Introduction:

Bangladesh is one of the developing countries in the world. The economy of the country has a lot left to be desired and there are lots of scopes for massive improvement. In an economy like this, banking sector can play a vital role to improve the overall social – economic condition of the country. The banks by playing the role of an intermediary can mobilize the excess fund of surplus sectors to provide necessary finance, to those sectors, which are needed to promote for the sound development of the country.The motives of banks are profit-earning. The word ‘Bank’ refers to the financial institution that deals with money transaction. Banks collect deposits at the lowest possible cost and provide loans and advances at highest cost. The spread between the two is the profit for the bank. Commercial banks are primary contributors to the national development of the country.

This report is an attempt to reflect the position of Prime bank Ltd in the banking industry of the country in respect of her activities in the arena of General Banking.

Rationale of the study:

Commercial banks in Bangladesh economy are to face an increasing competition for their business in coming days, like any other emerging market economies. Their business is no longer remaining easy as they earlier. The real change in the banking business has started to come with the government’s decision to allow the business in the private sector in the middle of the Eighty’s. This report is an effort to reflect a clear idea about the strategies, activities, and performance of Prime Bank Ltd. regarding general banking activities.

The General Banking department is the vital part for financial institution. It is linked with all other department. So it is very important to have an effective and sound management System in banking business. Bank is an important and the most appropriate institution for the necessity of the use of money and the protection of the money. As a BBA student having major in marketing, Financial institutions are the most appropriate field to gather the experience and among the financial institutions, Bank is the most prominent place.

Origin of the report:

This report is originated having three months long internship program originated after completing the BBA program from Department of Marketing under DhakaUniversity. During the internship a student has to undertake an arena of investigation of any organization for in depth study. This report is the outcome of the assigned internship, suggested by the human resource department of Prime Bank Limited, Head Office.

Objective of the report:

In this report, I tried to furnish all sorts of practical dealings that are conducted in case of handling various types of activities in general banking department, the theoretical aspects, that is what should be the procedures and requirements maintained from first to last, and actual practices as well as the ultimate gain for the bank in conducting financial activities are mainly discussed. So the purpose and objective of this report can be summarized as follows:

- Focus on the Brief description of general banking.

- To know deeply about general banking procedure.

- To examine bank’s performance in general banking activities

- To know how they minimize general banking risks

- To focus on some other activities of general banking

- To specify some findings on given topic

- To reveal some recommendation for better performance in general banking

Scope of the report:

Banking sector is a large and difficult area. A bank has different products, different services and different customers. Different departments of a bank perform different activities.

However, the scope of present study was limited in a specific area of an organization Prime Bank Limited, Utara Branch. So this study says only about the activities of Prime Bank Limited, Uttara Branch. This study covers only various section of Prime Bank Limited, Uttara Branch only.

Methodology:

The methodology of this report is very different from conventional reports. I have emphasized on the practical observation though this report has to need some primary and secondary data. Nevertheless, eventually almost the entire report consists of my practical observation.

Sources of data collection:

While preparing the report, I have taken information from the following sources:

Primary Sources:

- Observation of banking activities.

- Overflowing Conversation with the in-charge of general banking department of Prime Bank Limited, Uttara Branch.

- Working with my own experience while internship program.

Secondary Sources:

- Daily diary (containing my activities of practical orientation in Prime Bank Ltd) maintained by me,

- Various publications on Bank,

- Website of Bangladesh Bank,

- Website of Prime Bank Limited,

- Annual Report of the bank,

- Personal investigation with bankers,

- Different circulars issued by Head Office and Bangladesh Bank

Potential problems of statement:

Some of the limitations faced in preparing this report are:

- It was very difficult to collect the information from various personnel for their job constraint.

- There were some difficulties in understanding some activities due to not being relevant to the theoretical knowledge.

- Due to confidentiality the Bank’s policy restricts disclosing some data.

- Most of the cases I have to use previous year’s data for the evaluation and analysis, since data about the performance of the bank of the year 2007 have not yet been disclosed by the bank. Because the annual report and the financial statement of the bank are published at the month of August each year.

- The study of such a short course of time is not free from limitation. So time limitation is the main point of limitation.

- The data relevant for the analysis report writing sometimes could not be collected due to excessive year-ending workload at the branch.

- During the month of January in the branch, there was excessive year-ending workload, which sometimes acts as a barrier on the way of my effort.

- It is too much difficult to comment and suggest based on only the annual report and information collected from written documents.

PRIME BANK LIMITED: AN OVERVIEW

Introduction of the Organization:

Bank is a financial institution. The economy is mostly dependent on the bank since the bank facilitates the economic and financial transactions. Prime bank limited is a fast growing private sector bank and the bank is already at the top slot in terms of quality services to the customers and value addition for the shareholders. The bank made satisfactory progress in all areas of business operation in 2007.

Prime Bank Ltd. is one of the few banks permitted by the Bangladesh in the early 90’s. These banks are known as the second-generation banks and fortunate to remain immune from the bad loan culture. Prime Bank Limited was designed to provide commercial and investment banking services to all types of customer ranging from small entrepreneur to big business firms. Besides investment in trade and commerce, the bank participates in the socioeconomic development through the participation in priority sectors like agriculture, industry, housing and self-employment. Prime Bank Limited wants to establish, maintain, and conduct all types of banking, investments and businesses in Bangladesh and abroad with superior service quality and performance.

The bank has consistently turned over good returns on Assets and Capital. During the year 2006, the gross revenue of the bank grew by 34% to reach Tk.3232 million while operating profit increased by 40% to arrive at Tk. 2131 million. At present the bank has 61 branches all over the Bangladesh and a booth located at Dhaka Club, Dhaka. Out of the above 41 branches, 05 (Five) branches are designated as Islamic Branch complying with the rules of Islamic Shariah, the modus operandi of which is substantially different from other branches run on commercial conventional basis.

Hierarchy of Prime Bank Limited

Organizational Hierarchy in Prime Bank Limited

Chairman |

↑ |

Managing Director (MD) |

↑ |

Additional Managing Director (AMD) |

↑ |

Deputy Managing Director (DMD) |

↑ |

Senior Executive Vice President (SEVP) |

↑ |

Executive Vice President (EVP) |

↑ |

Senior Vice President (SVP) |

↑ |

Vice President (VP) |

↑ |

Senior Assistant Vice President (SAVP) |

↑ |

Assistant Vice President (AVP) |

↑ |

First Assistant Vice President (FAVP) |

↑ |

Senior Executive Officer |

↑ |

Executive Officer (EO) |

↑ |

Principal Officer |

↑ |

Senior Officer |

↑ |

Management Trainee |

↑ |

Officer |

↑ |

Junior Officer |

↑ |

Assistant Officer |

↑ |

Trainee Assistant |

Brief Description of Business Activities, Product & services and Financial Position of Prime Bank Limited

|

The Principal activities of the bank were banking and related businesses. The banking businesses included deposits taking, extending credit to corporate organization, retail and small & medium enterprises, trade financing, project financing, international credit card etc. Prime Bank Limited provides a full range of products and services to its customers, some of which are mentioned below with a brief overview of the major business activities.

As a part of risk diversification strategy PBL expended the lending activities in this sector during 2006. The growth rate of PBL’s consumer financing was 38% during this year. The loan schemes offered by the bank include Home Loan, Loan against Salary, Marriage Loan, Car Loan, Hospitalization Loan, Education Loan, Doctors Loan, Travel Loan etc.

SME Lending:

Job creation is essential and it must come from Small and Medium Enterprise that will ultimately dominate the private sector. During 2006 bank’s Strategy was focused on customer convenience. The Bank provided working capital loans to suppliers or dealers of large corporations or clusters of small exporters of non-traditional items. Outstanding loan of SME is Tk.437 million. The growth rate of PBL’s SME Lending was 41% during this year.

PBL’s strategy is to provide comprehensive service to the clients of this segment who are large and medium size corporate customers with expertise in trade finance and related services. Besides trade finance bank are providing working capital finance, project finance and arranging syndication for our corporate clients. Syndication and structured Finance Unit of the Bank strengthened its footstep in the consortium financial market and arranged a number of syndication deals for its corporate clients

Islamic Banking:

For the development of Islamic Banking Business, 2006 was also a commendable year. It has been observed that compliance of Shariah has improved in 2006 as compared to the preceding years. According to their advice Islamic Banking operation of the bank has been separated from the operation of Conventional Banking and shown separately in the bank’s financial statement. It is found that the investment and deposits grew by 38% and 89% respectively in the year 2006. The operating profit of Islamic Banking Branches grew by 45% during the Year.

Credit Card:

In the year of 2005, Prime Bank Ltd has launched VISA. Before that PBL started its credit card operation in 1999 by introducing Master Card. Now PBL has become the first local Bank of the country to achieve principal membership of both the worldwide-accepted plastic money network i.e. Master Card and VISA. PBL has redesigned the credit card facility by providing the incentive of “Free Life Insurance Coverage” for their valued cardholders to mitigate the financial risk.

Custodial Service:

PBL equator fulfills its strategic commitment to provide custody and clearing services. Equator’s focuses are on the following:

- Commitment to quality

- Dedication to customer needs

- Sustained investment in people and systems

International Trade Management:

This division is operational throughout the group and PBL’s core strength is trade finance and services. With an experience, Prime Bank has developed knowledge of trade finance, which is world class. Principle services to importers include imports letter of credit, import bills for collection and back-to-back letters of credit facilities. Services provide to exporters include export letters of credit, direct export bills, bonds, and guarantees.

Cash Management:

Prime Bank recognizes the importance of cash management to corporate and financial institutional customers, and offers a comprehensive range of services and liquidity management.

Institutional Banking:

Prime Bank Limited provides a wide range of services to institutional clients, commercial, merchant and central banks; brokers and dealers; insurance companies; funds and managers, and others. It provides relationship managers who are close to their customers and speak local language. This wide network of institutional banking facilities includes transaction, introduction, problem solving and renders advice and guidelines on local trading condition.

Treasury:

Treasury operations had been consideration as an important avenue for income generation purpose within Head Office. In fact, in the past, income from treasury operation was quite sizable and significant to the total income generated by the bank. The treasury division publishes daily and weekly currency newsletters, which provide analyses of currency trends and related issues. Seminars and workshops are conducted for customers from time to time on foreign exchange related topics. Prime Bank is one of the first local banks in Bangladesh to integrate treasury dealings of local money market and foreign currency under one Treasury umbrella. The bank has handled significant volumes of treasury over the last several years. Prime Bank’s Dealing Room is connected with automated Reuters Terminal facility thus enabling the bank to provide forward/future facilities to its corporate clients at a very competitive rate.

Foreign Exchange Business:

Over the years, foreign trade operations of the bank played a pivotal role in the overall business development of the bank. The bank has established relationship with as many as 110 new foreign correspondents abroad thereby raising the total number of correspondents to 350. The total import & export business handled by the bank during the year 2006 was TK 52,639 million and Tk 41,801 million. The growth rate was 46%. The bank has also entered into remittance arrangements with several banks and exchange houses and expects to handle increased volume of remittance business over the near future.

Merchant Banking:

The Bank’s operation in this sector was limited to Underwriting, Portfolio Management and Banker to the Issue functions. The compulsory requirement for opening BO account for share trading has increased the demand for opening BO account.

Online Branch Banking:

The bank has set up a Wide Area Network (WAN) across the country to provide online branch banking facility to its valued clients. Under this scheme, clients of any branch shall be able to do banking transaction at other branches of the bank.

Under this system a client will be able to do following type of transactions:

- Cash withdrawal from his/her account at any branch of the bank.

- Cash deposit in his/her account at any branch of the bank irrespective of the location.

- Cash deposit in other’s account at any branch of the bank irrespective of the location.

- Transfer of money from his/her account with any branch of the bank.

SWIFT:

Prime Bank Limited is one of the first few Bangladeshi banks, which have become member of SWIFT (Society for Worldwide Inter-bank Financial Telecommunication) in 1999. SWIFT is a member-owned co-operative, which provides a fast and accurate communication network for financial transactions such as Letters of Credit, Fund Transfer etc. By becoming a member of SWIFT, the bank has opened up possibilities for uninterrupted connectivity with over 5,700 user institutions in 150 countries around the world.

Information Technology in Banking Operation:

Prime Bank Limited adopted automation in banking operation from the first day of its operation. The main objective of this automation is to provide efficient and prompt services to the bank’s clients. At present, all the branches of the bank are computerized. At branch level, the bank is using server-based multi-user software under UNIX operating system to provide best security of automation.

Profitability and Shareholder Satisfaction:

The bank had been one of the most profitable in the banking sector. The bank’s return on assets (ROA) was 2.05% in the year 2006. Even though the capital market of the country has been suffering over the last few years, the good performance of Prime Bank made sure that the banks share price remained in a respectable position.

|

Prime Bank Limited offers various kinds of deposit products and loan schemes. The bank also has highly qualified professional staff members who have the capability to manage and meet all the requirements of the bank. Every account is assigned to an account manager who personally takes care of it and is available for discussion and inquiries, whether one writes, telephones or calls.

Loan Schemes:

General Loan Scheme

Consumer Credit Scheme

Lease Finance

HouseBuilding Loan & Apartment Loan Scheme

Advance against Shares

Custodial Services for investors (both individual & institutional) investing in through Stock exchange

One stop services for payment of utility bills.

Credit card

|

Investment:The Bank’s investment increased during the year by Tk 3,905 million and stood at Tk. 7,844 million as at 31 December 2006.

Loan & Advances and Deposits:

Loans and Advances of the Bank grew strongly by 41% to 45010 million in 2006. Bills purchased and discounted increased by 27% indicating strong growth in export performance.

The Bank’s deposits and the Customer deposits of the Bank grew by 52% & 52% respectively in 2006. However, fixed deposits remained the main component of deposits contributing about 55% of total deposits.

Liabilities:Total liabilities of the Bank are increased by Tk. 18,341 million during 2006. Resulting mainly from increase in deposits from customers.

Shareholders Fund:

The Shareholder’s Fund is increased by 37% during the year. Paid-up capital increased by Tk.350 million and stood at Tk.1,750 million during 2006.

Non-interest & Investment Income:

Non-interest & Investment Income are increased by 28% & 62% respectively in year 2006.

Net Profit before & After Tax :

Net Profit before Tax stood at Tk.1741 million and Net Profit after Tax had become Tk.1,052 million. Thus the growth rate of the Net Profit before Tax was 45% then that of previous year. In case of Net profit after Tax it was negative growth of 85% during 2006.

Summary of Financial Performance:

Despite the challenges, Prime Bank closed on a high note and made an impressive progress in many lines of business during 2006. The operating profit before provisions registered a growth of 40% during the year. Strong profit performance was attributable to its sustained high level of deposits and loan growth, maintaining the good asset quality and enhancing productivity and proactive management of balance sheet. Revenue income increased by 34% while expenses increased by 24%. The growth asset was 47% and non-performing loan remained below 1%. Contingent business grew by 21% during 2006 contributing to the increase in fee based income. Profit before tax showed a growth of 45%. Profit after tax was 1052 million registering growth of 85%. Return on asset stood at 2.03% compared to 1.54% of previous year. Despite the rise in capital base by Tk. 350 million, EPS was an impressive Tk. 60.11 while return on average equity stood at 31.55%.

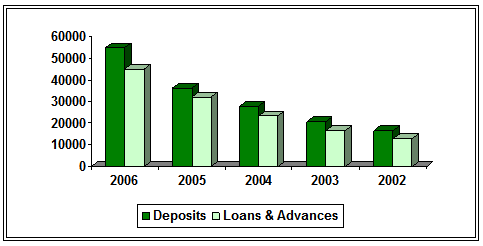

The financial position for the last five years of Prime Bank Limited at a Glance

(Taka in million):

Particulars | 2002 | 2003 | 2004 |

2005 |

2006 |

| Total Deposits | 16482 | 20483 | 28069 | 36022 | 54727 |

| Loans and Advances | 12687 | 16492 | 23220 | 31916 | 45010 |

| Investment | 1996 | 2750 | 3084 | 3940 | 7844 |

| Foreign Exchange Business | 31754 | 41931 | 56249 | 69185 | 94440 |

| Operating Expenditure | 448 | 591 | 824 | 886 | 1101 |

| Operating Profit | 748 | 1001 | 1146 | 1520 | 2131 |

| Profit after tax | 418 | 375 | 612 | 568 | 1052 |

| Total Assets | 19359 | 24249 | 32362 | 41506 | 60899 |

| Market value per share | 307.51 | 374.25 | 879.5 | 618.50 | 528.75 |

| No of Branches | 27 | 30 | 36 | 41 | 50 |

| No of Employees | 730 | 777 | 894 | 1024 | 1172 |

| No of Shareholders | 1727 | 1993 | 2620 | 4467 | 5262 |

| No of Foreign Correspondences | 422 | 441 | 501 | 517 | 528 |

uttara BRANCH, PRIME BANK LIMITED

Introduction to uttara branch:

Uttara Branch is the 22nd branch of Prime Bank Ltd. The name of the present branch Manager is MR. M. SHAHIN ALAM, VP. The overall banking operation of Uttara Branch can be divided into three broad categories. These categories or divisions are:

1. General Banking

2. Foreign Exchange Division

3. Investment or Advance Division

Account opening, Local Remittance, Clearing, Deposit and Accounts are the subdivisions that belong to the General Banking Division, where as Import, Export and Foreign Remittance are the subdivision under Foreign Exchange Division.

At present about 23 personnel work at Uttara Branch of Prime Bank Limited.

STRUCTURE of UTTARA Branch:

Deposit:

Every body knows that the deposit is the lifeblood of a Bank. From the very beginning Prime Bank Uttara Branch is aware about deposit build-up. The branch is trying to do better day by day. The deposit on February 19, 2008 was 171, 98, 02,716.49 corers.

Table 10: Deposit under different Schemes

| Nature of Deposits Under Different Schemes As on February 19, 2008 | |

| Schemes | Amount (BDT) |

| Contributory Term Deposit | 5,50,58,480.72 |

| Special Term Deposit | 11,86,37,320.18 |

| Monthly Benefit Deposit | 7,28,00,000.00 |

| Education Savings Scheme | 8,44,007.88 |

| Lakhopati Deposit Scheme | 4,93,49,614.31 |

| HouseBuilding Deposit Scheme | 1,61,730.71 |

Number of Accounts:

Number of accounts in Uttara Branch as on February 19, 2008 is as follows:

Table 11: Total Number of Accounts

| Types of Account | No. of Accounts |

| Current Account (CD) | 1073 |

| Savings Account (SB) | 3315 |

| Short Term Deposit (STD ) | 38 |

| FC Account | 47 |

| Loan Account | 685 |

| DPS | 2 |

| Savings Account | 3963 |

Loans and Advances:

The age of Uttara Branch is more than 7 years. In these period the Branch have already invested thousand millions of money. The officials of the Branch are trying their best to follow the Head Office instruction. But the Branch believes in good investment not volume of investment. The branch continues to explore and diversify the area of financing in addition to traditional financing of domestic and international trade. It financed a number of industrial projects and participated in industrial loans.

Table 12: Loan/Advances in Uttara Branch:

| Nature of Loan/Advances in Uttara Branch |

As on Feb19, 2008Nature of AdvancesAmount (BDT)Loan (General)320626392.66T.R.Loan209784707.21HouseBuilding Loan27567785.42Lease Finance958534.94Cash Credit199925150.87Cash Credit Scheme50264528.67Staff Loan6137401.53Overdraft87110946.30

GENERAL BANKING SECTION:

The general banking department does the most important and basic works of the bank. All other departments are linked with this department. It also plays a vital role in deposit mobilization of the branch. Actually general banking is called the mother of banking. However, PBL provides different types of accounts, locker facilities and special types of savings scheme under general banking.

ACCOUNT OPENING SECTION:

The relationship between banker and customer begins with the opening of an account by the customer. Selection of customer for opening an account is very crucial for a bank. In fact, fraud and forgery of all kinds start by opening account. So, the Prime Bank Limited takes highest caution in this regard. However, PBL opens the following accounts for its customers:

Current account (CD A/C)

Savings account (SB A/C)

Shot term deposit (STD A/C)

Fixed deposit account (FDR A/C)

A brief on this Accounts are given below:

CURRENT ACCOUNT:

Current account is purely a demand deposit account. Basically it can be open for the purpose of business. There is no restriction on withdrawing money from this account. It is suitable when funds are to be collected and money is to be paid away at frequent interval. It is the most suitable for private individuals, traders, merchants, importers and exporters, mills and factory owners, limited companies etc. For opening a current account minimum deposit tk 5,000/- is required along with introductory reference. No interest is given on the current account deposit money. The following points are important:

- A current account is a running and active account. There is no restriction on the number and the amount of withdrawals from a current account.

- The banker is under an obligation to repay these deposits on demand, so they are called demand liabilities of a banker.

- The primary objective of current account is to save customers such as businessmen, join stock companies, public authorities, etc. from risk of handling a lot of cash money.

- The bank does not pay interest on current deposits while on the other hand, some bank charge for incidental charges on such accounts.

- The bank provides overdraft facilities also in certain cases.

- The account holder can withdraw the deposited money from his account with the cheque, which will be issued to the against his account number.

- The cancellation fee for current account is tk. 100.

- An account holder can withdraw and deposit money in his account in several times in a week.

There are several types of current account which are stated below:

- Current Deposit Account for Individual/Joint Account.

- Current Deposit Account for Private firm (Proprietorship concern).

- Current Deposit Account for Private firm (Partnership concern).

- Current Deposit Account for Limited Company.

- Current Deposit Account for the account of Societies, Clubs, etc.

- Current Deposit Account for Private firm (Proprietorship concern)

Documents required:

1) A/C opening form.

2) Introducer of CD A/C holder in this bank.

3) Signature form/card.

4) If it is used for the purpose for business, it must require trade license.

5) Photocopy of character certificate or photocopy of passport.

6) Two-copy passport size photo & Declaration certificate.

- CD for partnership A/C

Documents required:

- Partnership deed.

- List of partners with their address.

- Copy of trade license.

- Photographs of signatories.

- Separate nomination form duly signed by the nominee & the account holders and photograph of the nominee duly signed by the account holders.

- CD for Private & Public Limited Company A/C

- Trade license.

- Photograph of the director.

- Certified copy of the memorandum and articles of association.

- Certificate of incorporation.

- List of directors as per return of joint stock company with signature.

- Resolution for opening account with the bank.

- Signature of the introducer.

- TIN certificate.

- Certificate of commencement.

- CD for Association/Club/Charity A/C

Documents required:

- Two copies of photograph of the person(s) who will operate the account.

- Certified copy of memorandum and articles of association.

- Certified copy of bye laws and regulations.

- Certified copy of resolution for opening and operation of the account.

- Photograph of signatories.

- Up-to-date list of office bearers/ government body/managing committee.

SAVINGS ACCOUNT:

Savings account is allowed for all people. Anyone can run this account for his personal or business purposes. To open this account depositor have to give at least Tk.1000 at the time of opening. The main objective of this account is to promote lower income people to save their portion of their income for their future use. Hence there is restriction on withdrawals in a month. Heavy withdrawals are permitted only against prior notice.

- Any adult person can open this account with his own name or with some one else that joint account.

- Any minor can open this account with the guidance of the guardian.

- Any company/ club can open this account.

Any illiterate person can open this account with his thumbprint. So he can withdraw money from his account in the presence of himself.

However the other noticeable features of the saving account are as follows:

- Frequent withdrawal is not encouraged.

- Normally withdrawal not allowed more than ¼ of the balance.

- One may allow withdrawn his amount maximum twice a week.

- Seven days notice is required for withdrawal of large amount.

- Account holder is not allowed to withdraw the amount more than 25000 at a time.

- The rate of interest is 6% against savings account.

- The depositor can deposit money in his account in several times. But if he wants to deposit pay order, cheque draft etc., he has to cross that instrument as an account payee.

- If the account holder wants to close his account he has to pay a cancellation charge that is tk.100/- for the saving account.

- The number of leaves in the saving account’s cheque book is 10.

FIXED DEPOSIT RECEIPT:

Actually Fixed Deposit Receipt (FDR) is not an account. It merely deposits receipt. It is popularly known as “Time Deposit”. Because these deposits are not repayable on demand but they are withdraw able subject to a period of notice. The prospective fixed deposit holder is expected to fill up an application form prescribed for the purpose stating the amount and the period of deposit. The application itself contains the rules and regulations of the deposits including the space for specimen signature. The general features of FDR are as follows:

- Payment made on expiry of agreed period.

- FDR allowed for one, three, six and twelve month period.

- Payment demanded before expiry of agreed date then penalty may be charged.

- Introducer is not needed in this case.

- Two copies of account holder and nominees photograph are needed.

- Loan may be sanctioned against FDR.

INTEREST RATE OF FIXED DEPOSIT RECEIPT:

SL. No.

| Period

| Amount

| Rate of Interest (%)

|

01 | One month | 7.5% | |

02 | Three months | Below Tk. 5 crore | 11.00% |

Tk. 5 crore & above | 11.50% | ||

03 | Six months | Below Tk. 5 crore | 11.00% |

Tk. 5 crore & above | 11.50% | ||

04 | One year & above | Below Tk. 5 crore | 11.50% |

Tk. 5 crore & above | 11.75% |

SHORT TERM DEPOSIT:

Short Term Deposit Account opening procedure is similar to that of the savings account. The rate of interest on this type of account is:

| Serial No | Particulars | Rate of interest |

| 1 | Below Tk.1 crore | 5.00% |

| 2 | TK.1 crore & over Tk. 1 crore | 6.00% |

DOCUMENTS NECESSARY TO OPEN AN ACCOUNT:

Account opening form-to be filled in and signed by each account holder.

2 copies of passport size photographs of the account holder attested by the introducer.

1 copy passport size photograph of the nominee attested by the account holder.

Copy of passport / voter identity card/ chairman’s certificate.

Fill up declaration form (Under Money Laundering Prevention Act-2)

To fill up Know Your Customer (KYC) Form.

The procedure to open an Account is given as following:

Note: This is a sample of process to open an Account. But varies the required documents to open that particular account. The requirements to different accounts have mentioned earlier.

DOCUMENTS THAT ARE GIVEN TO THE ACCOUNT HOLDER:

After all the account opening formalities have been completed Bank opens an account in the name of the applicant. Bank provides customer:

- A Deposit slip

- A Cheque book

- A Receipt book

ISSUANCE CHEQUE BOOK TO THE CUSTOMER:

After opening an account the account holder need a cheque book to withdraw money from the bank whenever he or she needed. However, cheque book issuance procedures of PBL are as follows:

- Issuance of cheque book (for new account): to get a new cheque book the account holder need to fill up the specific application form.

- 2. Issuance of cheque book (for existing account):

In case of existing account the cheque requisition are in the cheque book where a white pages lies containing the name and account number of the account holder. Whenever the leaves of the cheque finished the account holder submit it to cheque issue officer requesting to issue a new cheque book with his/her signature. However, for both the cases the following procedures are needed to follow to issue a new cheque book.

- After getting the requisition the respective officer required to verify the account holder’s signature and identification. It is very important task. No cheque can be issued without verification.

- Now the officer needs to attach round and branch seal on cheque.

- After that it needs to be attached account number seal on the cheque.

- In this stage two officers’ initial is needed on the cheque.

- Now it needs to entry on the cheque issuie register and signature on the register of the client.

- Finally verifying all the necessary seal, initial the officer issue the cheque and submit the requisition form to the computer section.

- Thus a new cheque book can be issued for both the new or existing client.

Total procedures have to done very carefully because most of the fraud found in this case.

OTHER TERM DEPOSIT ACCOUNTS:

- Monthly Benefit Deposit Scheme (MBDS A/C)

- Contributory Savings Scheme (CSS)

- Double Benefit Deposit Scheme (DBDS).

- Lakhpoti Deposit Scheme (LDS) and

- House Building Deposit Scheme (HBDS)

MONTHLY BENEFIT DEPOSIT SCHEME (MBDS):

MBDS are another main part of Prime Bank Ltd. This account is created for the benefit of the people who intend to meet the monthly budget of their families from the income out of their deposit. This scheme is suitable for trusts, club and foundations or other associations, which award monthly scholarships to the students etc. We know the bank is the most secured place to deposit money. So, people can come and run this account quite easily for big savings with little installment per month.

The terms and conditions for operating MBDS account:

1. To open a MBDS account the client has to use its form and must have an introducer and also the name of the nominee. If the client give attested photograph, it would be helpful at the time of closing the account.

2. The deposit of Tk. 25,000 and multiples thereof, but maximum Tk. 25, 00,000 shall be acceptable under the scheme.

3. The deposit shall be for a period of 5 years. The principal amount is refundable on maturity.

4. Profit shall be paid on monthly basis @ Tk. 1,000/- & net of taxes @ Tk. 900/- per Tk.1, 00,000.

5. Payment of monthly profit starts from the subsequent month after a clear minimum gap of 30 days from date of deposit.

6. If the mailing addresses of the depositors changes, he/she immediately have to inform it to the bank.

7. Income tax, Tk. 10% will be deducted on the income received from the deposit.

8. The client can transfer his/her account to another branch of the same bank by only for special cause.

9. The receipt is not transferable.

10. Advance against lien on such Receipt can be allowed up to 80% of the deposit bearing normal rate of interest prevalent at the time on Overdraft/Loan.

11. In case the instrument is lost the procedure for issuance of a duplicate will be the same as applicable in case of loss of FDR.

12. During the period of such Overdraft/Loan, the monthly benefit shall be credited to the concerned Overdraft/Loan.

13. Normally, the deposit is not encashable before 5 years. But if any depositor can withdraw his deposit before maturity due to certain unavoidable reasons, he/ she will be allowed to do so in the following manner:

- No benefit including interest shall be allowed for pre-mature encashment within one year.

- If the accounts/deposits are closed/ enchased after 1 year of its opening, benefit shall be allowed on the deposit at existing normal savings deposit rate.

- If the amount of monthly profit already paid exceeds the amount payable at normal savings rate.

14. The bank has the right to change the rules or update the whole thing of MBDS

CONTRIBUTORY SAVINGS SCHEME:

le & upper class people who want to save money for future use. In this project depositor have to deposit money for five years any installment size at the time of opening of the A/C. Any person can open the scheme by following proper guidance. At the time of opening account under CSS customer must refer his/her SB A/C. No. for his /her pension amount or may open SB A/C at the time of maturity for getting monthly pension amount. Lump sum amount shall be paid after maturity or monthly pension shall be paid for the next 5 years according to the size of deposit. For example, a brief chart of lump sum amount and monthly pension installment payable are shown in the following chart:

Size of monthly deposit | After 5 years terminal value | Pension for next 5 years |

2,000 | 1,60,000 | 3,457 |

3,000 | 2,40,000 | 5,186 |

4,000 | 3,20,000 | 6,915 |

5,000 | 4,01,000 | 8,644 |

6,000 | 4,81,000 | 10,373 |

Some other features are mentioned below:

- The depositor is not allowed change the size of installment afterwards.

- A person can open more than one account for different size of installments in any branch of the bank.

- The specified amount on maturity at any slab shall be paid after one month from the date of deposit of the final installment.

- The installment shall be payable by 8th day (in case of holiday the next working day) of every month.

- Normally the depositor can not withdraw money before maturity except certain unavoidable reasons.

- When a depositor fails to deposit any installment, he/she will have to pay a fine @ 5% of the overdue amount payable at the time of depositing the next installment or maximum Tk. 500/-.

- The bank at its discretion may allow inter branch transfer of the A/C holder.

DOUBLE BENEFIT SCHEME:

This offer is very attractive for the person who has additional money in hand. By this account people can deposit their money for a period of six years and after the maturity he/she will get double money back. By this account people can use their ideal money by which he cannot earn or cannot able or don’t feel secure to invest on business. Under this project his/her money can be fully secured with some benefit after few years.

The benefits categories are mentioned in the following table:

Double Benefit Scheme:

Period

| Deposit Amount (Taka One Time)

| Interest with deposit

| Payment Amount with Interest on Maturity

|

6 years | TK. 10,000 | Double | TK. 20,000 |

6 years | TK. 25,000 | Double | TK. 50,000 |

6 years | TK. 50,000 | Double | TK. 100,000 |

6 years | TK. 100,000 | Double | TK. 200,000 |

6 Years | TK. 200,000 | Double | TK. 400,000 |

There are some features which are mentioned below:

- Photograph of the nominee attested by the depositor.

- The scheme carries free life insurance coverage facility.

- Income tax may be deducted as imposed by the government on the interest amount at the time of maturity.

- Normally no withdrawal will be allowed before maturity. But if any depositor intends to withdraw his deposit before maturity, the following rules will apply:

a) No benefit including interest/profit shall be allowed for pre-mature encashment within 1 year.

b) If the accounts/deposits are closed/encashed after 1 year of its opening, benefit shall be allowed on the deposit at normal savings deposit rate.

LAKHOPA00TI DEPOSIT SCHEME:

The scheme is suitable for the person who intends to deposit money for next use. Normally, by this account people can deposit their money for different period, after the maturity he/she will get Tk.1, 00,000/- back. The benefits categories are mentioned in the following table:

period | Monthly deposit | Payment on the maturity |

15 | 250 | 1,00,000 |

10 | 500 | 1,00,000 |

5 | 1,285 | 1,00,000 |

3 | 2,400 | 1,00,000 |

HOUSE BUILDING DEPOSIT SCHEME:

This scheme is another attractive scheme for interested people who are willing to invest money for different periods for future use. It is normally suitable for the retired person. Besides minor can open the scheme complying all formalities related with opening of minor’s account. For house building loan facilities it is the most perfect scheme because the depositor will be allowed to take loan from the bank against it. According to the installment and duration of the deposit, equity building amount shall be Tk.10 lac/Tk.20 lac and a chart in this regard is mentioned below:

Monthly deposit (in Taka) | Investment period (in Year) | Age limit (for HBL facilities only) | Payment after the investment period (in Taka) |

4,570 | 10 | 35 years | 10,00,000 |

7,890 | 7 | 38 years | 10,00,000 |

12,465 | 5 | 40 years | 10,00,000 |

9,135 | 10 | 35 years | 20,00,000 |

15.770 | 5 | 38 years | 20,00,000 |

24,925 | 7 | 40 years | 20,00,000 |

ACCOUNT CLOSING SECTION:

It is a general right for every account holder to close his or her account at any time s/he find inconvenient to continue. But also has some formalities. The person needs to apply to the manager of the specific branch mentioning the reason for the account closing also the date when he would like to close his/her account with 100/- account closing charge.

REMITTANCE SECTION:

This department is another important part of the Bank. This department also issues and receives PO, PS, DD, TT, etc. By this department clients can send their money to different places of the country or in the world. This department is helps the bank to domestic and international transaction for the clients.

The items of this dept. are following:

PAY ORDER (PO):

Process of issuing Pay order

Customer is supplied a Pay Order form with a commission voucher and vat on banking service voucher. After filling the form the customer pays the money in cash or by cheque. The concerned officer then issues PO on its specific block. The officer then writes down the number the PO block on the PO form then two authorized officers sign the block. At the end customer is provided with the two parts of the block after signing on the block of the bank’s part.

Accounting procedure of pay order:

a) On issuing of PO

1. Cash A/C of party A/C ————Dr.

PBL General A/C ————Cr.

Income A/C commission on PO ———Cr.

2. PBL General A/C ————— Dr.

Bills Payable A/C- P.O ———-Cr.

b) On encashment of P.O.

Bills Payable A/C —————Dr.

Party A/C ————————Cr.

Payment of Pay Order (PO):

AS the PO issued by the bank is crossed one it is not paid over the counter. On the contrary the amount is transferred to the payees account. To transfer the amount the payee must duly stamp the PO.

Commission and Vat on PO.

Amount | Commission | Vat |

| 10,000 | 15 | 3 |

| 10,001-1,00,000 | 25 | 4 |

| 1,00,001-5,00,000 | 50 | 8 |

| 5,00,001-10,00,000 | 75 | 12 |

| 10,00,001-above | 100 | 15 |

DEMAND DRAFT (DD):

A demand draft is a written order of one branch upon another branch of the same bank, to pay a certain some of money to or to the order of a specified person. Drafts are not issued payable to bearer. In practice, drafts are not to be drawn between branches within the same city.

Process of DD Issue:

Customer is supplied a DD form with a commission voucher and vat on banking service voucher.

Customer fill up the form which includes the name of payee, amount of money to be sent, exchange, name of the drawer branch, signature and address of the drawer.

The customer may pay in cash or by transferring the amount from his / her account (if any).

After the money is paid and the form is scaled and signed accordingly it is given to the DD issuing desk.

Upon the receiving the form concerned officer issues a DD on a particular block. The DD block has two parts, one for bank Bank’s part contains issuing date, drawer’s name, payee’s name, sum of the money and name of his drawee branch.

Customer’s part contains issuing date, name of the payee, sum of the money and name of the drawee branch.

After furnishing all the required information entry is given in the DD Issue register and register and at the same time bank issue a DD confirmation slip addressing the drawee branch. This confirmation slip is entered into the DD advice issue register and a number is put on the confirmation slip from the same register. Later on the bank mails this slip to the drawee branch. At least two Grade -1 officer sign the DD block and amount is sealed on the DD with a special red seal to protect if from material alteration. The number of DD is put on the DD form. Next the customer is supplied with his/her part.

PAYMENT OF DD:

When a DD is brought for payment, the branch check out the following matters: Whether the DD is drawn on them. Whether it is crossed or not . Whether it is properly signed by the authorized officer of the issuing branch.

The branch then checks out whether the confirmation slip has arrived or not.

If the confirmation has not arrived, the DD is given entry in the Ex-Advice register.

Concerned officer writes down the date on which the DD was paid on the confirmation slip and sign on it.

When the confirmation slip arrived before the DD, it is entered into the DD advice register and kept in a file. Later on, when the DD arrives the date is put on the confirmation slip and the above mentioned procedure is applied.

When the situation of payment arises concerned officer checks out whether it is crossed or not.

If it is crossed he should just transfer the amount to the account mentioned in the DD by crediting the account and debiting If all the particulars are all right and the payee is genuine bank made the payment.

PAY SLIP:

Pay slip is generally used for bank’s internal payment purpose. It has been observed that the bank has issued a pay slip in the name of payee then the principal office has sent the pay slip with a forwarding letter. Two copy of the forwarding have sent to the Head office. In the photocopy of the forwarding the authorized officer has given signature has written “received” so that this paper can be used as a document that the Head Office has got the pay slip with in order. This paper has put in the principal office as a document. Then the pay slip has been given to the person, the creditor of the bank as a supplier.

TELEGRAPHIC/ELECTRONIC TRANSFER:

There may be certain types of fund transfer for which a customer may wish to specify the payment system in its instruction to the Bank. In such cases, the Bank will attempt to execute the instructions as specified by the Customer. Prime Bank Limited reserves the right to route the funds transfer via any means available in order to execute the transfer instructions on the specified payment date. Neither the Bank nor subsequent banks in the process will necessarily investigate discrepancies between names and identifying or account numbers and may execute instructions on the basis of the number given in the instructions even if such number identifies a person different from the named bank or beneficiary.

ONLINE BANKING:

Online banking is the banking activities conducted from home, business, or on the road, instead of at a physical bank location. It has capabilities ranging from paying bills to securing a loan electronically. It saves time and money for users. Considering these, PBL started online services with several branches. It is available for all customers- both cash deposit and withdrawals, cheque deposit and transfer in CD, SB, STD, and Loan accounts.

DATA ENTRY SECTION:

A strong computer network system exits here. Total 16 PC are available here and all are connected with LAN. Three PC of foreign exchange department is connected with internet for foreign transaction of L/C and others. One is connected with all branches of PBL for online transactions. But a separate section exists in general banking section. Two officers and two computers are available in this section. They perform all type of posting of the day of this branch; make statement for the customer about their financial status and produce various types of statement and supplementary documents for future reservation and verifying purpose.

CASH SECTION:

The Prime Bank Limited has a heavy equipped cash section. Cash is received and disbursed in this section. The cash section consists of three junior officers.

CASH RECEIVE SECTION:

Any person can deposit money by filling up the deposit slip or pay in slip and gives the form along with the money to the officer. The officer checks the A/C number, amount of taka both in words and in figure. Then the officer gives the entry to the receiving cash book and also writes the denomination of currency at the book of deposit slip. Then the officer sends the deposit slip counterfoil credit voucher and cash book for rechecking the particulars and for a second signature. After this second signature stamp “cash received” is given over the credit voucher. At the end of the day total of scroll book are entered in the cash book and total of the credit vouchers are found out and checked with the previous entries. The process is same for cash received the date of the next day.

CASH DISBURSING SECTION:

The PBL received various financial instruments for encashment. The common instrument handled by the branch is cheque, demand draft, pay orders, and debit cash vouchers etc. This instrument is hacked for apartment tenor. If the instrument is all right it is sent for posting by computer. After posting, signature is verified by the head. Then the cheque is sent for cancellation. After checking the A/C number, payee instruction and date the cancellation, officer cancels the cheque. Ther after the payment is done. The process is same for other financial instrument along with the clearing step. Bearer cheque is paid in cash cross cheque is balanced to the A/C.

TRANSACTION CASH MONEY:

At first the cash officer gives some money from the vault to the officer who makes payment to the clients and keeps a record of that amount. There are two teller desk from which the payment is being made. At the end of the payment period the balance must be adjusted with the records of the transaction. That is the received balance; the payment balance must be similar with the balance on the receiving and the payment register book.

CASH BALANCE BOOK:

This is a book on which the balancing record of the cash has maintained, the opening balance has to be always the previous day’s closing balance. At the end of the transaction hour, all the receipts have to be added with opening balance and then the payments have to be deducted from the total balance. After deducting this balance has constituted the opening balance of the next transaction day. This is the process of maintaining the opening and closing balance of cash in Prime Bank Limited which have observed by this duration.

CHEQUE SECTION:

Cheque book issue has described below in terms of some cases observed in the bank.

Cheque book issue to the person except owner of the accounts:

It has been observed that a client that is owner of the account has wanted to draw a cheque book by another person from the bank then the authorization letter of the owner to draw this cheque book must have submitted by the bearer. In the authorization letter the bearer’s signature must have to be verified by the owner of the account.

Cheque book issue to the account holder:

When an existing account holder wants to draw a cheque book from the bank then he comes to the bank with the requisition slip which is already fixed in the cheque book that was delivered to him before this newly one. There is acquisition slip in every cheque book issued by the Prime Bank Limited.

It has been observed that if the owner of the account has wanted to draw a cheque book by a bearer then the bearer’s signature has appeared on the top left hand side (on the back of the requisition slip) on the requisition slip. And the bearer signature has been authenticated by the account holder by a signature, which has appeared on the bottom left hand side (on the back side of the requisition slip) just below the bearer’s signature.

When the cheque book is lost:

It has been observed that when a cheque book has been lost by an account holder, the holder of the account must have filled a indemnity bond which have been authorized by a guarantor. The guarantor must have to maintain an account in the Prime Bank Limited and the signature of the guarantor must have to appear on the indemnity bond.

Indemnity Bond:

Indemnity bond describes that if there is any loss or liability for the issuing of this new cheque book despite the old cheque book is lost; the guarantor will be liable for this loss or liability.

Process:

At first the requisition slip has to be filled by the account holder. On the requisition slip the main components are:

1) The name of Bank

2) The name of the branch

3) Date

4) CD/SB Account No

5) Containing no. of leaves

6) Name of the account

7) First serial no and last serial no of the leaf

8) Address of the account holder

9) Signature of the account holder

10) Signature of the authorized officer

Then these components have to be filled by the account holder, the authorized officer and the cheque book issued who are on the desk for giving services to the client. The desk man then gives entry in the “Cheque Book Issue Register”. The components on the register book are date of issue, cheque serial no, account no of the account holder.

CLEARING SECTION:

This department has three main jobs. They are:

- Inward cheque clearing

- Outward cheque clearing

- Attending house

Inward Cheque Clearing:

This is the opposite flow of the Inward cheque clearance. When PBL’s cheque sends to other person of other Bank, that Bank will do the same thing to claim money from Prime Bank Ltd. with the same procedure like Inward clearing of that Bank. At the time of Outward Cheque for clearing, the things must have to be checked: The Clearing Seal, The Endorsement Seal, and The Branch Seal.

Outward cheque clearing:

Whenever any branch of Prime Bank Ltd. receives a cheque of other Bank to collect money, then the branch sends the cheque to its Head Office. The Head Office arranges the cheques separately by the name of different bank and then it send to the respective bank for clearance by the clearinghouse. Those cheques of different Bank to collect money for the ordered person are called Inward Cheque for clearing. Then these cheques go for entry in to the Inward Registry Book and Database of Clearing Department.

Bangladesh Bank conducts this job of clearinghouse name HOUSE. This is done twice a day- First house and Return house. First house is to deliver cheques and collect cheques from other banks. Return house is to return the honored cheques. The practice among the bank is to give only the name of those cheques, which were not honored.

Note: Bangladesh Bank keeps separate A/C for the entire bank and settles the balance considering the flow of cheque in both ways that is Inward & Outward.

As soon as the principal branch gets the clearance it sends an Inter Branch Transaction Advice (IBTA) to the branch, who has sent the cheque for collection. Receiving the IBTA is considered as clearance for the payment to the party.

- Cost of clearing:

The collection cost normally varies with the distance and PBL does not take any charge for collection within DhakaCity or within the district. But when anyone issue check of PBL without having enough sufficient money in the account, the clearing dept. will cut Tk.100 fine for this.

- L.B.C:

The word LBC means Local Bills for Collection. It is applied on transaction between inter branch. Issuing cheque/DD from one branch to another branch of the same Bank. Suppose Gulshan branch have issued a cheque to Banani branch. After received the cheque the Banani branch will give a seal of Crossing, LBC seal and Endorsement seal on that check and will issue forwarding on Gulshan Branch.

IBTA: Inter Bank Transaction Account

I.B.C :

IBC means Inward Bills for Collection. It is the reverse of LBC. In this case gulshan branch will receive cheque and give a seal of Crossing, LBC and Endorsement seal on the cheque and send it to Banani branch with an Advise.

The transaction will be as follows:

Check A/C Debt.

IBTA Gulshan Cr.

- O.B.C:

The word OBC means Outward Bills for Collection. There are two types of OBC:

1) Outside Zone

2) With Different Branch

1) Outside Zone:

It is used only for issuing DD or TT. Under this system any other bank of different area can issue DD/TT to this branch. The TT is used for inter branch transaction.

D.D: Demand Draft

T.T: Telegraphic Transfer

2) With Different Branch:

Under this system clients can issue DD/TT to different branches of this Bank

Receiving of cheques:

It has been seen that when the cheques of Sonali Bank, HSBC etc. has deposited in the Dhaka, Uttara branch of Prime Bank, the different accounts which have been maintaining in those particular branches then that particular branches have sent that instrument to the local office (Prime Bank) for collection.

IBCA to the branches:

Then the Prime Bank (Local Office) has given an IBCA in the hand of the sender of those particular branches and has taken a signature on a register book. IBCA bears the documents of the total amount of cheques received by the local office from the particular branches. IBCA has described that the Prime general accounts (those particular branches) have credited.

Sorting and Scheduling:

The Prime Bank (local office) then has made the schedule of the cheques drawn on different banks. That the bank has separated those instruments according to the bank wise and then separated according to branch wise. Then the bank has added the figures of the instrument for the particular branches in a schedule paper.

Given entry to the Computer:

The bank has given entry to the computer. There some row box in the clearing. These are from the bank, to the bank, account number, cheque serial number, branch name, issuing date etc.

If the balance of Prime Bank in the Bangladesh Bank account has shown the debit figure then it has been assumed that the drawn amount of instruments drawn on Prime Bank by other banks has exceeded the amount of instruments drawn on other banks by P rime Bank.

Return of the instrument:

It has been seen that when some instruments have been returned from other banks to the local office of Prime Bank. Then the bank has put those in the drawer and then the bank has written a letter to owner of instruments to make them known about the matter. The instruments have been turned with a “Return Memo” which has shown the reasons for what the instruments have been dishonored. When the client has withdrawn the returned instrument from the bank the bank officer has written on the pay slip return.

IBDA:

When the instruments of the Prime Bank (another branches) have been returned from the other bank on which the instruments have been dawn, the Prime Bank has sent a IBDA (Inter Branch Debit Advice) to that branch separately amounting to the instruments received from that particular branches of Prime Bank.

ACCOUNTS SECTION:

1) Collection of clearing cheque from client and send to the main branch to present clearing house for collection without any charge.

2) Computer entry of clearing cheque and credit posting.

3) Voucher sorting reconciliation with supplementary summary.

4) Voucher arrangement and preparation of voucher cover.

5) Preserve daily cash position trial balance.

6) To prepare salary sheet and record all the stationary cost.

7) To provide solvency certificates.

8) If the supplementary summary and voucher are not same his duty to find out the discrepancies. And other works demanded by the authority

DISPATCH SECTION:

This section is responsible for receiving the entire letter from outside of the bank and to send the entire letter from the bank. For this the section keeps a register book. It’s also received the entire document and anything addressing the book. However two types of letters are continuously received in the branch. These are:

1) Inward (registered/ unregistered) letters.

2) Outward (registered/ unregistered) letters.

This is in short about general banking which I have learned from the bank at the time of my internee period. If the cash received and cash payment, transfer received and payment are same and no fraud is found then the day transaction is closed and it is time to go.

Dispatch division mainly operates the functions of dispatching the intimation letter to the client, IBCA, IBDA, OBC to the other banks for their internal transaction with the banks. Dispatch division receives the documents come from the negotiating bank, from the opening bank (incase of export) and any other documents, letter, papers etc. in the name of main branch (Prim Bank). The officer engaged in the dispatch division maintains a register book to keep entries those documents. When the officer receives paper from outside then the officer seals on that paper “received” and when the officer sends paper to the outside of the bank then the bank seals on the paper “dispatch” and puts his signature on that documents.

SWOT ANALYSIS:

The acronym for SWOT stands for:

- STRENGTH

- WEAKNESS

- OPPURTUNITY

- THREAT

The SWOT analysis comprises of the organization’s internal strength and weaknesses and external opportunities and threats. SWOT analysis gives an organization an insight of what they can do in future and how they can compete with their existing competitors. This tool is very important to identify the current position of the organization relative to others, who are playing in the same field and also used in the strategic analysis of the organization.

|

Banking Experience of 12 years provides PBL the strength of being one of the market leaders in the sector. This strength of PBL is totally unmatched by any other commercial bank in Bangladesh, as the long term success of a bank heavily depends on its reputation while dealing with every sensitive commodity like money.

PBL received many awards during 2006. PBL is the recipient of 1st prize under ICAB National Awards 2005.

- Credit Rating Information and Services Limited (CRISL) rated the Bank as A+ Considering its good profitability, best asset quality and diversified product lines.

- As the 6th largest listed company at Dhaka Stock Exchange PBL has strong confidence among the investors, both individual and institution.

- PBL focus strongly on remittance business and with that aim they opened rural branches where remittance business concentrates. PBL opened Exchange House at Singapore, Prime also entered into agreement with various exchange houses at USA, UK, Middle East and South Asian countries for inward foreign remittances of the wage earners.

- To be the most efficient Bank PBL has chosen T24 of Temenos Holdings, NV Netherlands Antilles as the core banking Software (CBS) for the first time in Bangladesh.

- In Bangladesh PBL has wide range of customer base and is operating efficiently in this country.

- PBL has a bulk of qualified, experienced and dedicated human resources.

- PBL has the reputation of being the provider of good quality services to its potential customers

|

- PBL has fewer branches than their competitors. Such as PBL have only 61 branches whereas Uttara Bank Limited has 205 branches and 12 regional offices.

- PBL do not provide any ATM facility to the customers. This is one of the major weaknesses of PBL.

- The population of Bangladesh is continuously increasing at a rate of 7.3% per annum. The country’s growing population is gradually and increasingly learning to adaptation of consumer finance. As the bulk of our population is middle class, different types of products have very large and easily pregnable market.

- The activity in the secondary financial market has direct impact on the primary financial market. Investment is a national socio economic activity. And activity in the national economy controls the bank.

- PBL is now focusing on lending to SME and Retail sector. The bank is not only providing credit but also decided to popularize the SME sector by participating in various trade shows organized in the country.

- Bangladesh has a huge consumer base for maintaining several accounts. So PBL has the opportunity to keep these customers by reducing its current fees and charges.

|

- In today’s economy, substantial amount is remaining idle and currently the investment in the secondary market by foreign is relatively low. These economic situations of the country indicate political threats.

- Increased competition by other banks is also another threat to PBL. Furthermore, the new comers in private sector like Dutch Bangla Bank, Exim Bank, BRAC Bank, Southeast Bank, Mercantile Bank, Islami Bank are also coming up with very competitive force.

PROBLEMS IDENTIFIED:

There are some problems of Prime Bank Ltd. faced by clients. These are given below:

- Where computer leads every sphere of lives including banking activities,

- PBL bank does not have experts in computer.

- The number of employee is poor

- There is no uniformity in their fixed pricing.

- All branches of the bank are not online banking system.

- It has no ATM facility.

- Most of the clients also face to fill up the A/C opening form.

- When the clients come to close an account they get their money after

two or three days. Now a day’s it should not be for a commercial bank.

- To write Voucher for every transaction is so difficult, and it consumes time.

RECOMMENDATION:

Prime bank is one of the local banks in our country. So, this bank has some advantages to capture the market to generate capital and profits from this market. But the thing is that like other local bank this bank cannot gain enough profit. Obviously there are some reasons behind this. Some of them have been mentioned. To overcome these problems I have tried to search some solutions. These are followings:

- Firstly, the management has to think about quicker services to the customers. Like Online banking systems, though it has been introduced. But many of the employees are not expert on computer literacy. The management should train them effectively.

- Their interest rate on FDR varies client to client. Like, the interest rate should be fixed for all. This things also a barrier to create a good image.

- The management should think about the A/C opening form. They should try to make it easier to understand. There are no bindings that the form must have to be in English. They may introduce it by Bangla.

- PBL can make a database to maintain the registry records in Computer. It may make the activities faster.

- PBL may introduce some better alternative of “Voucher”. Because it takes more time to write many for a single matter. So, the management should build up a database system for this, or they should go for the writing and posting system of Voucher by the same person.

Every people have some limitations. The bank is rune by the people. So, the bank may have some limitations also for their employee’s. But he is the winner who can overcome these problems quickly and update the systems time to time.

CONCLUSION:

Prime Bank Ltd has emerged itself as one of the most disciplined and promising banks in the commercial banking sector in Bangladesh under the active supervision of its competent management team led by Mr. M. Shahjahan Bhuiyan. In this competitive market Prime Bank Ltd. competes not only with the others commercial banks but also with the public Bank sector banks and has been able to throw in more positive contributing towards economic development of Bangladesh as compared to other banks.

Prime Bank Ltd. invests comparatively more funds in export and import businesses. It has been operating its foreign exchange operation with great success and been able to make positive contribution to the economy of Bangladesh by virtue of its devoted and expert personnel. Prime Bank Ltd is considered to be specialized in Foreign Exchange Operation. That is exactly why with in a very short period of time, Prime Bank Ltd. has positioned itself one of the leading bank in Bangladesh.

To the gateway to practical professional life, an experience at PRIME Bank Limited as an intern was a privilege for me. Prime Bank Ltd. does offer a real practical orientation to the new comers with typical corporate culture. This three months internship orientation with Prime Bank Ltd. undoubtedly will help me a lot to understand and cope with any future typical corporate culture.