The projected benefit obligation (PBO), also known as the present value of defined benefit obligation (PVDBO), is an actuarial calculation that determines how much money a corporation will need now to fund future pension obligations. It’s the actuarial present value of all potential pension payments accrued to date by employees. It depends on expected future compensation increments. The PBO is utilized to decide what amount should be paid into a characterized advantage benefits intend to fulfill all annuity privileges that have been procured by representatives up to that date, adapted to expected future compensation increments. The PBO is calculated under the assumption that the company will continue to operate and that employees will remain with the company until retirement.

Projected benefit obligation (PBO) accepts that the arrangement won’t end soon and is changed in accordance with reflect expected remuneration in the years ahead. The PBO considers how long the representative will function and any expanded future commitments to the worker’s benefits. It is possible for the accountant to measure the PBO by working backwards using financial statement analysis. Actuaries are in charge of calculating whether or not pension funds are underfunded using the projected benefit obligation (PBO).

The PBO is assessed by statisticians by applying complex measurable displaying methods. Organizations can give representatives various advantages, including a compensation, when they resign from work. Companies must calculate and report their pension commitments, as well as the performance of their arrangements, at the end of each accounting period, according to the Financial Accounting Standards Board’s (FASB) Statement of Financial Accounting Standards No. 87. The present service cost, interest cost, past (prior) service cost, adjustments in actuarial assumptions, and benefits paid to workers all contribute to the adjustment in the PBO.

- Current service cost: the present value of employee benefits received during the fiscal year

- Interest cost: the increase in the obligation due to the passage of time

- Past (prior) service cost: retroactive benefits awarded to employees

- Changes in actuarial assumptions: changes in the discount rate, mortality, and employee turnover cause gains and losses

- Benefits paid: benefits paid to employees that lower the obligation

Together, these segments roll out up the improvement in the PBO. The PBO is contrasted and reasonable worth of plan resources for discover an annuity asset’s subsidized status. It is one of three different ways to figure costs or liabilities of conventional characterized advantage annuity designs that consider representative long periods of administration and pay to ascertain retirement benefits. Every year, the projected benefit obligation is unwound by acknowledging interest on the obligation, increasing both the PBO balance and the pension expense. The product of the opening PBO and the discount rate equals the interest cost.

The projected benefit obligation (PBO) formula looks as follows:

PBO = beginning of the year + service cost + interest cost + past service cost +/– actuarial gains/losses – benefits paid

Using the funded status formula,

funded status = fair value plan assets – PBO

PBO is adjusted to represent planned benefits in the years ahead, assuming that the pension scheme will not be terminated in the near future. As a consequence, it considers a variety of factors, including the ones mentioned below:

- The estimated remaining service life of employees

- Assumed salary rises

- A forecast of employee mortality rates

Projected benefit commitment (PBO) varies from the accumulated benefit obligation (ABO) in that the ABO depends on current assistance delivered and remuneration level while PBO estimates future pay level, expected help term, and so forth despite the fact that both measure commitment emerging from administrations delivered to date. Actuaries are in charge of determining whether or not pension funds are underfunded. Via a present value calculation, these trained practitioners, who specialize in the assessment and management of risk and uncertainty, assess the benefits needed.

Actuaries are in charge of calculating the liabilities and assets of a pension scheme. In general, they provide a breakdown of the following:

- Service costs: The rise in the present value of the defined benefit obligation as a result of existing workers receiving an additional year of service credit.

- Interest costs: When an employee’s service time rises, annual interest accrues on the PBO’s unpaid balance.

- Actuarial gains or losses: The disparity between an employer’s pension contributions and the sum anticipated. If the price paid is less than estimated, there is a profit. If the amount charged is greater than estimated, a loss occurs.

- Benefits paid: Obligations are reduced when benefits are paid out.

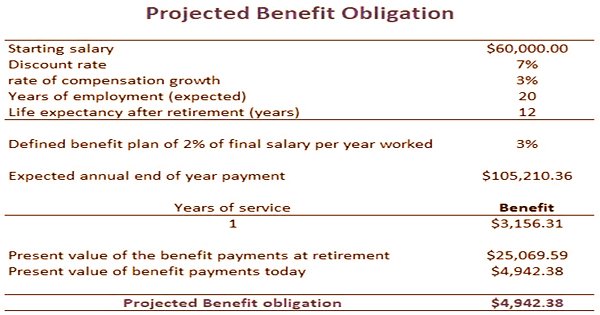

The calculations needed to calculate the shift in the PBO are shown in the table below. To perform the required calculation, a simple spreadsheet is clearly appropriate.

Building up whether an organization has an underfunded benefits plan can be accomplished by contrasting annuity plan resources the speculation reserve alluded to as the reasonable worth of plan resources, to the PBO. In the event that the reasonable worth of the arrangement resources is not exactly the advantage commitment, there is an annuity shortage. Despite the fact that a PBO is listed as a liability on the balance sheet, there is much debate about whether it meets the predefined requirements for such classification.

Information Sources: