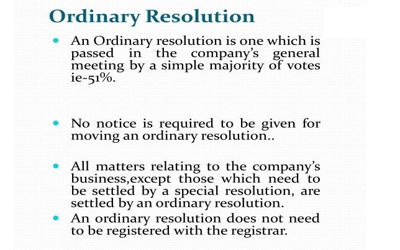

Ordinary Resolution

An ordinary resolution is a method by which members approve routine company decisions, traditionally in general meetings. Most company decisions are made by resolution and this will be an ordinary resolution unless the Companies Act 2006 or the company’s articles of association require it to be a different type of resolution. Section 81(1) of the Companies Act, 1994 provides that a resolution shall be an ordinary resolution when at a general meeting, of which the notice required under this Act has been duly given, the votes cast in favor of the resolution by members exceed the votes cast against the resolution.

An ordinary resolution is the most common method by which a corporate entity conducts its business or the board of directors seeks shareholder approval of its actions.

Here are some typical examples of decisions passed via an ordinary resolution:

- Approval of the annual accounts,

- Approval of a final or interim dividend,

- Re-appointment and appointment of a director,

- Increasing the authorized share capital,

- Reappointment of auditors,

- Removing a director.

In effect this covers the normal things a business would need to do, e.g. vote on giving people new shares, changing a director, making a small investment like office materials or a revamp. In business or commercial law in certain common law jurisdictions, an ordinary resolution is a resolution passed by the shareholders of a company by a simple or bare majority (for example more than 50% of the vote) either at a convened meeting of shareholders or by circulating a resolution for signature. This type of resolution can be passed with a show of hands at a meeting.

An ordinary resolution is the most common method by which a corporate entity conducts its business or the board of directors seeks shareholder approval of its actions. The ordinary resolution is commonly used for ordinary business transacted in the general meeting such as the declaration of dividends, the appointment of an auditor, adoption of annual accounts, the election of directors, issue of shares at a discount, the appointment of secretary, etc.

This ordinary resolution type needs a simple majority under the Companies Act 2014, that is to say, above 50% of the members are required to sign. Certain items of ‘special businesses’ also require ordinary resolutions under the Companies Act –

- Issue of shares at a discount

- Alteration of the share capital.

- Appointment of Branch Auditor.

- Increasing or reducing the number of directors within the limits fixed, by the Articles.

- Approval to the Board of Directors for exercising any of the powers.

- Appointment of the sole selling Agent.

- Remuneration is payable to the directors.

- Investment in any other body corporate.

- Voluntary winding up in specified circumstances.