Methods of Costing:

We know that costing is the system of calculating the cost. In the system of costing, we use different methods of costing. Any method of costing can be used in any business according to the need. Following are the main methods of costing.

1. Job Costing

In job costing, we calculate and collect the expenses for each work . This work is done on the basis of order. So, this is the part of specific order costing. A job card is made for each work or job. This method of costing is used in the factories which produce the machine tool and other engineering products, furniture projects, hardware and interior decoration. This method of costing is also called a piece of work costing or terminal costing.

Following are its features

a) Cost of Each unit of production is calculated separately.

b) A cost sheet is made for each job.

2. Batch Costing

Batch costing is just the extension of job costing. In batch costing, we do not calculate and collect the cost of each unit of production but we calculate the cost of each group or batch. Each group will be one unit of production under batch costing. For example, we are calculating the cost of 1000 bricks. It is one unit and under batch cost, we will calculate the material cost, labour cost and overhead cost of producing 1000 bricks. Except this example, we can take the example of ready-made garments batch, biscuit batch of 10 units in one packet etc.

3. Contract Costing

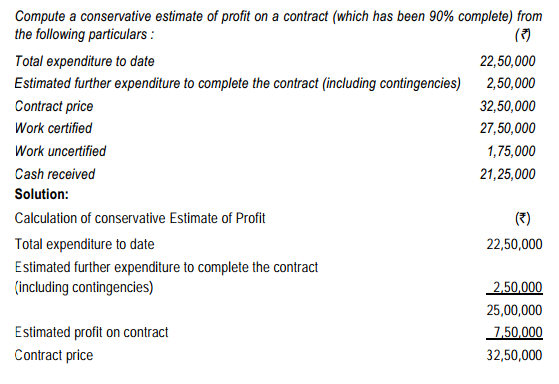

When the form of work will be big, at that time, we will use contract costing. We keep different contract account for each contract. Contract costing is used in building construction, machine construction contract. Actually like job costing, we will calculate the cost of material, cost of labour and cost of overhead of each contract. Suppose, we have to construct the 40 foot by 40 foot shopping mall. This one contract will be the our cost unit. Our contract price is just like our sale value. After deducting our all expenses, we will calculate our profit from contract. If any contract goes more than one year. We will calculate the notion profit on the basis of completed work of contract.

Process costing is used where production process will active all the time. Every production in one process will be the raw material of other process. Because produced product will become at the end of process, we will not only calculate the cost of each process but we will calculate the unit cost. For every process, we will open process account. We will show all the expenses relating to process in it. We will use the process costing in oil industry, chemical industry, paper industry etc.

5. Unit Costing

Unit costing is also called single or output costing. In cement industry, we can see the example of unit costing. Every bag of cement is important. We will calculate its production cost when we have to decide its sale price. When we produce the many units, we calculate unit cost by dividing total cost with total units of product.

6. Operating Costing

When any company provides the service instead of production of goods, this method of costing is used. For example, transport carriers, electricity distributing company, municipal committee, hospitals and hotels. Following is the cost unit, we use

Transport service = Passenger per kilometer, tonne per kilometer

Hospital = Patient per day

Cinema = Per ticket cost

7. Operation Costing

When a product is produced with different operations, we will use the operation costing. We calculate the conversion cost of converting raw material into output. We also deduct the cost of rejected material.

8. Multiple Costing

Multiple costing is that method in which we use many methods of costing together. For example, we have to make a product whose part are made from different factories. So, every part’s cost is calculated under job costing. After this, it is joined with different process. So, process costing will be applied. At the end, we will calculate the cost which we have calculated from multiple methods of costing.