1.1 Introduction: The internship program of BBA students of Department of Marketing, Institute of Business Studies, DarulIhsanUniversity, is an imputing part of the BBA program, 3 credit hours are for this internship program, out of 135 credit hours of the program. The program is for 3 months duration. However, I was assigned to UTTARA BANK LTD to complete the program.During this period I have worked closely with the employees of the UTTARA BANK LTD. A student must submit one copy of report on the assignment topic to the faculty supervisor, to the director of report of BBA program and to the host supervisor after the completion of the program period.

1.2 Rational of the Study

Theoretical knowledge is not enough for a student. Because there lies a far difference between theoretical knowledge and practical knowledge. Theoretical knowledge applied in practical field. So, these two may be synchronized. Our internship program is launched mainly for this purpose. Other purpose that may be is to know about the rules, regulations, management, and environment of an organization before getting a job. To gather some experience that will help a student to get a good job or may also be another purpose of the study.

1.3 Objectives of the Study:

The internship experience is meant to serve as a bridge between the theoretical learning of students and the practical application of the same.

The objectives of the study are categorized as below:

a) General:

- To carry out effective and comprehensive accounting system that followed by the management of Uttara bank Ltd. As a financial institution.

b) Specific:

- To develop knowledge about accounting system of Uttara Bank Ltd.

- To identify the strengths and weaknesses of the accounting system overall operation and monitoring process in Uttara Bank Ltd

- To make recommendations regarding the Bank’s overall accounting system.

1.4 Scope of the study:

The Uttara Bank Ltd. is a private Ltd Bank where all types of financial transaction took place. It is the second largest private commercial Bank in Bangladesh. It has a massive network all over the country with 198

Branches in the country. It contains separate functioning division that furnished all types of activities. I have the opportunity to do everything practically, which is helpful to gather experience. I have got the opportunity to work at all the important desk of the Uttara Bank Shymoli Branch. As the Bank doing Branch Banking rather than Unit Banking. So I can have a very clear scenario of the all Branches accounting System in other words the accounting system of the Uttara Bank Lt as well. The liability side of the Balance sheet that is deposit collection and the system it is maintained. The asset side of the Balance sheet that is advance/loans/Credit. Selection of borrower, system of choosing the correct borrower, approval of loan. Providing the advance to the customer. having the proper documentation. This documentation is very important in case of lending for a Bank to meet up the legal procedure. Here some documents called the Prime Document. Banks also keep some other security in the name of Collateral Security to safeguard the Banks interest. Here the Banks often keeps Primary Security in support of Secondary Security or addition security.

1.5 Methodology:

Sources of Data:

Both primary and secondary sources of data have been used in this study:

1) Primary sources:

Among the primary sources, the main sources are:

i) Face to face interview of the employees of the Uttara Bank Ltd.

ii) Official record of related section of the Uttara Bank Ltd.

iii) Direct interaction with the customers.

2) Secondary sources:

i) Annual Report of the Uttara Bank Ltd.

ii) Relevant Books of the Uttara Bank Ltd. and

iii) Uttara Bank Ltd. website.

1.6 Limitation of the study:

Like other study, my study has some limitations also. The organization on which I have studied is a Branch of Uttara Bank Ltd. at Shymoli. It is a private Bank in Bangladesh. The main limitations are:

- The main limitation that I faced during conducting the study was lack of access to information considered confidential by employees of Head Office due to strategies.

- Shortage of time: I could not get into the depth of the Study due to time limitation.

- Insufficiency of necessary information of data.

- Lack of proper explanation of records and documents.

- Inaccurate or contradictory information.

- Field practice varies with the standard practice that also created problem.

Overview of the Uttara bank Ltd.

- Introduction

- Objectives & Nature of the Uttara bank Ltd.

- Capital of the Uttara bank Ltd.

- Organization structure & Department of the Uttara bank Ltd.

- Management of the Uttara bank Ltd.

Board of Director

Overview of Uttara Bank Ltd:

2.1 Introduction:

Uttara Bank ltd is closely related from very beginning history, tradition, and people life of this country. This Bank established at first privately named “Eastern Banking Corporation” since January 28,1965. The mission statement of the Bank is

“ Abohoman Banglar Oitijhya Lalito”. Before the start of Eastern Banking Corporation it was Nath Bank. This Nath Bank was situated at the Mymensingh region. All the asset and liability of Nath bank were taken by the then Eastern Banking Corporation. Before liberation the Bank was one of two Bangali owned Bank in Pakistan with the fastest growth. After liberation the Bank was nationalized and named Uttara Bank in 1972. After reduction of capital under privatization policy of government it got permission to work as privately named Uttara Bank ltd since the month September 1983.This Bank is registered on June 29, 1983 and get certificate to operating business activities at August 21, 1983. The registered office of this bank located at 90 Motijhil, C/A , Dhaka-1000.This bank operates its activity allover the country through its 198 branches. Uttara Bank ltd enlisted in Dhaka Stock Exchange ltd by selling its share in 1984. It enlisted in Chittagong Stock Exchange ltd in 2004.

2.2 Objectives and Nature of the Uttara Bank Ltd.:

Uttara Bank Ltd-one of the largest and oldest private-sector commercial bank in Bangladesh. With years of experience adaptation of modern technology both in terms of equipment and banking practice ensures efficient service to clients. 198 branches at home and 600 affiliates worldwide create efficient networking and reach capability. Uttara is a Bank that serves both clients nationally and internationally.

2.3 Capital of the Uttara bank Ltd.

| Capital | 2005 | 2004 |

| Authorize Capital 20,00,000 Ord Sh of Tk 100 each | 20,00,00,000 | 20,00,00,000 |

| Issued Capital 10,00,000 Ord Sh of Tk 100 each | 10,00,00,000 | 10,00,00,000 |

| Paid up Capital 9,98,324 Ord Sh of Tk 100 each | 9,98,32,400 | 9,98,32,400 |

| Proposed Bonus Share 9,98,324 Sh of Tk 100 each | 9,98,32,400 | |

| Statutory Reserve | 51,08,37,039 | 51,08,37,039 |

| Others Reserve | 115,09,62,512 | 113,09,62,512 |

| Profit and Loss Account balance | 35,69,539 | 7,78,411 |

| Shareholders total equity | 4206,22,01,299 | 3970,09,32,623 |

2.4 Organization structure & Department of the Uttara bank Ltd.

Head Office

Chairman’s Secretariat

Managing Director’s Secretariat

Board Department

Share Department

MIS & Computer Department

Establishment Department

Stationary & Records Department

Transport Department

Human Resources Division

Personnel Department

Test Key Department

Disciplinary Department

Marketing Division

Business Development Department

Branches Department

Engineering Department

Public Relations Department

Credit Risk Management Division

Credit Approval Department

Credit Admin & Monitoring Department

Credit Marketing Department

Credit Recovery Department

Central Accounts Division

Accounts Department

Reconciliation Department

Internal Control & Compliance Division

Audit & Inspection Department

Monitoring Department

Compliance Department

International Division

Treasury Division

Foreign Remittance department.

Regional Offices.

Whole country is divided in to 12(twelve) Regions headed by not less than Deputy General Manager ranking Officer. The regions are as under.

Regional Offices | Headed By |

| Dhaka Central Zone | General Manager |

| Dhaka North Zone | General Manager |

| Dhaka South Zone | General Manager |

| Narayanganj Zone | Deputy General Manager |

| Mymensingh Zone | Deputy General Manager |

| Chittagong Zone | General Manager |

| Comilla Zone | Deputy General Manager |

| Rajshahi Zone | Deputy General Manager |

| Bogra Zone | Deputy General Manager |

| Barishal Zone | Deputy General Manager |

| Khulna Zone | Deputy General Manager |

| Sylhet Zone | Deputy General Manager |

2.5 Management of the Uttara bank Ltd.

Mr. Azharul Islam

Mr. Md. Asaduzzaman

| Mr. Md. Mahfuzus Subhan | Prof. Mirza Mazharul Islam |

| Mr. Sarwar Boudius Salam | Prof. Sharif Md. Shahjahan |

| Mr. Abu Hossain Siddique | Mr. Syed A. N. M. Wahed |

| Mr. Abul Barq Alvi | Mr. Mustafizur Rahman |

| Mr. Faruque Alamgir | Mr. Shah Habibul Haque |

| Col. Engr. M. S. Kamal (Retd.) |

Mr. Shamsuddin Ahmed

| Chairman | Mr. Azharul Islam |

| Vice Chairman | Mr. Md. Asaduzzaman |

| Directors | Mr. Md. Mahfuzus Subhan |

| Mr. Sarwar Boudius Salam | |

| Mr. Abu Hossain Siddique | |

| Mr. Shah Habibul Haque | |

| Managing Director | Mr. Shamsuddin Ahmed |

3.1 Deposit Schemes

3.1.1 Foreign Currency

- (a)Non Resident Foreign Currency Deposit Account (NFCD)

- (b) Foreign Currency Account

- (c) Resident Foreign Currency Deposit Account (RFCD)

3.1.2 Local Currency

- (a) Savings Account

- (b) FDR Account

- (c) STD Account

3.2 Loan/Advance Schemes

- 3.2.1 Consumers Credit Scheme

- 3.2.2 Personal Loan Scheme

3.3 International Banking

3.4 Treasury and dealing room

3.5 Lease Financing

3.6 Home Remittances

3.1 Deposit Schemes

3.1.1 Foreign Currency

3.1.1(a) Non Resident Foreign Currency Deposit Account (NFCD)

- All Non-Resident Bangladesh nationals and persons of Bangladesh Origin including those having dual nationality ordinarily residing abroad may open this account with any AD branches of Uttara Bank Ltd.

- The NFCD account may be opened in single/joint name for a period of 1, 3, 6, 12 months.

- This account may be maintained as long as account holder desires.

- On maturity the account holder can encash it in local currency or can transfer the amount including accrued interest anywhere he likes.

- Initial deposit US$ 1000 or GBP 500 sterling or equivalent currency.

- The account offers attractive interest Payable in foreign and tax free.

- The account with accrued interest can be renewed either of the instruction of the account holder or be renewed automatically if there is no instruction otherwise.

- No interest is given on premature encashment.

NFCD Interest Rate:

| Currency | 1Month | 3Month | 6 Month & Above |

| US$ | 0.8000 | 0.7775 | 0.7200 |

| GBP | 3.0075 | 2.9875 | 2.9100 |

Requirement for opening of the account

- Account opening form as per format supplied by the Bank. The account opening form and signature card to be filled in and duly signed.

- Two copies passport size photographs of the account holder.

- Photocopies of the first 7 pages of the passport duly attested by the remitters bank/exchange companies having drawing arrangement with UBL or by Bangladesh Mission abroad.

3.1.1(b) Foreign Currency Account

A) Foreign Currency Account for private individual/firm/organization.

- Any person/firm/organization who earns foreign currency can open Foreign Currency Account with UBL.

- Payments in foreign currency may be made freely abroad from this account and local payment in Taka may also be made from this account.

- Bank pay interest provided the accounts are maintained in the form of term deposit for minimum period of 90 days.

Requirement for opening of the account.

- Account opening form as per format below. The account opening form and signature card to be filled in and duly signed.

- Two copies passport size photographs of the account holder duly attested by remitter’s Bank/Embassies

- Photo copies of the first 7 pages of the passport duly attested by the remitters bank/ exchange

- Companies having drawing arrangement with UBL or by Bangladesh Mission abroad.

B) Foreign Currency Account for Bangladeshi Nationals Working and earning abroad.

- No initial deposit is required.

- A/c holder may nominate his nominee to operate the account.

- The account holder can freely transfer entire amount in foreign currency anywhere he chooses or can convert into Bangladeshi Taka currency.

- Funds from this account may also be issued to the account holder up to his entitlement for the purpose of his foreign travels in usual manner.

Requirement for opening of the account:

Ø Account opening form as per format below . The account opening form and signature card to be filled in and duly signed.

Ø Two copies passport size photographs of the account holder.

Ø Copies of employer’s certificate/work permit.

One copy of the passport size photograph of the nominee if any to be attested by the account holder

Photocopies of the first 7 pages of the passport of the account holder.

3.1.1(c) Resident Foreign Currency Deposit Account (RFCD)

RFCD

Resident Foreign Currency Deposit Account

- Persons ordinarily resident in Bangladesh may open and maintain RFCD Account with foreign exchange brought in at the time of his return from travel abroad.

- Any amount brought in with declaration to customs authorities in the form FMJ and up-to US$ 5000 brought in without any declaration can be deposited in this account.

Balance in this account can be freely transferred abroad.

- Funds from this account may also be issued to the account holder for the purpose of his foreign travels in the usual manner.

- Interest in foreign currency is paid in this account if the deposits are for a term of not less than one month and the balance is not less than US$ 1000 or GBP 500 or its equivalent.

RFCD Interest Rate | |

| Currency | Interest |

| US$ | 0.7000% |

| GBP | 2.9075% |

Requirement for opening of the account

- Account opening form as per format below. The account opening form and signature card to be filled in and duly signed.

- Two copies of passport size photograph of the account holder.

- Photocopies of the passport and the relevant pages showing evidences of traveling abroad.

3.1.2 Local Currency

3.1.2(a) Savings Accounting System.

The savings accounting system will accommodate various types of savings plans. Designed to allow one time entry of the customer information which may be tied to as many accounts as necessary. Accounts are set up based on size type class and reports may be generated accordingly. Compounding may be done daily, monthly, quarterly, half yearly basis. Normally compounded half yearly basis but in case of employees account and some special account it may be at the daily basis. Deposits and withdrawals may be made at any time. In case of big amount a seven day notice is required but there is flexibility, actually the notice is taken for the safety of the depositor. Statements are created individually and send to the customer (Depositor) half yearly basis but the statement is also available on demand. Inquiry of customer or accounting balances is always available. Average daily balance ADB designed to work with general ledger systems, produces a balance according to accounts for the purpose of monitoring trends is also included. Customer waiting list, Current customer waiting list, current customer list, mailing labels, Slabs on the basis of deposit amounts designated by the central bank. An amount of incidental charge of taka 50.00 is charged half yearly basis if the amount of deposit fallen down a certain size. An amount of Government duty (Excise duty) started from taka 150.00 to 5000.00 (amount fixed by the Government may change time to time) is charged yearly basis against the deposit slabs fixed by the Central Bank.

Requirement for opening of the A/c.

- Account opening form as per format below. The account opening form and signature card to be filled in and duly signed.

- Two copies passport size photographs of the account holder.

- Photograph of nominee (if any) duly attested by the account holder.

- Photocopy of the 1st 7 pages of the passport for non-resident Bangladeshi national.

- Signature in the account opening form/card must be same with the signature of the passport.

3.1.2(b) FDR Account (Fixed Deposit.)

Designed as the complete management system for the safe deposit . The system will support global regional or branch pricing with the ability to add a discount percentage to any box ( ie senior citizens, employees etc.)Income projection for any month is available. State source tax can be assessed with exceptions for tax exempt individual or organization. Branches may have their individual tax rates. You may mark a box frozen in the event of death or a court order. A record may be kept of openings for the courts. Included you will find easy daily and monthly routines. The product incorporates a built-in tickler system. Income projection for any month is available. We may maintain waiting lists for the first available box, and specific box sizes. Standard notices include. Many reports are available including, Available Box list, Customer waiting list, Current customer waiting list, current customer list, mailing labels, slabs on the basis of deposit amounts designated by the central bank. An amount of Government duty (Excise duty) started from taka 150.00 to 5000.00 (amount fixed by the Government may change time to time) is charged yearly basis against the deposit slabs fixed by the Central Bank

Requirement for opening of the A/c.

- Any Bangladeshi national residing home or abroad may open FDR with UBL.

- FDR may be opened single/joint name for a period of 3, 6, 12, 24 and 36 months.

- UBL offers attractive/competitive rate of interest in FDR.

3.1.2(c)STD Account Short term Deposit Accounting System.

This product will effectively manage any number of sizes classes types or sizes. Actual and current report is available on spot on request. Here interest is given against this type of deposit on daily basis but here interest rate is lower. But this type of account is of very useful for the business personalities. Many reports are available including, Available Box list, Customer waiting list, Current customer waiting list, current customer list, mailing labels, Slabs on the basis of deposit amounts designated by the central bank. An amount of incidental charge of taka 100 is charged half yearly basis if the amount of deposit fallen down a certain size. An amount of Government duty (Excise duty) started from taka 150.00 to 5000.00 (amount fixed by the Government may change time to time) is charged yearly basis against the deposit slabs fixed by the Central Bank

- Govt, Semi-Govt, Autonomous, Non Government organization (NGO) Public Limited , Private Limited and an individual may open STD Account with UBL.

- UBL offers attractive/competitive rate of interest in STD Account.

- 7 days notice required to withdraw big amount.

- Head Office permission is needed to open NGO accounts.

- Memorandum of articles, Memorandum of association, Cirtificate of Incorporation, TIN, VAT and other necessary papers are needed.

3.2 Loan/Advance Schemes

Loan accounting systems.

Loan service plus : the most portable system on the market today. Can be configured from one to unlimited users handling up to 16 million loans.

Loan portfolio: the same core transaction prosing as the larger loan service system. But designed with the small user in mind.

Basic Criteria: What You should expect from any loan servicing system that you use.

Benefits : FAS has invested in extra benefits for the user by using larges ever concepts applied in a PC environment.

Reports : FAS has developed many reports to balance the accounting and general ledger needs of your organization.

Summary : General summary of important feature.

Economic Development Summary : general summary of important Economic development edition feature.

Comparison : Loan service plus vs Loan portfolio products comparison.

3.2.1 Consumers Credit Scheme

UBL started Uttaran Consumers Credit Scheme from 1996.

UBL offers opportunity of Financial assistance for:

- Motor cycle/car- New or re-conditioned.

- Refrigerator/ Deep Freeze.

- Television/ VCR /VCP/VCD

- Radio/ Two-in-one/ Three – in – one

- Air-Conditioner/ Water Cooler/ Water Pump

- Washing Machine.

- Personal Computer/ UPS/ Printer/ Type writer

- Sewing Machine.

- House hold furniture- Wooden & Steel.

- Cellular Telephone.

- Fax

- Photocopier.

- Electric Fan- Ceiling/ Pedestal/ Table.

- Bi-Cycle

- Dish Antenna.

- Baby Taxi, Tempo/Microbus (For self employed persons)

- Kitchen articles such as Oven, Micro-oven, Toaster, Blender, Pressure Cooker etc.

- No collateral security is required.

- Simple rate of interest.

- Quick sanction

- Maximum Loan amount Tk.3,00,000/-

- 5% incentive on total interest charged

Special Features

3.2.2 Personal Loan Scheme

Personal Loan Scheme for Salaried Officers

UBL started personal loan scheme for salaried officials of reputed organizations from 1999 to meet :-

- Emergency expenses for own marriage of a service- holder or his dependents.

- Emergency expenses of urgent surgical operation/ medical treatment.

- Emergency educational expenses of the children for admission/purchase of books, examination fees etc.

- Any permanent salaried employee aged between 20 to 55 years is eligible to get loan.

- No collateral security is required.

- Maximum Amount of loan Tk. 1,00,000.

- Maximum period of loan up to 3 years.

Special Features

3.3 International Banking

UBL is equipped with all modern technology & provides following international banking services.

- Plays vital role in import / export and other foreign currency of the country through more than 600 foreign correspondents world wide.

- Renders fastest service to the exporter and importer through its SWIFT service.

- Offers competitive price for importers and exporters.

- Provides support to the exporter and importer by extending working capital, pre-shipment, post- shipment facilities.

- Upholds its commitment in international payment

3.4 Treasury and dealing room

UBL has got its independent treasury and dealing room equipped with Reuters Dealings System and provides.

- Effective service to the client.

- Daily exchange rate buying and selling.

- Forward cover at competitive price.

- deals in foreign currency with Central Bank, Commercial Bank and other potential clients.

- Buying and selling third currency with all leading banks worldwide.

- Covers exchange fluctuation risk by providing competitive premium.

Value Date :20-09-2006 Dealing rates to customer : SELLING BUYING TT & OD B.C Currency T.T. Clean TT (DOC) OD Sight (Exp.) OD Transfer

67.3500 67.4000 U.S. DOLLAR 66.3000 66.2740 66.2084 65.9950 86.2056 86.2690 EURO 84.0673 83.9691 83.8285 83.7352 0.5855 0.5859 J.YEN 0.5626 0.5622 0.5605 0.5602 127.3917 127.4859 G.B.P 124.3469 124.2413 123.8634 123.7857 60.0728 60.1172 CAN. DOL 58.6569 58.6240 58.4345 58.3962 50.9810 51.0187 AUD 49.7061 49.6748 49.5236 49.5002 17.9862 17.9995 SAUDI. RYAL 17.5932 17.5863 17.5267 17.5119 53.9212 53.9611 SWISS FR. 52.8967 52.8760 52.7071 52.6529 42.6431 42.6746 SING. DOL 41.5859 41.5782 41.4380 41.4039 8.6991 8.7055 HKD 8.4793 8.4775 8.3911 8.3501 18.4430 18.4566 AED 17.9872 17.9801 17.9289 17.9141 Export Bill Usance Rate 30 Days 60 Days 90 Days 120 Days 180 Days

USD 65.6533 65.1009 64.5485 63.9960 62.8911 GBP 123.5990 122.5590 121.5191 120.4789 118.3988 EUR 83.2156 82.5154 81.8153 81.1150 79.7145

CURRENCY PAK. RS IND. RS LANKA. RS NEPAL. RS IRAN RYAL MY. KYAT

USD1= 60.5000 45.9100 102.4700 73.0000 N/A 6.4200 Cash & Travellers Cheque Selling CURRENCY Buying 70.0000 U.S D 69.0000 127.2859 G.B.P. 124.1469 69.9000 USD.T.Cs 68.9000 CROSS RATE IN TOKYO MARKET CURRENCY GBP/USD AUD/USD USD/JPY USD/CAD USD/CHF EUR/USD SELLING 1.8831 0.7536 117.3400 1.1263 1.2509 1.2680 BUYING 1.8826 0.7531 117.3700 1.1267 1.2514 1.2675 |

3.5 Lease Financing

UBL started Lease Financing since Sept’1999.

UBL offers opportunity of Financial assistance for:

- Capital Machinery.

- Heavy Construction Equipments.

- Lift.

- Air-Conditioner.

- Vehicles.

- Medical Equipments.

- Consumer Durables.

- UBL provides 100% fund for purchasing equipment/machinery usually for BMRE purpose.

- No down payment is required.

- Tax benefit.

- Financial Assistance without out flowing own fund.

- Off Balance sheet Financing.

- Prompt Service

Special Features

3.6 Home Remittances

Remittance in Taka currency and in foreign currency from abroad Any Bangladesh national residing, working and earning abroad can remit their earnings in Bangladeshi Taka as well as in foreign currency through the Banks/Exchange Companies having drawing arrangement with Uttara Bank Limited. Such remittances are delivered to the beneficiaries expeditiously through its close/wide net work of 198 branches all over the country. It also ensures delivery of remittance to the beneficiary within 24 hours.

CREDIT MANAGEMENT OF UTTARA BANK LTD.

Part-A PRUDENTIAL REGULATIONS

Regulation-1 Sources and capacity of repayment and cash flow backed lending

Regulation-2 Personal Guarantees

Regulation-3 Per party exposure limit

Regulation-4 Aggregate exposure of a Bank/NBFI on SE sector

Regulation-5 Limit on clean facilities

Regulation-6 Securities

Regulation-7 Loan documentation

Regulation-8 Margin requirement

Regulation-9 Credit Information Bureau (CIB) Clearance

Regulation-10 Minimum condition for taking exposure

Regulation-11 Proper utilization of loan

Regulation-12 Restriction on facilities to related parties

Regulation-13 Classification and provisioning for assets

PART-B DEVELOPMENT GUIDELINES

4.2. Policy Guidelines

4.2.1 Product Program Guidelines

4.2.2 PPG Guidelines (for Service Concern)

4.2.3 PPG Guidelines (for Trading & Other Concern)

4.2.4 PPG Guidelines (for Manufacturing Concern)

4.2.5 Segregation of Duties

4.2.6 Credit Approval

4.3. Procedural Guidelines

4.3.1 Approval Process

Duplication Check

Maintenance of Negative Files

4.3.2 Credit Administration

- Credit Documentation.

- Disbursement.

- Custodial Duties.

- Compliance Requirements

4.3.3 Risk Management

- Credit Risk.

- Contract point verification.

- Third party Risk.

- Fraud Risk.

- Application Fraud.

- Liquidity & Funding Risk.

- Political & Economic Risk.

- Operational Risk.

- Maintenance of Documents & Securities.

- Internal Audit.

4.3.4 Collection & Remedial Management

- Monitoring.

- Recovery.

- Collection Objective.

- Identification & Allocation of Accounts.

- Collection/ Monitoring Steps.

- Productivity Tracking.

- Agency Management

4.4 Preferred Organogram and Responsibilities

- Preferred Organizational Structure.

- Key responsibilities.

- Conclusion.

CREDIT MANAGEMENT OF UTTARA BANK LTD.

4.1. Introduction:

Risk is the element of uncertainty or possibility of loss that prevail in any business

transaction in any place, in any mode and at any time. In the financial arena, enterprise risks can be broadly five categorized as Credit Risk, Asset-Liability/Balance Sheet Risk, Exchange Rate Risk, Money Laundering Risk and Internal Control & Compliance Risk.

Credit risk is the possibility that a borrower or counter party will fail to meet agreed

obligations. Globally, more than 50% of total risk elements in banks and FIs are Credit Risk alone. Thus managing credit risk for efficient management of a FI has gradually become the most crucial task. Credit risk may take the following forms:

- In direct lease/term finance: rentals/principal/and or interest amount may not be repaid.

- In issuance of guarantees: applicant may fail to build up fund for settling claim, if any;

- In documentary credits: applicant may fail to retire import documents and many others.

- In factoring: the bills receivables against which payments were made, may fail to be paid.

- In treasury operations: the payment or series of payments due from the counter parties under the respective contracts may not be forthcoming or ceases.

- In securities trading businesses: funds/ securities settlement may not be effected.

- In cross-border exposure: the availability and free transfer of foreign currency funds may either cease or restrictions may be imposed by the sovereign countries.

Credit risk management encompasses identification, measurement, matching mitigations, monitoring and control of the credit risk exposures to ensure that:

- The individuals who take or manage risks clearly understand it.

- The organization’s Risk exposure is within the limits established by Board of Directors with respect to sector, group and country’s prevailing situation.

- Risk taking Decisions are in line with the business strategy and objectives set by BOD.

- The expected payoffs compensate the risks taken.

- Risk taking decisions are explicit and clear.

- Sufficient capital as a buffer is available to take risk.

Credit risk management needs to be a robust process that enables FIs to proactively manage facility portfolios in order to minimize losses and earn an acceptable level of return for shareholders. Central to this is a comprehensive IT system, which should have the ability to capture all key customer data, risk management and transaction information including trade & Foreign Exchange. Given the fast changing, dynamic global economy and the increasing pressure of globalization, liberalization, and consolidation it is essential that FIs have robust credit risk management policies and procedures that are sensitive and responsive to these changes.

The purpose of this document is to provide directional guidelines to the FIs that will improve the risk management culture, establish minimum standards for segregation of duties and responsibilities, and assist in the ongoing improvement of the FIs in Bangladesh. Credit risk management is of utmost importance to FIs, and as such, policies and procedures should be endorsed and strictly enforced by the MD/CEO and the BOD of the FI.

PART – A

Prudential Regulations

REGULATION-1

SOURCE AND CAPACITY OF REPAYMENT AND CASH FLOW BACKED LENDING

Branches shall specifically identify the sources of repayment and asses the repayment capacity of the borrower on the basis of assets conversion cycle and expected future cash flows. In order to add value, the Branches must assess conditions in the particular sector / industry they are lending to and its future prospects. The Branches must be able to identify the key drivers of their borrowers businesses, the key risks to their businesses and their risk mitigates.

The rationale and parameters used to project the future cash flows shall be documented and annexed with the cash flow analysis undertaken by the Branch. It is recognized a large number of SE will not be able to prepare future cash flows due to lack of sophistication and financial expertise. It is expected that in such cases Branches shall assist the borrowers in obtaining the required information and no SE shall be declined access to credit merely on this ground (for details, refer to Regulation – 10).

REGULATION – 2

PERSONAL GUARANTEES

All facilities to SEs shall be backed by the personal guarantees of the owners of the SEs. In case of limited companies, guarantees of all directors other than nominee directors shall be obtained.

REGULATION – 3

PER PARTY EXPOSURE LIMIT

The minimum and maximum exposure of a Branch on a single SE shall remain within the range of Tk. 1.00 lac and Tk. 50.00 lac respectively subject to the following:

a) In case of working capital finance- maximum up to 100% of the net required working capital or 75% of the sum total of inventory and receivables whichever is lower. Please refer to Appendix- VI for calculation of net required working capital.

b) In case of fixed assets purchase – Maximum up to 90% of the purchase price.

REGULATION – 4

AGGREGATE EXPOSURE OF OUR BANK ON SMALL ENTERPRISE SECTOR

The aggregate exposure of our Bank on SE sector shall not exceed the limits as specified below:

| % OF CLASSIFIED SE ADVANCES TO TOTAL PORTFOLIO OF SE ADVANCES | MAXIMUM LIMIT |

| a. Below 5% | 10 times of equity |

| b. Below 10% | 6 times of equity |

| c. Below 15% | 4 times of the equity |

| d. Up to and above 15% | Up to the equity |

REGULATION – 5

LIMIT ON CLEAN FACILITIES

In order to facilitate growth of smaller loans, HO/CRM will determine security requirement for loans up to Tk. 5.00 lac. Guidelines for security requirements for loans of amounts more than Tk. 5.00 lac are given in Regulation-6.

REGULATION – 6

SECURITIES

Consequent upon the regulation stated in Regulation –5 , facilities provided to SEs shall be secured by Branches as follows:

i) For loan from Tk.1.00 lac to Tk.5.00 lac.

As a minimum Branches must take charge over assets being financed.

ii) For loan from Tk.5.00 lac to Tk.50.00 lac

a) Hypothecation on the inventory, receivables, advance payments, plant & machineries.

b) Equitable/Registered mortgage over immovable properties.

c) Personal Guarantees of Spouse/Parents/other family members.

d) One third party personal guarantee.

e) Post dated cheques for each installment and one undated cheque for full loan value including full interest.

REGULATION – 7

LOAN DOCUMENTATION

For all facilities, branches must obtain (as applicable and not limiting to following) documents before disbursement of loan is made:

01) Loan Application Form duly signed by the customer.

02) Acceptance of the terms and condition of Sanction Advice.

03) Trade License.

04) In case of Partnership Firm:

a) Copy of Registered Partnership Deed duly certified as true copy or a partnership

Deed on non-judicial stamp of Tk. 150 denomination duly notarized.

05) In case of limited company:

Copy of Memorandum & Articles of Association of the company including Certificate of incorporation duly certified by Registrar Joint Stock Companies (RJSC) and attested by the Managing Director accompanied by an up-to-date list of Directors.

a) Copy of Board Resolution of the company for availing credit facilities and authorizing Managing Director/ Chairman/Director for execution of documents and operation of the accounts.

a) An Undertaking not to change the management of the company and the memorandum and articles of the company without prior permission of the Branch.

b) Copy of last audited financial statement up to last 3 years (as applicable and subject to Regulation-10)

c) Personal Guarantee of all the Directors including the Chairman and Managing Director.

d) Certificate of registration of charges over the fixed and floating of the company duly issued by RJSC.

e) Certificate of registration of amendment of charges over the fixed and floating assets of the company duly issued by RJSC in case of repeat loan or change in terms and condition of Sanction Advice regarding loan amount, securities etc.,

06) Demand Promissory Note

07) Letter of hypothecation of stocks and goods

08) Letter of hypothecation of book debts & receivables

09) Letter of hypothecation of plant & machinery

10) Charge on fixed assets.

11) Personal Letter of Guarantee

12) Wherever practical, insurance policy for 110% of the stock value covering all risks with Branch’s mortgage clause in joint name of the Branch and client.

REGULATION – 8

MARGIN REQUIREMENTS

Branches shall adhere to the minimum margin requirement as prescribed by Bangladesh Bank/ our Bank.

REGULATION – 9

CREDIT INFORMATION BUREAU (CIB) CLEARANCE

While considering proposals for any exposure, Branches should send CIB enquiry form along with related papers to obtain CIB report from Credit information Bureau (CIB) of Bangladesh Bank. The condition of obtaining CIB report will be governed by rules & regulations as prescribed by Bangladesh Bank from time to time.

REGULATION – 10

MINIMUM CONDITIONS FOR TAKING EXPOSURE

Branches shall, as a matter of rule, obtain a copy of financial statements duly audited by a practicing Chartered Accountant, relation to the business of every borrower who is limited company or where exposure of the bank exceeds Tkkk.40.00 lac, for analysis and record. However, financial statements singed by the borrower will suffice where the exposure is fully secured by liquid assets.

It is recognized that a large number of enterprises other than limited companies (i.e., sole proprietorship/partnership firms etc.) may not have proper books of accounts including Income Statement, Balance Sheet and they many not be able to prepare current and future Cash Flows due to lack of sophistication and expertise. It is expected that in such cases, Branches shall assist the borrowers in obtaining/ developing such books of accounts as per forms/formats prescribed in Appendices-VII, VIII & IX.

Each branch has to submit existing Loan Application Form as prescribed by Head Office and ‘Borrowers Basic Fact Sheet’ (refer to Appendix –II). NO proposal will be considered (including renewal, enhancement and rescheduling) until and unless the prescribed Loan Application From is accompanied by a ‘Borrower’s Basic Fact Sheet under the seal and signature of the borrower.

REGULATION – 11

PROPER UTILIZATION OF LOAN

The Branch should ensure that the loans have been properly utilized by the SEs and for the same purposes for which they were sanctioned. The branch should do proper monitoring for utilization of loans.

REGULATION –12

RESTRICTION ON FACILITIES TO RELATED PARTIES

Branches shall not take any exposure on a SE in which any of its directors, shareholders, employees or their immediate family members is holding 5% or more of the share capital of the SE.

Development guidelines

This part is a special one for the development of the Sees guidelines. The purpose of the Development Guidelines is to provide directional guidelines to the Bank who is considering introduction of Small Enterprises financing to entrepreneurs all across Bangladesh. These Guidelines will assist Bank to develop and implement pragmatic and value added products, efficient Credit Approval & Risk Management processes, sound organization structure, strong credit administration and a robust collection procedures.

It may be noted here that these are the minimum requirements and should not in any way be construed to restrict the role of the management processes through establishing comprehensive credit risk management systems.

The Process Guidelines have been organized into the following sections:

i) Product Program Guidelines

ii) Segregation of Duties

iii) Credit Approval

PROCEDURAL GUIDELINES

- Approval Process Credit Administration

- Risk Management

- Collection & Remedial Management

PREFERRED ORGANISATIONAL STRUCTURE & RESPONSIBILITIES

These guidelines have been prepared by senior executives of the Bank which will assist the Bank to create a long term sustainable and a profitable Small Enterprises business in Bangladesh.

4.2. POLICY GUIDELINES

Before embarking upon Small Enterprises financing, the bank has developed a fully documented product program guidelines. These guidelines have included objective/quantitative parameters for the eligibility of the borrowers and determining the maximum permissible limit per borrower.

These fundamental guidelines will be the key elements that would support the Banks’ credit culture and they will dictate bank’s behavior when dealing with customers and managing lending portfolio of such loans. Any deviations from these guidelines must in all cases, will require approval from competent authority.

Fundamentally, credit polices and procedures can never sufficiently capture all the complexities of the product. Therefore, the following credit principles are the ultimate reference points for all concerned Branch staff for making SE financing decisions:-

- Assess the entrepreneur’s character for integrity and willingness to repay

- Only lend when the entrepreneur has capacity and ability to repay

- Only extend credit it Branch can sufficiently understand and manage the risk

- Use common sense and past experience in conjunction with thorough evaluation and credit analysis.

- Do not base decisions solely on customer’s reputation, accepted practice, other lender’s risk assessment or the recommendations of other officers

- Be proactive in identifying, managing and communicating credit risk

- Be diligent in ensuring that credit exposures and activities comply with the requirement set out in Product Program

A generic Product Program Guidelines (PPG) has been developed for Small Enterprises Financing. Branches should take these as a reference without compromising the fundamentals of credit principles.

4.2.1 Product Program Guideline

The given product program guidelines are suggestive but not limited to this list, based on the requirements further guidelines to be incorporated in the PPG to ensure that the PPG is covering all the aspects of risk and return for the particular product.

4.2.2 PPG Guidelines (for Service Concern)

Parameters | Remarks |

| Customer Segment | Doctors, Legal Advisors, Teachers & other persons engaged in other services. |

| Purpose | For expansion and smooth running of professional activities |

| Nationality | Bangladeshi |

| Age Limit – Minimum age (years) / Maximum age (years) | 21 years to 55 years. |

| Nature of Loan | Term Loan |

| Minimum Income (Yearly) to avail minimum amount of loan | Tk.3,00,000.00 |

| Loan Size (minimum/maximum) | Tk.1.00 lac to Tk.50.00 lac |

| Security/Collateral | i) Hypothecation of goods, ii) Personal guarantee, iii) Collateral in the from of FDR/Registered Mortgage of property |

| Legal Documents | As per existing SEs guidelines |

| Interest Rate | 13.50% (subject to change by Management) |

| Maximum Term of Loan | 5 Years |

| Repayment Method | Monthly Installment |

| Disbursement Mode | Cash/Payment Order |

| Disbursement pre-condition | Formalities as per SEs guidelines |

| Debt Equity Ratio (DER%) | Maximum 70% : 30%, Minimum 50% : 50% |

| Verification of Personal Details and Quotation | As per SEs guidelines |

| Substantiation of Income | From the concerned authority/records of the parties |

| Involved Persons/Workers | Not more than 30 Persons |

| Total assets cost less land & building | From Tk.0.50 lac to Tk.30.00 lac |

Besides the above parameters, branch/RM should follow the circulars issued from time to time in respect of the subject. |

4.2.3 PPG Guidelines (for Trading & Other Concern)

Parameters | Remarks |

| Customer Segment | Persons who are involve with trading business. |

| Purpose | i. To help the genuine businessman having entrepreneurship, sincerity, honesty, to run their business smoothly. ii. To enable the poor section of people to do business with the help of Bank Finance. iii. To improve the banking habit of self employed persons of the society. iv. To contribute towards development of socio-economic condition of the country. |

| Nationality | Bangladeshi |

| Age Limit – Minimum age (years) / Maximum age (years) | 21 years to 55 years. |

| Nature of Loan | Term Loan, CC (Hypo), CC (Pledge), LC, LTR, LIM, Overdraft |

| Minimum Income (Yearly) to avail minimum amount of loan | Tk.3,00,000.00 |

| Loan Size (minimum/maximum) | Tk.1.00 lac to Tk.50.00 lac |

| Security/Collateral | i) Hypothecation of goods, ii) Personal guarantee, iii) Collateral in the from of FDR/Registered Mortgage of property |

| Legal Documents | As per existing SEs guidelines |

| Interest Rate | 13.50% (Term Loan) & 13.00% for others (subject to change by Management) |

| Maximum Term of Loan | 1 Month to 5 Years depending on the nature of facilities |

| Repayment Method | Monthly Installment/in lump sum from time to time |

| Disbursement Mode | Cash/Payment Order |

| Disbursement pre-condition | Formalities as per SEs guidelines |

| Debt Equity Ratio (DER%) | Maximum 70% : 30%, Minimum 50% : 50% |

| Verification of Personal Details and Quotation | As per SEs guidelines |

| Substantiation of Income | From the concerned authority/records of the parties |

| Involved Persons/Workers | Not more than 20 Persons |

| Total assets cost less land & building | From Tk.0.50 lac to Tk.50.00 lac |

Besides the above parameters, branch/RM should follow the circulars issued from time to time in respect of the subject. |

4.2.4 PPG Guidelines (for Manufacturing Concern)

Parameters | Remarks |

| Customer Segment | Persons who are involved in manufacturing products & selling thereof |

| Purpose | i. To help the genuine businessman having entrepreneurship, sincerity, honesty, to run their business smoothly. ii. To enable the poor section of people to do business with the help of Bank Finance. iii. To improve the banking habit of self employed persons of the society. iv. To contribute towards development of socio-economic condition of the country. |

| Nationality | Bangladeshi |

| Age Limit – Minimum age (years) / Maximum age (years) | 21 years to 55 years. |

| Nature of Loan | Term Loan, CC (Hypo), CC (Pledge), LC, LTR, LIM, Overdraft |

| Minimum Income (Yearly) to avail minimum amount of loan | Tk.3,00,000.00 |

| Loan Size (minimum/maximum) | Tk.1.00 lac to Tk.50.00 lac |

| Security/Collateral | i) Hypothecation of goods, ii) Personal guarantee, iii) Collateral in the from of FDR/Registered Mortgage of property |

| Legal Documents | As per existing SEs guidelines |

| Interest Rate | 13.50% (Term Loan) & 13.00% for others (subject to change by Management) |

| Maximum Term of Loan | 1 Month to 5 Years depending on the nature of facilities |

| Repayment Method | Monthly Installment/lump sum from time to time |

| Disbursement Mode | Cash/Payment Order |

| Disbursement pre-condition | Formalities as per SEs guidelines |

| Debt Equity Ratio (DER%) | Maximum 70% : 30%, Minimum 50% : 50% |

| Verification of Personal Details and Quotation | As per SEs guidelines |

| Substantiation of Income | From the concerned authority/records of the parties concerned |

| Involved Persons/Workers | Not more than 60 Persons |

| Total assets cost less land & building | From Tk.0.50 lac to Tk.50.00 lac |

Besides the above parameters, branch/RM should follow the circulars issued from time to time in respect of the subject. |

4.2.5 SEGREGATION OF DUTIES

Adequate segregation of duties is a prerequisite of an effective system of internal control. To be adequate, segregation must ensure that the following functions are performed by persons independent of each other, although, within limits, certain duties may be combined so long there is adequate supervision:-

Processing loan proposal – by Branch

Credit approval – by Head Office

Documentation – by Branch

Sales and marketing – by Branch

Credit recover – Primarily by the Branch under the supervision of ZO/HO.

The credit approval team will evaluate and approve the loan. The BM will check and ensure the documentation and disburse the loans. This will ensure better control of the Branch asset and mitigate the risk of compromise of the duties.

4.2.6 CREDIT APPROVAL

Proposals received at ZO, Credit Risk Management (CRM), Head Office from Branches should include the following papers (where necessary):-

a) Existing loan Proposal Form (Credit Memorandum).

b) Borrowers Basic Fact Sheet (Appendix-II)

c) Contract Point Verification Report (Appendix-III)

d) Comments on the Enterprise and Entrepreneur (Appendix-IV)

e) Borrower Credit Rating (Appendix-V)

f) Work Sheet for Working Capital Requirement (Appendix-VI)

g) Income Statement (Appendix-VII)

h) Balance Sheet (Appendix-VIII)

i) Cash Flow Statement (Appendix-IX)

j) Financial Ratios (Appendix-X)

k) Checklists etc. (Appendix-XX)

Applications will be evaluated/assessed by Credit Analyst/Departmental Officials/Executives of SE Financing on the basis of different particulars as mentioned above. The evaluation process is carried out based on the agreed and standard guidelines for different loans product and the documents checklist as per the PPG. The detailed credit and risk assessment should be conducted prior to the approval of any loan.

The branch officials are held responsible to ensure the accuracy of the loan application submitted for approval. They must be familiar with the Bank’s lending Guidelines and should conduct due diligence on new borrowers, purpose of the loans and guarantors.

All Branches should have established Know Your Customer (KYC) and Money Laundering guidelines, which should be adhered to at all times.

Credit Applications should have include, as a minimum, the following details:

- Amount and type of loan(s) proposed.

- Purpose of loans.

- Loan Structure (Tenor, Covenants, Repayment Schedule, Interest)

- Security

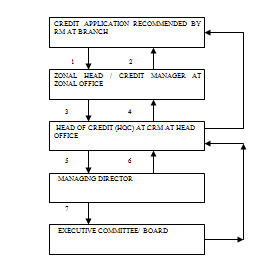

Branch should follow the sample process work flow chart in (Appendix I).

4.3. PROCEDURAL GUIDELINES

This section outlines the main procedures the are required to ensure compliance with the policies contained in Section 1.0 of these guidelines.

4.3.1. APPROVAL PROCESS

The Relationship Manager will assess the particulars/information of the application and will sanction loans/advances if within the delegated power of Relationship Manger (RM). But if it is not within the delegated power, Relationship Manger (RM) will recommend the limit for approval to Zonal Head, Who will sanction loan/advance as per delegation given to him and for loans and advances beyond his discretionary power should be sent to CRM at Head Office, (Credit Division). The responsibility for preparing the credit proposals should rest with the Relationship Manager (RM).

The recommending or approving executives should take responsibility for and be held accountable for their recommendations or approval. Delegation for approval of limits should be in accordance with revised business delegation powers circulated by Head Office from time to time.

The approval process is illustrated below:-

1. Proposal is to be forwarded by Relationship Manager to Zonal Office for approval

/ decision.

- Decision is to be conveyed as per delegated authority (approval / decline) to recommending branches by Zonal Office. A monthly summary of Credit Proposals approved by ZO should be sent to HOC. The HOC should review 10% of ZO approvals to ensure adherence to Lending Guidelines and bank’s policies.

- Zonal Head (ZH) forwards proposals to Head of Credit (HOC) CRM for approval of the proposals which are beyond his Delegation of powers.

- HOC advises the decision as per delegated authority to Relationship Manager/Branch Manager, with a copy to Zonal Office.

- HOC forwards proposal which is not within his delegated power with due recommendation to Managing Director for approval/decision.

- Managing Director presents the proposal to EC/Board as the case may be.

- EC/Board gives the decision to HOC.

DUPLICATION CHECK:

All approved applications must be checked against Branch’s database to identify whether the applicant is enjoying any other loan in other account apart from the declared loans.

MAINTENANCE OF NEGATIVE FILES

Two negative files – one listing the individuals and the other listing the employers – are to be maintained to ensure that individual with bad history and dubious integrity and employers with high delinquency rate do not get loan from Branches.

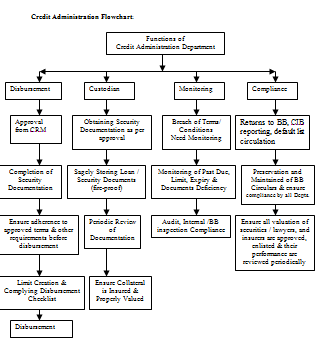

4.3.2 CREDIT ADMINISTRATION

The function of Credit Administration is a complicated job. Prior to disbursement of loan facilities to a borrower it is necessary to ensure that proper documentation and approvals are in place for record and for subsequent reference. For this reason, it is essential that the functions of credit Administration be strictly segregated from Relationship Management/Marketing in order to avoid the possibility of controls being compromised.

Credit Administration procedures should be to ensure the following as shown in this chart.

CREDIT DOCUMENTATION

Security documents are prepared in accordance with approved terms and are legally enforceable. Standard forms of documentation that has been reviewed by lawyers should be used in all cases. Exceptions should be referred to panel lawyer for advice.

BM/RM is responsible:

- To ensure that all security documentation complies with the terms of approval.

- To control loan disbursements only after all terms and conditions of approval have been met, and all security documentation as per the checklist of approved PPG is in place.

- To maintain control over all security documentation.

- To monitor borrower’s compliance with agreed terms and conditions, and general monitoring of account conduct/performance.

DISBURSEMENT

Branch will disburse the loan amounts under the approved loan facilities when all security documents are in place.

CUSTODIAL DUTIES

Loan disbursements and the preparation and storage of security documents should be done at the branch under supervision of the zonal office / Credit Risk Management. ZO, if required will send copies of the documents as directed by the Credit Monitoring Cell working within CRM at Head Office, Credit Division.

Appropriate insurance coverage is maintained ( and renewed on a timely basis ) on assets mortgaged as collateral or undertaking from the borrower should be taken as per circular in force in lieu of insurance policy.

Security documentation is held under strict control, for safety purpose that is to protect from untoward incidences preferably in a locked fireproof storage.

COMPLIANCE REQUIREMENTS

All returns required for submission to Bangladesh Bank to be prepared in prescribed format correctly and timely. And these are to be submitted to the concerned department of Bangladesh Bank.

Circulars / rules and regulations issued from Bangladesh Bank and instructions from HO shall be maintained at the Branches, Zonal Offices and at H.O CRM desk. The instruction of the circular shall be complied with by all relevant officers/ executives at all levels.

4.3.3. RISK MANAGEMENT

CREDIT RISK

The credit risk is managed by the BM/ZH, which is completely segregated from business/sales. The following elements contribute to the management of credit risks.

In order to manage the Credit Risk associated with the products, the following areas are to be meticulously examined:-

- Loans will be given only after proper verification of customer’s static data and after proper assessment & confirmation of income related documents, which will objectively ascertain customer’s repayment capacity.

- Proposals will be assessed by BM/ZH who are completely separated from business/sales.

- Every loan will be secured by hypothecation over the asset financed, and customer’s authority taken for re-possession of the asset in case of loan loss.

- The loan approval systems is encouraged to be parameter driven as much as possible which will substantially eliminate the subjective part of the assessment procedure.

There will be responsible officer at the branch who will ensure timely monitoring of loan repayment and its follow up.

CONTACT POINT VERIFICATION

Contact Point verification should be done wherever possible for all applicants. The external CPV includes residence, office and telephone verifications (format of CPV report attached in Annexure III). All verifications are done to seek /verify/confirm the declared/undeclared information of the applicant.

THIRD PARTY RISK

In case of third party deposits/security instruments, Branches should verify third party’s signature against the specimen attached to the original instrument and Branch will also send the instrument to the issuing office for their verification and written confirmation on lien marking and encashment of the instrument. Therefore, any inherent risk emanating from accepting third party deposits / security instruments is minimal.

FRAUD RISK

There is an inherent fraud risk in any lending business. The most common fraud risks are:

APPLICATION FRAUD

The applicant’s signature may not be verified for authenticity. However, the applicant’s identity should be confirmed by way of scrutiny of identification and other documentation. RM should be in place to verify applicant’s residence, office and contact phone numbers etc.

There always remains the possibility of application fraud by way of producing forged documents. Considering the current market practices and operational constraints, it may not always be feasible to validate the authenticity of all documentation. However, Branches should be aware of this threat and may consider validating the Branch statement ( the most important and commonly provided income document) through RM.

LIQUIDITY AND FUNDING RISK

This risk would be managed and the position monitored by the Asset Liability Committee headed by the Managing Director.

POLITICAL AND ECONOMIC RISK

Political and economical environment of a country play a big role behind the success of business. Branches should always keep a close watch in these areas so that it is able to position itself in the backdrop of any changes in country’s political and economical scenario.

OPERATIONAL RISK

For SE loans, the activities of front line sales and behind-the-scene maintenance and support are clearly segregated.

BM/RM will manage the following aspects of the product: a) inputs, approvals, customer file maintenance, monitoring & collections; b) the Operation jobs like disbursal in the system including raising debit standing orders and the lodgment and maintenance of securities.

It will ensure uncompromising checks, quick service delivery, uncompromising management of credit risks and effective collections & recovery activities.

MAINTENANCE OF DOCUMENTS & SECURITIES

The applications and other documents related to SE loans will be held in safe custody by RM or Operations Unit. All this documents will go under single credit file per customer developed before launch of the product.

The physical securities and the security documents will be held elsewhere inside fire-proof cabinets under RM’s or Operation’s custody. The dual-key system for security placement and retrieval will have to be implemented.

INTERNAL AUDIT

All big/A.D. Branches should have a segregated internal audit department who will be responsible with performing audits of all departments. Audits should be carried out on regularly or periodically as agreed by the Management to assess various risks and possible weaknesses and to ensure compliance with regulatory guidelines, internal procedures, Lending Guidelines by ZO/HO.

4.3.4 COLLECTION & REMEDIAL MANAGEMENT

MONITORING

Supervision, follow-up and monitoring of loans are very vital and important to ensure proper use and recovery of loans. The bank can not thrive if its loans and advances are not timely repaid and recovered for further rolling to generate economic activities and earn income. Recovery of loan is also an important source of the bank for its very existence and survival. The band cannot be sure of repayment of loans unless it has an effective system of supervision, follow-up and monitoring. The sanction of a loan for project investment activity is only a flittering moment between the preparatory work and its implementation, keeping in mind the objectives of the financing unit/activity/purpose. The purpose of any input/injection of money to a business is to increase output, increase employment, increase value of Products, increase the standard of living of the borrower/ lender and others involved in the activities for which loan is sanctioned. It is also for the purpose to enable sustaining the investment process upon a long period of time.

RECOVERY

The Loan Recovery Unit established in the branch and at zonal office will ascertain the states of the Loans and Advances as Sub-Standard, Doubtful and Bad & Loss as the case may be as per guidelines of Bangladesh Bank when the outstanding in the account is not being operated as per norms, the RM is to take steps to regularize the same and when it is observed that the limit expired but not renewed it becomes overdue. The authority should take steps and at this stage normal steps like physical contact with the borrower and through letters be requested to take steps for adjustment and renewal . If the borrower fails to do so within a specified period final notice/legal notice may be served. Even then if no tangible result emanates from the process legal action is to be initiated in consultation with the panel lawyer in accordance with the existing laws of the country after obtaining permission from competent authority. Recovery process also refers to amicable settlement even after taking legal action out side the court. Branch will act as per guidelines of revised Artharin Adalat 2003. In sending proposal for legal action amicable settlement the relevant particulars of the account along-with security aspects and status of classification should be submitted. In case of amicable settlement acceptable repayment arrangement along with sources thereof should be clearly furnished.

COLLECTION OBJECTIVES

The collector’s responsibility will commence from the time an account becomes delinquent until it is regularized by means of payment or closed with full payment amount collected.

The goal of the collection process is to obtain payments promptly while minimizing collection expense and write-off costs as well as maintaining the customer’s goodwill by a high standard of service. For this reason it is important that the collector should endeavor to resolve the account at the first time worked.

Collection also protects the assets of the bank. This can be achieved by identifying early signals of delinquency and thus minimizing losses.

The customers who do not respond to collection efforts – represent a financial risk to the institution. The Collector’s role is to collect so that the institution can keep the loan on its books and does not have to write-off / charge off.

IDENTIFICATION AND ALLOCATION OF ACCOUNTS

When a customer fails to pay the minimum amount due or installment by the payment due date, the account is considered in arrears or delinquent. When accounts are delinquent, collection procedures are instituted to regularize the accounts without losing the customer’s goodwill whilst ensuring that the Branch’s interests are protected.

COLLECTION / MONITORING STEPS

To identify and manage arrears, the following aging classification is adopted:

| Days Past Due (DPD) | Collection Action |

| 1-14 | Letter, Follow up & Persuasion over phone (Appendix-XI) |

| 15-29 | 1st Reminder letter & Sl. No. 1 follows |

| 30-44 | 2nd reminder letter +Single visit |

| 45-59 |

|

| 60-89 | With the permission of Head Office:-

|

| 90 and above |

|

As and when an account become delinquent, collection system works together to achieve business objectives. At the beginning of the month collection unit has taken the total asset portfolio from the system. Then all X to 149 DPD account has to identify and allocate those accounts to the individual collectors to collect the over dues on a set target basis. The respective collector has got one month time to recover the overdue on a target based matrix. During the month, officer collection will generate the fresh arrival to X DPD accounts once in a week and hand over those to the collectors of front end to minimize the delinquency as well as the flow rate.

Delinquent Accounts Identification & Classification

The delinquent accounts can be classified as three categories as follows:

- 1. Front-End

- 2. Mid-Range

- 3. Hard-Core

|

Front-end is the first collection bucket in which delinquent accounts are identified and at this stage, the customers are normally contacted by phone and letter, which serves as a reminder of his/her obligation to pay the overdue amount to the Branch.

Any account, which is past due by one day from his payment date, will be assigned to respective collectors at the beginning of the month and given one month time to recover the dues. Telephone call should be conducted in a soft and tactful manner in consistency with the customer service level. Collector must always do an inquiry through the system to

confirm if payment has been received before commencing with telephone calling to avoid causing misunderstanding with the customer.

Initial telephone contact should be directed at the office. If the customer cannot be contacted, telephone call should then be made to the residence telephone number. Upon successful contact with a customer, the collector will tactfully inquire about the reason for not paying the minimum payment due. The collector will then proceed to obtain a promise to pay for the overdue installment along with the penal interest.

If collection letter or statement returned from the customer due to change of address, it is the responsibility of the respective collectors to collect the new address and telephone number and on some extent they could use the external agency for update the same. The collectors should ask the customer to provide written instruction of address change to the customer services department and at the same time record the new address and telephone no into the Branches system.

Selective letters can be issued to customers who are difficult to contact through telephone.

|

Mid-range is the bucket in which the account is considered to be seriously delinquent thus collection efforts must be more intensive, as the account has threatened our asset. When the front-end delinquent collection effort fails to obtain installment, the account will automatically age into the 30 DPD and subsequently 60 DPD delinquent category.

These are accounts, which flow down from Front-end. Collectors must exercise a more aggressive approach at this stage as the customer has failed to submit a payment even after Front-end efforts. Collection letters also send to the customers reminding the customers to pay the overdue within due date.

The Collector must review and analyze the reason(s) for delay in payment. Upon successful contact with the customer, the collector must secure a payment date. Constant telephone calls should be made to those customers who have given numerous broken promises.

Seeking assistance letter to the guarantor or on some extent to the employer may be an effective instrument at this stage.

|

90+DPD accounts are considered hard-core delinquency and collection efforts are to be more intensified than 30 DPD and DPD accounts. Interest to be suspended at this stage of delinquency (90 DPD).

Extra telephone calls and letters are mandatory. Final reminder letter & Guarantee call up letter must be sent to the customers and guarantors informing the consequences and demanding the payments. Intensive visits are also conducted on accounts for immediate settlements. Requests for waiver are entertained in case of settlement at one go payment. Reschedulment can also be offered in some cases as an exception.

When recovery opportunities are considered good through legal notice, collectors should make recommendations for legal notices if necessary but not as mandatory.

|

The account in 150+DPD is provided, monitored and tracked separately other than the above delinquent accounts. A recovery management team is dedicated for dealing those accounts till settlement. Facility call up letter must be served to the customer and demanding the total outstanding is the first initiative for this stage. Then legal notice and other legal consequence will be the next course of action for the recovery. External agencies and legal agency are involved at this stage. Tremendous pressure will be given to the customer as well as to the guarantor for the settlement through using internal collectors as well as external recovery agencies.

PRODUCTIVETY TRACKING:

For productivity tracking, analysis from the collectors call sheet is required. the variables for productivity tracking are, number of calls made per day, valid contact, promise to pay, kept promise, broken promise etc needs to be analyzed.

A process should be established to share the lessons learned from the experience of credit losses in order to update the lending guidelines.

AGENCY MANAGEMENT:

All provided accounts must be placed into a dedicated recovery management team. The recovery portfolio has sub divided into various collectible and non-collectible pools of accounts. Depending upon the size of the account balance, internal recovery efforts may continue while rest of the portfolio that would be assigned to external agencies including legal agencies to ensure expected recovery.

Officer collections (recovery) would be empowered to offer interest waivers for one-time settlement, and installment plans (not re-writes) and amnesty offers to maximize recovery collections. The collections unit/branch would able to produce information of accounts to facilitate the above type of collection efforts. Incentive plans should exist for internal as well as external collections.

On every month the responsible officer/ collection unit will ensure the allocation of the provided accounts to the individual collectors as well as to the external agencies depending of the prospect of recovery to maximize the recovery.

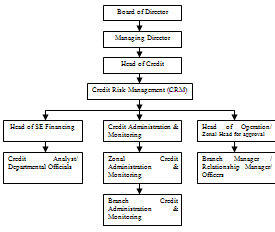

4.4 PREFERRED ORGANIZATIONAL STRUCTURE & RESPONSIBILITIES

PREFERRED ORGANIZATIONAL STRUCTURE

The following chart represents the preferred management structure:

Where,

- Loan processing function are segregated from approval function

- All application must be approved by the Head of Credit or Zonal Head.

- Branch will process and disburse all loans.

- Table of Appendix

- Findings Recommendations

- Difficulties, Problems that found by Uttara Bank Ltd

- Recommendations

- Accounting Entries

- Conclusion

- Elaboration

- Questionnaire

Findings & Recommendations

Uttara Bank Ltd Limited has been performing very well. The UBL is running with steady growth in almost every sphere. They are reducing nonperforming loan. They are one of the leading Bank in Bangladesh with in current years. No doubt this is the sign of good management. Though the appraisal and proposal system of the Uttara Bank Ltd is said to the best one in this kind certain factors are overlooked. Although there are shortage information we found some strength, weakness, opportunity and threats to Uttara Bank Ltd.

- In appraisal system the competitive position analysis is not focused while doing the appraisal system.

- The product appraisal is done on the customer base not any comparison is done with other product.

- The suppliers’ influence is overlooked.

- Due to the data unavailability the credit demand assessment is not properly done.

Strength:

- Stable source of fund.

- Strong Liquidity position.

- Wide network of branches.

- Experienced top management.

- Diversified product line.

- Satisfactory IT infrastructure

Weakness:

- Shortfall in capital adequacy.

- Problem in asset quality management.

- Asset infection rate is still high.

- Relatively high overhead expense.

- A segment of manpower of manpower is less skilled.

- Each branch is burdened with some non performer.

Opportunities:

- Regulatory environment favoring.

- Private sector development.

- Credit card business.

- SME and Agro based industry loan

Threats:

- Deposits as well as quality assets.

- Market pressure for lowering the interest rate.

- Shrinkage in export, import and guarantee.

- Business due to economic slump.

- Recruitment in the name of employees wardship quota in recent days is made without any competitive evaluation test will create burden instead of asset in future.

Difficulties, problems that are faced by Uttara Bank Ltd .

In present situation, there are several competitions in Bangladesh specially in Banking sector among four National Commercial banks( NCB), Twelve foreign and multinational Banks and thirty private Commercial Banks. Moreover there are twenty-five non banking financial institutions named SABINCO, IDLC, DBH etc are also acting and serving as commercial Banks.

So with in a small market main problems arises are following:

- Uneven Market competition.

- Ill and malpractice of other banks to attract clients.

- Weak market communication problem.

- Less effort to educate and upgrade the bankers.

- Poor customer service.

- Sales peoples are ignored in Bangladesh.

- Some times the interest rate is higher.

- Uttara Bank Ltd strictly follows the rules of the Central Bank.

- Savings/Deposit interest rates are not competitive.

RECOMMENDATIONS

Based on the evaluation of different aspects of the lending process of Uttara Bank Ltd the following recommendations have been made:

- In the face of competitive and borrower dominated credit scenario TheUttara Bank ltd must come up with innovative loan products to meet up the demand of time. In this connection Uttara Bank ltd can focus on some more loan products like:

v Leasing.

v Syndicate Banking.

v Merchant Banking/ Investment Banking.

v Apartment loan.

v House building/ Apartment project.

v Marriage loan.

v Education loan.

v On Line Banking.

v Car Loan.

v Credit card.

- To combat the problem of mobilizing deposit in the form of credit, Uttara Bank ltd should focus on intensive marketing effort.

- The deposit position of Uttara Bank ltd is quite satisfactory but keeping in mind the future need The Bank should go for extensive deposit hunting along with advance. The deposit rate should be fixed in a position that keep pace with the demand of the competitive market.

- Entrepreneurship lending should be given due emphasis.

- The Bank should go for syndicate Banking to avoid big loan, lending risk.

- The Bank should recalculate its lending rate on a periodic basis to cope up with changing lending scenario.

- As borrower selection is the key to successful lending, Uttara Bank Ltd should focus on the selection of true borrower. But at the same time it must be taken into account that right borrower selection does not mean that Uttara Bank Ltd has to adopt conservative lending policy but rather it means that compliance with the KYC or Know Your Customer to ascertain the true purpose of the loan.

- Care should also be taken so that good borrowers are not discarded due to strict adherence to the lending policy.

- At the branch level credit department must be adequately capable of collecting the correct and relevant information and analyzing the financial statements quickly and precisely.

- Credit officer must be skilled enough to understand the manipulated and distorted financial statements.

- Credit committees at all levels must work in co-ordination with each other for quick approval of loans and to reduce the loan processing cost.

- To expedite the lending process, board credit committee meeting should be held twice or more a month.

- To faster the lending process, Uttara Bank Ltd should facilitate online loan application submission and personal credit processing.

- In case of mortgage, care must be taken to accept collateral on second charge.

- In case of assignment the bank must ensure that undertaking has been given by the assignment debtor.

- Monitoring of a loan should be conducted at regular interval.

- Reporting of all loans should be periodically made to Bangladesh Bank

- Loan monitoring is a continuous task and requires expert manpower. Therefore it is suggested that Uttara Bank Ltd should set up a separate loan monitoring cell which will be responsible for monitoring its total loan portfolio with special care to the problem loan. Each branch should have at least one loan monitoring officer who is only meant for loan monitoring of the Branch and directly liable to the monitoring cell under control of the manager.

- Our sales people should be trained up properly so that customer gets interested to talk with them.