs concentrated in trade sector and made 45.40% of advances in this sector (25% for NCBs) in 1999, PCBs share in industrial Term Loan and working capital financing constitutes 27.50%, that is 45% in case of NCBs. The PCBs are lagging behind in financing agriculture and agribusiness (1.47%), the main reason as may be observed is that the PCBs have poor connection to the rural economy because of the slower expansion of the rural branch network.

10.6 Employment Generation: The PCBs have created good employment opportunities for fresh, bright and educated young generation of the country. The increase in the number of Banks and Bank-Branches and the gradual increase in the volume of businesses- fresh avenues for employment have been opened up for the educated and well-groomed group. We may cite that in 1988, the PCBs had manpower strength of 14,810 and that stood at 22,526 in 1998 representing 22% of total banking employment as against 61% employment in NCBs, 16% in SFIs and 1% in FCBs.

10.7 Foreign Trade Finance: The PCBs share, in import business and import refinancing was higher compared to the combined businesses of the financial intermediaries (Banks) in the country. The share in import trade was 50% for the PCBs in 1998, that was 34% for NCBs, 13% for FCBs and mere 3% for the SFIs. In export financing PCBs share is increasing day by day that was 22% in 1990 and came to 35% in 1998 and maximum disbursements were made in the exports of readymade garments sectors that stands at was 69% of the total exports handled and routed through the PCBs.

10.8 Profitability: The PCBs generated an operating profit (income – expenditure) of Tk.4,748 million in 1999 as against Tk. 2,313 million in 1996, recording an annual operating profit growth of 27%. In the periods covering 1988-98, the PCBs had earned an average annual net profit (after Tax) of Tk.575.10 million that was Tk.142.60 million for NCBs, Tk. 683.50 million for FCBs and a net loss figure of Tk.1844.80 million in case of Specialized Banks. The PCBs average annual net profit growth during the period was 16.76%, that was 34.57% for FCBs. The average annual profit growth, however, was negative in case of NCBs (-6.58%) and Specialized Banks (-235.49%). The PCBs and NCBs had net loss situations during the period 1990-93. The situation arose because of implementation of the reforms measures – the result of introduction of the loan classification standards and provisioning in 1989 by the Central Bank for that the Banks were not allowed to accrue interest on classified loans and had to make provisions for NPAs : substandard / doubtful and bad loans – having significant impact on Banks interest income and capital. The profitability data as above signifies that PCBs and FCBs have operational efficiency compared to that of the NCBs. The study of net profit per employees during the period of 1984-1997 reveals that though FCBs have the best performance records but for PCBs per employee net profit was higher than that of NCBs.

10.9 Financial Discipline Capital: In compliance par the revised policy decisions suggested by : FSRP, Commercial Banks need to maintain capital structure minimum of 8% and out of that minimum 4% as core capital based on the Risk Weighted Assets (RWAs). The shift in policy decision to Link Capital from liability approach to asset approach is a major breakthrough in Bangladesh to raise the Local Banks in reaching to the level of the international standards.

This is observed that, though PCBs initially failed to comply with the capital requirements and subsequently could maintain the capital adequacy – these signifies good financial discipline ensuring protections of depositors interests and the value for the shareholders having sound health for the Banks. In course of elaboration: in 1996 PCBs total capital was 80% of the required capital and that came to 110% in 1998, indicating marked improvement. The NCBs, however, could maintain 81% of capital requirements and that was 168% in case of FCBs during the year 1998.

FINANCIAL PERFORMANCE ANALYSIS OF SOUTHEAST BANK LIMITED

11.1 Analysis of the Financial Statements

Income statement: The main thing in the income statement is the income and the expense of an organization. In the banking sector the majority of the income comes from the interest and then from other investments made by the bank. Southeast Bank Limited a suggested by the income statement gives a clear idea of how the income and the expense are behaving for the last four years.

It shows that its income is always higher than the expense which is definitely a positive sign for the Bank. Its income is gradually increasing and simultaneously the expense is also rising due to the increase of business. Due to the healthy position of its net income after tax, the Bank is able to pay dividends to its shareholders and even keep some amount of money as retained earnings.

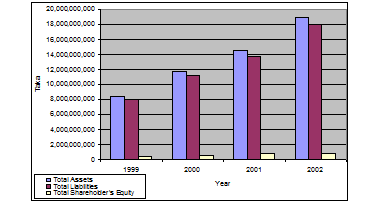

Balance Sheet: The balance sheet of SBL shows that it has pretty strong asset position. It is also financed heavily with debt and this is because it is a common characteristic of every banking institution to be financed more with debt. This happens because it has deposits that is a liability for the bank. SBL on an average has approximately 95% debt finance while the rest financed by the shareholders that is equity financed. Although the fixed asset of the Bank has decreased than before, but the current assets and other assets have gradually gone up which ultimately made the total asset to gone up. As bank is a service-oriented company, it does not need huge amount of fixed assets, but it needs to have healthy position in its current assets which Southeast Bank does possesses.

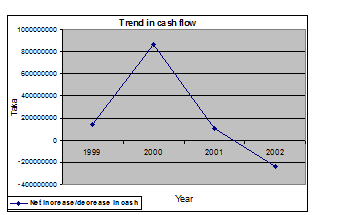

Cash flow Statement: The cash flow of the Bank shows that SBL has a good healthy cash inflow from operating activities for the last four years. The investment activities shows that for the last four years the Bank has a cash outflow from investment activities and this is mainly because the Banks has been investing a lot of money in different places like securities, deposit accounts and etc.

The Bank in the last four years had a cash inflow from financing activities only in the year 1999 due to the deposit of share money. Except that the Bank is having cash outflow from financing activities due to the payment of dividend to the shareholders of the Bank. The Bank had a net cash inflow for most of the time but in the last year the bank experienced a net cash outflow due to the cash outflow from investing and financing activities. The huge amount of investment in securities and other places and the large payment of dividend is the main reason behind this net outflow of cash during the year 2002.

Vertical Common Size Income Statement: From the vertical common size income statement, it can be seen that the percentage of income expense of the interest income over the four years have been going down, which is a good sign for the Bank considering the fact that the Bank is able to spend less on interest on the different kinds deposits. This has ultimately increased the net interest margin of the Bank.

Although the Bank has been experiencing increase in the net interest margin, the non-interest income has been going down due to the percentage increase in non-interest expense.

Expect these tow things all the other things like provision for loan loss, tax and other things has been quiet the same and the net income after tax on an average is approximately 16.5% of the interest income.

Vertical Common Size Balance Sheet Statement: From the vertical common size balance sheet statement it is found that the cash position of the Bank as a percentage of the total asset is more or less on an average is 12% which if compared with some other PCB is quiet in the lower end. The investment securities of SBL shows that, the Bank is concentrating quiet a bit on its investment securities because the portfolio of investment securities is quiet high than some other banks. On an average, it is found to be close to 12% of the total asset over the last four years. As mentioned earlier, the majority part of the asset of a bank comprises of loans and advances. So the loans and advances of SBL shows that on an average it has been maintaining an average of about 63.5% of the total asset which seems to be in the higher side because most of the PCB seems to have lower percentage of loans and advances. This makes the Bank to possess less other assets which is around 2.5% of the total asset while other banks seems to have it around 6-7% on an average.

It is also mentioned that the every bank is debt financed by almost 90-95% and the majority of the liability comes in the form of deposits mix. Southeast Bank Limited is debt financed by almost 95% whose deposit comprises of almost 70% on an average of the total liability and equity position of the Bank. The other 15% of the liability comes from non-deposit borrowings and other liabilities. But on the other hand, some of the PCBs deposit is only about 55% of the total liability and equity, although its debt finance is more than equity part. The rest of the liability comprises of other liabilities and only about 3% comes from equity financing. Due to the perfect mix of assets, liabilities and equity, the Bank is able to operate pretty smoothly till now.

11.2 Ratio Analysis

11.2.1 Value to Shareholders:

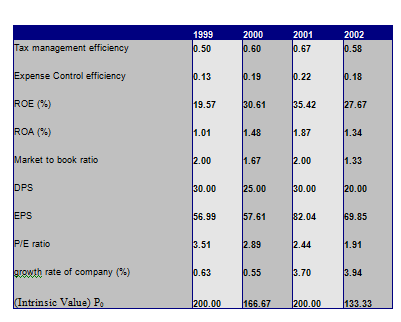

The key objective of any bank is to maximize the value of its shares, which represents their obligation to the shareholders, for the use of their equity. Share performance becomes an important indicator of their overall efficiency, as it is publicly traded. A bank that has low earnings capacity cannot provide shareholders with value, whether in dividends, or in high share prices. A close look at the dividend trend shows us that SBL dividend per share has been more or less in a stable position for the last 4 years.

| 1999 | 2000 | 2001 | 2002 | |

DPS | 30.00 | 25.00 | 30.00 | 20.00 |

EPS | 56.99 | 57.61 | 82.04 | 69.85 |

| (Intrinsic Value) Po | 200.00 | 166.67 | 200.00 | 133.33 |

The earnings per share have been rising from 1999 until 2001 which again dropped in the last year. It is thus, not surprising that SBL’s share price has followed somewhat stable position but in the last year it fell again although the Bank is earning well.

Another aspect of shareholders’ value maximization is the Return on Equity which gives further light to the performance measure of a bank The ROE of SBL for the last 4 years is as follows:

| 1999 | 2000 | 2001 | 2002 | |

| ROE (%) | 19.57 | 30.61 | 35.42 | 27.67 |

The rate of return flowing back to SBL’s shareholder, it can be seen that Return on Equity has been growing from 1999 till 2001 and in 2002 it fell again due to the fact that the income in 2002 was less than the previous year and more shares have been issues in 2002 which ultimately increased the equity portion of the Bank.

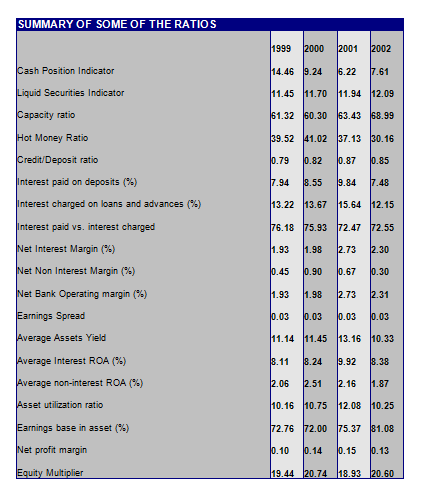

11.2.2 Interest Spread:

In order to look closer into the efficiency of SBL, one of the major factors behind its success, focus must be given to other aspects.

| 1999 | 2000 | 2001 | 2002 | |

| Net Interest Margin (%) | 1.93 | 1.98 | 2.73 | 2.30 |

In order to measure the spread between interest revenues and interest expenses, the net interest margin of the Bank must be focused. From this it can be seen that they have been able to raise the spread over the years. This reflects that in this competitive environment of the banking industry, SBL has been able to control its asset earnings, as well as its liability costs. This can be seen again in the table below:

| 1999 | 2000 | 2001 | 2002 | |

| Interest paid on deposits (%) | 7.94 | 8.55 | 9.84 | 7.48 |

| Interest charged on loans and advances (%) | 13.22 | 13.67 | 15.64 | 12.15 |

It can be clearly seen that, over the years, SBL has faced considerable pressure in terms of rising interest rates on deposits which they have efficiently managed to cope up with charging higher interest rates on loans and advances. The table below reconfirms this suggestion.

| 1997 | 1998 | 1999 | 2000 | |

| Interest paid vs. interest charged | 76.18 | 75.93 | 72.47 | 72.55 |

Looking into the earnings spread of SBL, it can be observed that SBL has not been able to raise the spread but continuing to carry on with the same spread.

| 1999 | 2000 | 2001 | 2002 | |

| Earnings Spread | 0.03 | 0.03 | 0.03 | 0.03 |

From this, it can be inferred that SBL has been able to control its interest rates on loans or on deposits, despite of the strong competition in the banking industry.

11.2.3 Non-Interest Spread:

Further into the efficiency aspects, the non-interest margin, which measures the spread between the revenues from services provided (fee income), and its non-interest cost (salaries and wages, repair and maintenance, and loan loss expenses) can be focused.

| 1999 | 2000 | 2001 | 2002 | |

| Net Non Interest Margin (%) | 0.45 | 0.90 | 0.67 | 0.30 |

From this, we can see that SBL has been successful at controlling internal costs, whereby the difference between service fees and internal costs has been in a stable position. But the margin fell in 2002. They have been successful at providing services that generate fee income.

| 1999 | 2000 | 2001 | 2002 | |

| Net Bank Operating margin (%) | 1.93 | 1.98 | 2.73 | 2.31 |

Therefore, it can be assumed that it is due to their expense control strategies, that SBL has been able to steadily increase its net bank operating margin, even in its competitive environment. SBL’s expense control efficiency will be discussed later in the report.

11.2.4 Asset Utilization:

The shift of focus is now to another aspect of SBL’s performance, namely the Return on Assets.

| 1999 | 2000 | 2001 | 2002 | |

| ROA (%) | 1.01 | 1.48 | 1.87 | 1.34 |

The Return on Assets shows a clearer picture of SBL’s over the last 4 years. From here, it can be reconfirmed the trend that SBL’s earnings have been on the rise. From this, it can be inferred that SBL boasts managerial efficiency, increasing the rate at which assets are being converted into net earnings.

As the banking industry of Bangladesh has become saturated, and extremely competitive, SBL has turned to non-interest income sources to increase its asset utilization ratio.

| 1999 | 2000 | 2001 | 2002 | |

| Asset utilization ratio | 10.16 | 10.75 | 12.08 | 10.25 |

From this it can understand that the management of SBL has been able to construct sound portfolio management policies, with respect to the mix and yield of the bank’s assets.

To look into the composition of SBL’s assets, with reference to the earning assets, its earning base in asset can be focused.

| 1999 | 2000 | 2001 | 2002 | |

| Earnings base in asset (%) | 72.76 | 72.00 | 75.37 | 81.08 |

This shows that SBL’s earning assets has been increasing over the last four years which is a good sign and the reason for its good income.

SBL has been increasing its proportion of loans and investments over the last 4 years. It can clearly seen a rise in their earnings base, meaning that the bank has been growing, even in the event of extreme competition and uncontrollable environment. Their success at growth can be considered a powerful indicator of their strength in the market. This speaks well for their expansion prospects.

| 1999 | 2000 | 2001 | 2002 | |

| Total Loans and advances | 31 | 36 | 30 | 42 |

The loans and advances of SBL has a steady growth rate with 2002 having a good growth as new branches are opened in some of the important cities of Bangladesh and due to rise in business, with the base rising steadily over the years.

11.2.5 Liabilities:

Another aspect of growth for SBL is the growth in deposits, which reflects their acceptability and image in the market.

| 1999 | 2000 | 2001 | 2002 | |

| Total Deposits | 37.00 | 37.13 | 22.5 | 31.42 |