1.1 Incidental of authorization & submittal

To explore & confront the reality, preparation of report with versatile knowledge from corporate world or organization under a specific direction or a topic is mandatory for our BBA requirement. The application of the knowledge in the practical field of & realization of the real working environment under a proper guidance is the primary purpose of this internship program. The process of preparing the report is to justify & to have a better view of the real life competitive organization environment. The crucial aspects & basic analysis of factors that affect portfolio construction have been given most priority in this report. In course of the preparation of this report, we have applied our knowledge, personal quality & justification. The report is an imperative step for us to have a sound knowledge about capital market of Bangladesh.

Portfolio formulation is the investment strategy that mixes variety of assets in order to minimize the adverse effect that one security will have on the overall performance of the portfolio. By increasing the number of assets in a portfolio, the risk will be spread-away across of the assets, thus minimizing the chance of capital loss. Varies in assets combination from different securities or industries will increase the chances of having as weak or negative assets correlation in the portfolio. This is to ensure, each of the securities complement each other to offset the large losses.

1.2 Background of the Study

Everybody earns and spends money. But to optimize this earning & spending and to accommodate the future uncertainties, inflation etc., there needs to be proper planning & management of wealth. Investment decision is one of major part of this management of wealth. Because, sometimes may have enough money in hand and sometimes not. If excess money is invested in a proper manner, then it can encounter the problem during deficit. Portfolio management is an important management process of wealth, which maximizes the return for desirable risk level. In portfolio management, emphasis is given on the investment in the capital market. For this reason, study on security market is so essential. Evaluating efficient portfolio that maximize the return & minimize the risk compare to other portfolio is very much important.

1.3 Objectives of the Study

The core objective of the study is to find out the reasons that affect portfolio formulation of different securities. However the objectives of the study can be described under the following head:

1.3.1 Broad Objective: The broad objective of the study is to find out the factors affecting portfolio formulation in the capital market.

Specific Objectives: With a view to fulfilling the broad objective some specific objectives have to be satisfied. The specific objectives of this study are as follows:

- To determine the affect of price on portfolio formulation

- To investigate the optimum number of stocks that can minimize the portfolio risk.

- To find out the volume of different securities which affecting portfolio formulation

- To find out relation of price earnings ratio with portfolio formulation

- To find out the affect of earning per share on portfolio formulation

- To find out the reasons behind portfolio formulation of different securities.

- To find out the impact of the economic condition during portfolio formulation

1.4 Scope of the Study

To achieve the objective it is needed to collect data from different investors. For achieving the objectives, the study will be focused on the price, volume, P/E, EPS, economic conditions, interest rate and other criteria of different companies. While doing so it identified the limitations and the weaknesses of the issue. All the analysis based on and primary data & secondary data derived from different investors. In case of samples, data is from the different investors and consultancy firm, though the research population was all the investors in Dhaka Stock Exchange Ltd. Therefore, it done with a good confident that the chosen sample is truly representative of the entire population.

1.5 Methodology

To attain the objective, we collected data & information required. Those data & information were collected from various sources & then analyzed.

Collection of data & information:

Primary data & information:

ü Observation & collection of data from different investors by asking them related question

ü Conversation with the executives & officers of Dhaka stock exchange Ltd.

ü Collection of Annual Report of DSE from the it’s library

Secondary data & information:

- Annual Report of listed companies

- Monthly review of Dhaka Stock Exchange Ltd

- Several kind of academic Test-Book.

- Different publications regarding stock exchange function

- Price index

1.6 Limitation of the study

While going through the internship program, it should be noted that the period was very pleasant because of cooperation & trustfully access had been given into too many databases, & for better learning purpose the authorization was also given to so many computerized data bases for updating. But as it was an internship program designed by the department of finance of BBA course under National University, Bangladesh. After all, some limitations that I have faced want to mention from report preparation point of view.

ü Shortcoming of practical experience to comprehend the conceptual framework of this type of report.

ü During the primary data collection period, it was seen that investors and the management of the investment companies were very much reluctant to talk to outsiders of the organization. Their excuse was the restriction of organizational rules. If it would not happen more data could be collected.

ü Sometimes it was possible to contract with a few number of respective management staffs for the research work .It would be resourceful for the report if more interviews could be taken.

ü The experts of our country, who could have put their valuable views on the report, were highly committed and therefore were unavailable for interview.

2.1 Literature Review

In the past decades, many researchers attempted to use different methods in order to predict decision regarding share markets. Here described some previous research works related to analysis sectors and tried to find out the limitations to improve the analysis process better then before.

Markowitz (1952) has developed a basic and most accepted model for portfolio selection, by introducing the usage of expected rate of return and expected risk for a portfolio. He has identified the risk-reduction benefits associated with holding a diversified portfolio of assets. Subsequently, a number of authors have attempted to measure the rate at which risk-reduction benefits are realized as the numbers of securities in a portfolio are expended.

Sharpe (1964) described the advantages of using a particular model of the relationship among the securities for practical applications of the Markowitz portfolio analysis techniques. A computer program has been developed to take full advantage of the model.

Evens and Archer (1968), who modeled risk in term of a portfolio’s standard deviation and concluded that randomly selected and equally weighted portfolio provides a little risk-reduction to be obtained from expanding a portfolio beyond ten of fifteen securities. So from this observation revealed that risk reduction affect diminishes rapidly as the number of stock increases.

Professor Statman, demonstrated that the optimal diversification of portfolios depended upon: 1) the risk premium (the expected excess return of equities over the risk free rate of return), 2) the covariance (the average correlation of price movements between stocks), and 3) the costs or fees associated with portfolio management.

Professor Statman concluded that, if individuals are going to hold individual common stocks in their investment portfolios, they should hold more than 120 different randomly selected stocks. This number would allow them to avoid holding a suboptimal portfolio that had higher risk and lower cost-adjusted expected returns relative to a market index fund.

William Bernstein is an investment advisor and the author of Efficient Frontier: an Online Journal of Practical Asset Allocation. His study, “The 15-Stock Diversification Myth,” points out that holding a limited number of stocks does not provide foolproof diversification. Mr. Bernstein formed 98 randomly selected 15-stock portfolios from S&P 500 firms that remained in that index throughout the ten-year period from 12/89 to 11/99. He calculated returns on a buy-and-hold strategy over these ten years.

The annualized 10-year return for the S&P 500 on an equally weighted (not capitalization-weighted) basis was just over 24%. Mr. Bernstein’s graph of the variation in returns of these 98 random 15-stock portfolios showed a very distinctive downward skew. Three out of four of his 15-stock portfolios underperformed the index. The reason is that only a relatively few stocks in the overall index were stellar performers over the long haul. Since there were relatively few huge gainers, the odds of including any one of them in a 15 stock portfolio selected from 500 possible stocks were not high. Mr. Bernstein calculated that the odds of picking one of the top 10 stocks for a 15-stock portfolio were only about one in six.

In “How Many Mutual Funds Constitute a Diversified Mutual Fund Portfolio?,” Professor O’Neal (1997), used Morningstar data for all U.S. “growth” style and “growth and income” style mutual funds that were in operation throughout the 1976 to 1994 period. For the full 19-year period, respectively, there were 103 and 65 of these mutual funds. He estimated the cumulative returns and volatility of investment portfolios that were composed of between one and thirty randomly selected mutual funds over various periods ranging from five to nineteen years. This study demonstrates that the failure to diversify among actively-managed mutual funds can expose you to huge variations in outcomes. Nevertheless, choosing one or many actively-managed mutual funds is just a crap shoot. When you spread you investment assess among many of them, at least you can achieve some diversification benefits, but at an unnecessarily high price.

One attempt at estimating such relationship for use in simulating monetary effects within a macroeconomic model is described in the research of Robert H. Rasche and Harold T. Shapiro (1968). A fuller discussion of this common stock valuation formula can be found in Burton G. Malkeil (1963), Martin Feldstein (1980) discussed a crucial cause of the failure of share prices to rise during a decade of substantial inflation. The analysis here indicates that this inverse relation between higher inflation and lower share prices during the past decade was not due to chance or to other unrelated economic events. One of the analyses by Franco Modigliani and Richard Cohn (1979) also shows that it is unnecessary to invoke a theory of systematic error of the type.

According to Kenneth E. Homa & Dwight M. Jaffee (1971), while forecasting share prices, further realism could be introduced. in particular, short sales of stock, the tax treatment of short term and long term capital gains, bills perhaps other assets, all could be introduced into the simulation. Finally, more practical use might be made of timing implications of the model if forecasts were generated on a monthly or weekly basis.

According to Martin Feldstein (1980), full understanding of the equilibrium relation between share prices and inflation requires extending the current analysis in a number of ways. A more explicit portfolio model could derive asset demand equations from expected utility maximization and could recognize that some institutional holdings are really indirect ways for individuals to hold assets in a tax-favored way. Martin Feldstein (1980) also concluded his study saying that the simplification that the capital stock remains constant should be replaced by a more dynamic model that recognizes the effect of inflation on capital accumulation.

According to the Executive Director of CPD (centre for policy Dialogue) Dr.Debapriya Bhattacharya’s (2006) research, during the first ten months of FY06 the Dhaka Stock Exchange (DSE) observed a decrease in all of its share price indices. All Share Price Index (DSI) declined by (-) 340 points from 1486.34 in March 2005 to 1146.33 on March 2006. The General IndexAB also declined by -427.5 points from 1919.3 to 1491.8 during the same period. Surprisingly, the major shock originated from the performance of the top ranked companies–the DSE20 index lost 605.0 points, declining from 2030.3 to 1425.3 during the period under consideration.

It seems that the present liquidity crisis in the money market is one of the key reasons for the continuing decline in share prices and indices. Under the current liquidity crisis in the banking sector, high deposit rate offered by banks and financial institutions may have encouraged small savers to deposit their money in banks instead of investing in capital market (Dr. Debapriya Bhattacharya, (2006)). From this report we got an idea that there may be a relationship between share prices and current call money rates.

Here to review on those papers/articles which have done analysis to check whether stock prices and oil price are related to each other or not. John Mauldin (2003) reported in an article of Swiss America Trading Corporation on the relationship between oil prices and stock prices that, he found strong evidence that changes in oil prices forecast stock returns. This predictability is especially strong in the developed countries markets. Among his (John Mauldin (2003) chosen 12 of the 18 countries, changes in oil prices significantly predict future market returns on a lagging monthly basis. Not surprisingly, a rise on oil price suggests a lower stock market and a drop in oil price infers a rise in stock prices. The magnitude of the oil price shift is also carried over into the magnitude of the expected increase/decrease in stock prices.

John Mauldin (2003) used such a method, while adding alpha or excess returns over buy and hold, is still volatile as heck (that’s a technical term) and is wrong over 40% of the time in most countries. It is just that when it is right, the returns are excessive. This also means that there could be certain random entry/trend following variables. Though the study clearly showed that oil prices and stocks, especially if there are big moves in oil, tend to go in opposite directions. Here we saw that though John Mauldin (6) found a relationship between share price and oil price, but it is wrong over 40% of the time in most countries. So we have tried to find this relation using different method to see whether the significance level could be high.

The issue of whether stock prices and exchange rates are related or not have received considerable attention after the East Asian crises. During the crises the countries affected saw turmoil in both currency and stock markets. If stock prices and exchange rates are related and the causation runs from exchange rates to stock prices then crises in the stock markets can be prevented by controlling the exchange rates. Moreover, developing countries can exploit such a link to attract/stimulate foreign portfolio investment in their own countries. Similarly, if the causation runs from stock prices to exchange rates then authorities can focus on domestic economic policies to stabilize the stock market. If the two markets/prices are related then investors can use this information to predict the behavior of one market using the information on other market.

This article of R. Smyth and M. Nandha (2003) examines the relationship between exchange rates and stock prices in Bangladesh, India, Pakistan and Sri Lanka using daily data over a six-year period from 1995 to 2001. Both the Engle-Granger two-step and Johansen co-integration methods suggest that there is no long-run equilibrium relationship between these two financial variables in any of the four countries. Granger causality tests find that there is unit-directional causality running from exchange rates to stock prices in India and Sri Lanka, but in Bangladesh and Pakistan exchange rates and stock prices are independent.

Most of the empirical literature that has examined the stock prices-exchange rate

relationship has focused on examining this relationship for the developed Countries with very little attention on the developing countries. The results of these studies are, however, inconclusive. Some studies have found a significant positive relationship between stock prices and exchange rates (for instance Smith (1992), Solnik (1987), and Aggarwal (1981)) while others have reported a significant negative relationship between the two (e.g., Soenen and Hennigar (1988). On the other hand, there are some studies that have found very weak or no association between stock prices and exchange rates (for instance, Franck and Young (1972), Eli Bartov and Gordon M.Bodnor (1994)).

The study by Naeem Muhammad and Abdul Rasheed (2001) uses monthly data on four South Asian countries, including Pakistan, India, Bangladesh and Sri- Lanka, for the period January 1994 to December 2000. They employed co-integration, vector error correction modeling technique and standard Granger causality tests to examine the long-run and short-run association between stock prices and exchange rates. The results of this study show no short-run association between the said variables for all four countries. There is no long-run relationship between stock prices and exchange rates for Pakistan and India as well. However, for Bangladesh and Sri Lanka there appear to be bidirectional causality between these two financial variables.

There is no theoretical consensus on the relationship between stock prices and exchange rates either. For instance, portfolio balance models of exchange rate determination postulate a negative relationship between stock prices and exchange rates. Franck and Young (1972) was the first study that examined the relationship between stock prices and exchange rates. They use six different exchange rates and found no relationship between these two financial variables. Aggarwal (1981) explored the relationship between changes in the dollar exchange rates and change in indices of stock prices. He uses monthly U.S. stock price data and the effective exchange rate for the period 1974-1978. His results, which were based on simple regressions, showed that stock prices and the value of the U.S. dollar is positively related and this relationship is stronger in the short run than in the long run.

Solnik (1987) examined the impact of several variables (exchange rates, interest rates and changes

in inflationary expectation) on stock prices. He uses monthly data from nine western markets (U.S., Japan, Germany, U.K., France, Canada, Netherlands, Switzerland, and Belgium). He found depreciation to have a positive but insignificant influence on the U.S. stock market compared to change in inflationary expectation and interest rates.

Soenen and Hanniger (1988) employed monthly data on stock prices and effective exchange rates for the period 1980-1986. They discover a strong negative relationship between the value of the U.S. dollar and the change in stock prices. However, when they analyzed the above relationship for a different period, they found a statistical significant negative impact of revaluation on stock prices. Amare and Mohsin (2000) examine the long-run association between stock prices and exchange rates for nine Asian countries (Japan, Hong Kong, Taiwan, Singapore, Thailand, Malaysia, Korea, Indonesia, and Philippines). They use monthly data from January 1980 to June 1998 and employed co integration technique. The long-run relationship between stock prices and exchange rates was found only for Singapore and Philippines. They attributed this lack of co-integration between the said variables to the bias created by the “omission of important variables”. When interest rate variable was included in their co-integrating equation they found co-integration between stock prices, exchange rates and interest rate for six of the nine countries.

To examine the long-run relationship between stock prices and exchange rates Naeem Muhammad and Abdul Rasheed (2001) employ the standard technique of co-integration. But their results suggested that in South Asian countries stock prices and exchange rates are unrelated. However, they suggested that the significance of our results could possibly be improved upon by applying daily or weekly data. The use of more frequent observations may better capture the dynamics of stock and currency market interrelationships.

Here most of the authors have used yearly or monthly based data to do the analysis which didn’t return that much satisfactory result (Naeem Muhammad and Abdul Rasheed (2001)). So here, collected updated data to do the analysis and hope that that will be much more accurate then previous analysis. One of the lacking of previous works in these sectors was most of them tried to follow one method to prove their analysis. But here tried to do the analysis first in one method then another method to compare both result for most optimum & better solution.

2.2 Questions and Hypotheses

3.2.1 Questions

Questions will be formulated in detail after doing exploratory task. However, the model of questions for this study is as follows:

Question 1 How is the price affecting portfolio formulation?

Question 2 What is the required volume of different securities affecting portfolio formulation?

Question 3 How does the size of the common stock risk premium affect portfolio diversification?

Question 4 How is the price earnings ratio affecting portfolio formulation?

Question 5 How is the earning per share affecting portfolio formulation?

Question 6 Is there any other factor which affecting portfolio formulation?

Question 7 How is the economic condition affecting portfolio formulation?

Question 8 How is the market Interest rate affecting portfolio formulation?

Question 9 What are the reasons behind portfolio formulation of different securities?

2.2.2 Hypotheses

From the above objectives and questions the following types of hypotheses formulated and tested.

Hypothesis 1

H0: More than or equal to 60% investors invest their money in the low price shares to formulate portfolio.

H1: Less than 60% investors invest their money in the low price shares to formulate portfolio

Ho: p>=0.6

H1: p < 0.6

Justification

A stock price is the price of a single share of a company’s stock. When viewed over long periods, the share price is directly related to the earnings and dividends of the firm. Over short periods, especially for younger or smaller firms, the relationship between share price and dividends can be quite irrational. To minimize the risk from one specific stock lot due to price change over time, investors would like to make a portfolio among different stock lots.

Hypothesis 2

H0: More than or equal to 80% investors invest their money in the portfolio when banks pay low interest rate.

H1: Less than 80% investors invest their money in the portfolio when banks pay low interest rate.

Ho: p> = 0.8

H1: p < 0.8

Justification

Higher interest rate for savings motivates the investors to invest in the banks or savings institutions. Interest rates also determine the cost and availability of credit for companies operating in an economy. Then low interest rate stimulates investment by making credit available easily and cheaply. Moreover, it implies lower cost of finance for companies and thereby assures higher profitability. On the contrary, higher interest rates result in higher cost of production which may lead to lower profitability and lower demand.

Hypothesis 3

H0: 70% investors invest their money to formulate portfolio when economic condition is good

H1: Less than 70% investors invest their money to formulate portfolio when economic condition is good.

Ho: p = 0.7

H1: p < 0.7

Justification

The performance of a company depends on the performance of the economy. If the company is booming, incomes rise, demand for goods increases, and hence the industries and companies in general tend to be prosperous. On the other hand, if the economy is in recession, the performance of companies will be generally bad. Investors are concerned with those variables in the economy which affect the performance of the company in which they intend to invest.

Hypothesis 4

H0: 80% investors prefer lower risk to invest their money for portfolio formulation.

H1: Less than 80% investors prefer lower risk to invest their money for portfolio formulation.

Ho: p = 0.8

H1: p < 0.8

Justification:

One of the major reasons to portfolio formulation is to minimize risk and maximize return. So most of the investors prefer to formulate portfolio to minimize their risk & maximize their return. There are many sources of risk that may affect the uncertainty in decision making of having a portfolio of investment. Therefore it becomes necessary to test whether investors invest in the lower risk or not.

Hypothesis 5

H0: 75% investors prefer to invest their money to formulate portfolio of those companies that give high earning per share.

H1: Less than 75% investors prefer to invest their money to formulate portfolio of those companies that give high earning per share.

Ho: p = 0.75

H1: p < 0.75

Justification:

An important aspect of EPS that’s often ignored is the capital that is required to generate the earnings (net income) in the calculation. Two companies could generate the same EPS number, but one could do so with less equity (investment) – that company would be more efficient at using its capital to generate income and, all other things being equal would be a “better” company. Investors also need to be aware of earnings manipulation that will affect the quality of the earnings number. It is important not to rely on any one financial measure, but to use it in conjunction with statement analysis and other measures.

2.3 Sampling Plan

The study carried out mainly through quantitative method. But personal observation and face to face conversation of the officers cannot ignore to data collection. Secondary data analysis and pilot study used for conducting this method. After Secondary data analysis pilot study carried out. Basing on the findings of the pilot study hypotheses tested.

It is almost impossible to do a complete census of most population. A properly designed sample is more efficiently managed, less costly and can provide the level of information necessary for most objectives. In this case, data has been collected from different investors and consultants. The following sections briefly discuss the steps followed in the sampling design.

- Target Population ( Sampling unit, extent, time)

- Sampling technique

- Sample size and

- Execution

As the time progress it focus on detail on sampling regarding objectives. It is focusing on demand analysis of factors affecting portfolio formulation.

2.4 Target Population

There have been two types of populations for this study. One is the investors of capital market and the other is the related consultancy firms/company.

2.4.1 Sampling Frame

There has been only one stratum within each population of interest, one from the investors and the other from the consultancy firms/company. Sampling frame was available for the study.

2.4.2 Sampling Technique

The research is mainly based on probability sampling method, which afterward follows non-probability sampling method to some extent. Out of the different probability, sampling methods random sampling has been used. Because the population is large and there is an equal and known chance of being selected for each member of the populations. At first, the stratum of sample from the population has randomly been identified then judgment sampling has been used to select the required number of subjects from each stratum. This sampling technique has been used because the entire sample has been drawn from one “representative” Dhaka Stock Exchange, even though the population includes both the security market.

2.4.3 Sample Size Determination

The sample size of a statistical sample is the number of observations that constitute it. It is typically denoted by n, a positive integer (natural number).

Typically, all else being equal, a larger sample size leads to increased precision in estimates of various properties of the population. This can be seen in such statistical rules as the law of large numbers and the central limit theorem. Repeated measurements and replication of independent samples are often required in measurement and experiments to reach a desired precision

To determine the Sample size the following formula is used:

n = σ2Z2/D2 where, n = sample size

σ = Standard deviation

D = Precision level

Z value is taken from table based on level of confidence.

It is assumed that, σ = 35

Z =1.64 for 90% level of confidence

D = ±4

So, we get n = 352*1.642/42

= 205.9225

= 206 (taking up to the next round figure)

Here the sample size is 206 but for some limitations (time, recourses etc.) data has been collected from 130 respondents’.

There were huge numbers of investors in Dhaka stock market. They were individual investors as well as institutional investors. But for this research conduct with the individual investors only. Very few of them was professional in this business. Most of the investors were doing other jobs while doing this business. During survey, it is found that there were some investors who are officers, students, other businessmen and others. There were institutional investors but for some limitation such as data accessibility and availability, data has been collected from only general investors for this research. From 130 respondents 20 investors was professionals, 30 investors was students, 30 investors was officers, 40 investors was other businessmen and 10 investors was doing other jobs.

2.5 Sources and Method of Data Collection

Primary and secondary sources have been used for data collection. Secondary data has been collected from different DSE Monthly review, company Annual report, publications, newspapers, magazines and websites. Primary data has been collected through taking door-to-door interview. No agencies have been engaged; rather the researcher has carried out the field survey for collecting data. Data has been collected from the investors and the consultants related to the stock market.

The structured questionnaires have been used for the field survey. Each set of questionnaire contains nine questions. The questions were both open ended and closed ended questions and scale response format. The average interviewing time was ten to twelve minutes.

2.5.1 Analysis Plan

After collection of all necessary data, those have been analyzed in the following two ways:

Subjective Analysis Qualitative data have been analyzed critically using judgment and previous knowledge.

Statistical Analysis The survey was mostly generating nominal, ordinal, interval and ratio data. To analyze the raw data appropriate statistical tools have been used. Primary data from the questionnaire has been placed in the data instrument sheet.

Frequency distribution and arithmetic mean of the respondents have been used to analyze data. Testing of the hypotheses was done using one and two-tailed Z test. Based on the tests hypotheses have been accepted or rejected. Correlation analysis was done for the purpose of trend analysis.

2.5.2 Assumptions

All research studies make assumptions. Like other research studies, the researcher has made some assumptions to conduct this study as follows:

- The sample selected represents the population.

- The instrument (survey) used in this study has validity and is measuring the desired constructs.

- Respondents have answered in the survey truthfully.

2.6 BRIEF IDEA ON PORTFOLIO FORMULATION

This section gives a brief idea on portfolio formulation before entering the minutiae of the report. It discusses about the portfolio, phases of portfolio management, objectives of portfolio management, investment avenues and different factors affecting portfolio formulation in details.

2.6.1 Portfolio

Investing entire savings in a group of securities instead of single security is called portfolio.

2.6.2 Portfolio Management

An investor considering investment in securities is faced with the problem on choosing from among large number of securities. His choice depends upon the risk-return characteristics of individual securities. An investor invests his funds in a portfolio expecting to get a good return consistent with the risk that he has to bear. It is evident that rational investment activity involves creation of an investment portfolio. Portfolio management comprises all the processes involved in the creation and maintenance of an investment portfolio. It deals specifically with security analysis, portfolio analysis, portfolio selection, portfolio revision and portfolio evaluation.

2.6.3 Phases of Portfolio Management

Portfolio management is a process encompassing many activities aimed at optimizing the investment of one’s funds. Five phases can be identified in this process:

- Security analysis

- Portfolio analysis

- Portfolio selection

- Portfolio revision and

- Portfolio evaluation

Each phase is an integral part of the whole process and the success of portfolio management depends upon the efficiency in carrying out each of these phases.

- Security Analysis The securities available to an investor for investment are numerous and of various types. Traditionally the securities were classified into ownership securities such as equity shares and preferences shares and creditorship securities such as debentures and bonds. From this group of securities the investor has to choose those securities which he considers worthwhile to be included in his investment portfolio.

- Portfolio Analysis A portfolio is a group of securities held together as investment. Investors invest their funds in a portfolio of securities rather than in a single security because they are risk averse. By constructing a portfolio, investors attempt to spread risk by not putting all their eggs into one basket. Thus diversification of one’s holdings is intended to reduce risk in investment.

- Portfolio Evaluation The objective of constructing a portfolio and revising it periodically is to earn maximum returns with minimum risk. Portfolio evaluation is the process which is concerned with assessing the performance of the portfolio over a selected period of time in terms of return and risk.

- Portfolio Selection The goal of portfolio construction is to generate a portfolio that provides the highest returns at a given level of risk. A portfolio having this characteristic is known as an efficient portfolio. From the efficient portfolios, the optimal portfolio has to be selected for investment.

- Portfolio Revision Having constructed the optimal portfolio, the investor has to constantly monitor the portfolio to ensure that it continues to be optimal. The investor has to revise the portfolio in the light of the developments of the market. This revision leads to purchase of some new securities and sale of some of the existing securities from the portfolio.

2.6.4 Objective of the Portfolio Management

The objective of the portfolio management is to invest securities in such a way that one maximizes one’s returns and minimizes risks in order to achieve one’s investment objective. A good portfolio should have multiple objectives and achieve a sound balance among them. Any one objective should not be given undue importance at the cost of others. Presented below are some important objectives of portfolio management.

- Safety of the investment The most important objective of a portfolio, no matter who owns it, is to ensure that the investment is absolutely safe. Other consideration like income, growths etc. only come into the picture after the safety of our investment is ensured. Investment safety or minimization of risks is one of the important objectives of portfolio management. There are many types of risks, which are associated with investment in equity stocks, including super stocks. Bear in mind that there is no such thing as a zero-risk investment. Moreover, relatively low risk investments give correspondingly lower returns. Investors can try and minimize the overall risk or bring it to an acceptable level by developing a balanced and efficient portfolio. A good portfolio of growth stocks satisfies all the objectives outlined above.

- · Stable current returns Once investment safety is guaranteed, the portfolio should yield a steady current income. The current returns should at least match the opportunity cost of the investor. It’s referring current income by way of interest or dividend, not capital gains.

- Appreciation in the value of capital A good portfolio should appreciate in value in order to protect the investor from any erosion in purchasing power due to inflation. In other words, a balanced portfolio must consist of certain investments that to appreciate in real value after adjusting for portfolio.

- Marketability A good portfolio consists of investments, which can be marketed without difficulty. If there are too many unlisted or inactive shares in portfolio, investor will face problems in encasing them, and switching from one investment to another. It is desirable to invest in companies listed on major stock exchanges, which are actively traded.

- Liquidity The portfolio should ensure that are enough funds available at short notice to take care of the investors liquidity requirements. It is desirable to keep a line of credit from a bank for use in case it becomes necessary to participate in right issues, or fore any other personal needs.

- Tax planning Since taxation is an important variable in total planning; a good portfolio should enable its owner to enjoy a favorable tax shelter. The portfolio should be developed considering not only income tax, but also capital gains tax as well. What a good portfolio aims at is tax planning, not tax evasion or tax avoidance.

2.7 Investment Avenues

There are a large number of investment avenues for savers in Bangladesh. Some of them are marketable and liquid while others are non marketable. Some of them are highly risky while some others are almost risk less. The investor has to choose proper avenues from among them depending on his preferences, needs and ability to assume risk. The investment avenues can be broadly categories under the following heads:

- Corporate securities

- Deposits in banks and non-banking companies

- UTI and other mutual fund schemes

- 5. Life insurance policies

- Provident fund schemes

- Post office deposits and certificates

- Government and semi-government securities

ü Corporate securities Corporate securities are the securities issued by joint stock companies in the private sector. These include equity shares, preference shares and debentures. Equity shares have variable dividend and hence belong to the high risk-high return category, while preference shares and debentures have fixed returns with lower risk.

ü Deposits among the non-corporate investments, the most popular are deposits with banks such as savings accounts and fixed deposits. Savings deposits have low interest rates whereas fixed deposits have higher interest rates varying with the period of maturity. Interest is payable quarterly or half-yearly. Fixed deposits may also be recurring deposits wherein savings are deposited at regular intervals. Some banks have reinvestment plans wherein the interests are paid on maturity. Joint stock companies also accept fixed deposits from the public. The maturity period varies from three to five years. Fixed deposits in companies have high risk since they are unsecured, but they promise higher returns than bank deposits. Fixed deposit in non-banking financial companies is another investment avenue open to savers. Non-banking financial companies include leasing companies, hire purchase companies, investment companies, chit funds, etc. deposits in non-banking financial companies carry higher returns with higher risk compared to bank deposits.

ü Mutual fund schemes mutual funds offer various investment schemes to investors. A number of commercial banks and financial institutions have set up mutual funds. Recently mutual funds have been set up in the private sector also.

ü Post office deposits and certificates The investment avenues provided by post offices are generally non-marketable. Moreover, the major investment in post office enjoys tax concessions also. Post offices accept savings deposits as well as fixed deposits from the public. There is also a recurring deposits scheme which is an instrument of regular monthly savings.

ü Life insurance policies The Life Insurance Corporation offers many investment schemes to investors. These schemes have the additional facility of life insurance cover. Some of the schemes of Life Insurance Company are Whole Life Policies, Jeevan Bima, Convertible Whole Life Assurance Policies, Endowment Assurance Policies, Marriage Endowment Plan, etc.

ü Provident fund schemes Provident fund schemes are compulsory deposit schemes applicable to employees in the public and private sectors. There are three kinds of provident funds applicable to different sectors of employment, namely Statutory Provident Fund, Recognized Provident Fund and Unrecognized Provident Fund. In addition to these, there is a voluntary provident fund scheme which is open to any investor whether employed or not. This is known as the Public Provident Fund. Any member of the public can join the scheme which is operated by the post offices and the Bangladesh Bank.

ü Government and Semi-Government Securities The government and semi-government bodies like the public sector undertakings borrow money from the public through the issue of government securities and public sector bonds. These are less risky avenues of investment because of the credibility of the government and government undertakings.

2.8 Fundamental Analysis of Portfolio Management

The primary motive of buying a share is to sell it subsequently at a higher price. In many cases, dividends are also expected. Thus, dividends and price changes constitute the return from investing in shares. Consequently, an investor would be interested to know the dividend to e paid on the share in the future as also the future price of the share. These values can only be estimated and not predicted with certainty. These values are primarily determined by the performance of the industry to which the company belongs and the general economic and socio-political scenario of the country. An investor who would like to be rational and scientific in his investment activity has to evaluate a lot of information about the past performance and the expected future performance of companies, industries and the economy as a whole before taking the investment decision. Such evaluation or analysis is called fundamental analysis.

Fundamental analysis is really a logical and systematic approach to estimating the future dividends and share price. It is based on the basic premise that share price determined by a number of fundamental factors relating to the economy, industry and company. Hence, the economy fundamental, industry fundamentals and company fundamentals have to e considered while analyzing a security for investment purpose. Fundamental analysis is in other words, a detailed analysis of the fundamental factors affecting the performance of companies. Each share is assumed to have an economic worth based on its present and future earning capacity. This is called its intrinsic value or fundamental value. The purpose of fundamental analysis is to evaluate the present and future earning capacity of a share based on the company, industry and company fundamentals and thereby assess the intrinsic value of the share. The investor can then compare the intrinsic value of the share with the prevailing market price to arrive at an investment decision. If the market price of the share is lower than its intrinsic value, the investor would decide to buy the share as it is underpriced. The price of such a share is expected to move up in future to match with its intrinsic value. On the contrary, when the market price of a share is higher than its intrinsic value, it is perceived to be overpriced. The market price of such a share is expected to come down in future and hence, the investor would decide to sell such a share. Fundamental analysis thus provides an analytical framework is known as economy-industry-company analysis. Fundamental analysis insists that no one should purchase or sell a share on the basis of tips and rumors. The fundamental approach calls upon the investor to make his buy or sell decision on the basis of detailed analysis information about the company.

2.9 Economy Analysis for Portfolio Management

The performance of a company depends on the performance of the economy. If the company is booming, incomes rise, demand for goods increases, and hence the industries and companies in general tend to be prosperous. On the other hand, if the economy is in recession, the performance of companies will be generally bad. Investors are concerned with those variables in the economy which affect the performance of the company in which they intend to invest. A study of these economic variables would give an idea about future corporate earnings and the payment of dividends and interest to investors. Let us look at some of the key economic variables that an investor must monitor as part of his fundamental analysis.

2.10 Economic Forecasting for Portfolio Management

Economy analysis is the first stage of fundamental analysis and starts with an analysis of historical performance of the economy. But as investment is a future-oriented activity, the investor is more interested in the expected future performance of the overall economy and its various segments. For this, forecasting the future direction of the economy becomes necessary. Economic forecasting thus becomes a key activity in economy analysis. The central theme in economic forecasting is to forecast the national income with its various components. Gross national product or GNP is a measure of the national income. It is the total value of the final output of goods and services produced in the economy. It is a measure of the total economic activities over a specified period of time and is an indicator of the level and rate of growth of economic activities. An investor would be particularly interested in forecasting the various components of the national income, especially those components that have a bearing on the particular industries and companies that he is analyzing.

2.11 Industry Analysis for Portfolio Management

An investor ultimately invests his money in the securities of one or more specific companies. Each company can be characterized as belonging to an industry. The performance of companies would, therefore, be influenced by the fortunes of the industry to which it belongs. For this reason an analyst has to undertake an industry analysis so as to study the fundamental factors affecting the performance of different industries. At any stage in the economy, there are some industries which are fast growing while others are stagnating or declining. If an industry is growing, the companies within the industry may also be prosperous. The performance of companies will depend, among other things, upon the state of the industry to which they belong. Industry analysis refers to an evaluation of the relative strengths and weakness of particular industries.

2.12 Company Analysis for Portfolio Management

Company analysis is the final stage of fundamental analysis. The economy analysis provides the investor a road outline of the prospects of growth in the economy. The industry analysis helps the investor to select the industry in which investment would be rewarding. Now he has to decide the company in which he should invest his money. Company analysis provides the answer to this question. Company analysis deals with the estimation of return and risk of individual shares. This calls for information which influences investment decisions. Information regarding companies can be broadly classified into two road groups: internal and external. Internal information consists of data and events made public by companies concerning their operations. The internal information sources include annual reports to shareholders, public and private statements of officers of the company, the company’s financial statements, and etc. external sources of information are those generated independently outside the company. These are prepared by investment services and the financial press. In company analysis, the analyst tries to forecast the future earnings of the company because there is strong evidence that earning have a direct and powerful effect upon share prices. The level, trend and stability of earnings of a company, however, depend upon a number of factors concerning the operations of the company.

2.13 Factors Analysis for Portfolio Management

ü Growth Rates of National Income: The rate of growth of the national economy is an important variable to be considered by an investor. GNP, NNP and GDP are the different measures of the total income or total economic output of the country as a whole. The growth rates of these measures indicate the growth rate of the economy. The estimates of GNP, NNP and GDP and their growth rates are made available by the government from time to time. The estimated growth rate of the economy would be a pointer towards the prosperity of the economy. An economy typically passes through different phases of prosperity, known as the different stages of the economic or business cycle. The four stage of the economic cycle are depression, recovery, boom and recession. The stage of the economic cycle through which a country passes has a direct impact on the performance of industries and companies. Depression is the worst of the four stages. During a depression, demand is low and declining, inflation is often high and so are interest rates. During the recovery stage the economy begins to revive after a depression. Demand picks up leading to more investments in the economy. Production, employment and profits are on the increase. The boom phase of the economic cycle is characterized by high demand. Investment and production are maintained at a high level to satisfy the high demand. Companies generally post higher profits. The boom phase gradually slows down. The economy slowly begins to experience a downturn in demand, production, employment, etc. the profits of companies also start to decline. This is the recession stage of the business cycle. While analyzing the growth rate of the economy, an investor would do well to determine the stage of the economic cycle through which the economy is passing and evaluate its impact on his investment decision.

ü Inflation: Prevailing in the economy has considerable impact on the performance of companies. Higher rates of inflation upset business plans, lead to cost escalation and result in a squeeze on profit margins. On the other hand, inflation leads to erosion of purchasing power in the hands of consumers. This will result in lower demand for products. Thus, high rates of inflation in an economy are likely to affect the performance of companies adversely. Industries and companies prosper during times of low inflation. Inflation is measured both in terms of wholesale prices through the wholesale price index and in terms of retail prices through the consumer price index. These figures are available on weekly or monthly basis. As part of the fundamental analysis, an investor should evaluate the inflation rate prevailing in the economy currently as also the trend of inflation likely to prevail in the future.

ü Interest rates: Interest rates determine the cost and availability of credit for companies operating in an economy. A low interest rate stimulates investment by making credit available easily and cheaply. Moreover, it implies lower cost of finance for companies and thereby assures higher profitability. On the contrary, higher interest rates result in higher cost of production which may lead to lower profitability and lower demand. The interest rates in the organized financial sector of the economy are determined by the monetary policy of the government and the trends in money supply. These rates are thus controlled and vary within certain ranges. But the interest rates in the unorganized financial sector are not controlled and may fluctuate widely depending upon the demand and supply of funds in the market. Further, long-term interest rates differ from short-term interest rates. An investor has to consider the interest rates prevailing in the different segments of the economy and evaluate their impact on the performance and profitability of companies.

ü Government revenue, expenditure and deficits: As the government is the largest investor and spender of money, the trends in government revenue, expenditure and deficits have a significant impact on the performance of industries and companies. Expenditure by the government stimulates the economy by creating jobs and generating demand. Since a major portion of demand in the economy is generated by government spending, the nature of government spending is of great importance in determining the fortunes of many an industry.

ü Exchange Rates: The performance and profitability of industries and companies that are major importers or exporters are considerably affected by the exchange rates of the taka against major currencies of the world. A depreciation of the taka improves the competitive position of Bangladesh products in foreign markets, thereby stimulating exports. But it would also make imports more expensive. A company depending heavily on imports may find devaluation of the taka affecting its profitability adversely. The exchange rate s of the take influence by the balance of trade deficit, the balance of payments deficit and also the foreign exchange reserves of the country. The excess of imports over exports is called balance of trade deficits. The balance of payments deficits represent the net difference payable on account of all transactions such as trade, services and capital transaction. If these deficits increase, there is a possibility that the taka may depreciate in value. A country needs foreign exchange to meet several commitments such as payment for imports and servicing of foreign debts. Balance of payment deficit typically leads to decline in foreign exchange reserves as the deficit has to be met from the reserve. The size of the foreign exchange reserve is a measure of the strength of the taka on external account. Large foreign exchange reserves help to increase the value of the taka against other currencies. The exchange rates of the rupee against the major currencies of the world are published daily in the financial press. An investor has to keep track of the trend in exchange rates of taka. An analysis of the balance of trade deficit, balance of Payments deficit and the foreign exchange reserves will help to project the future trends in exchange rates.

ü Economic and political Stability A stable political environment is necessary for steady and balanced growth. No industry or company can grow and prosper in the midst of political turmoil. Stable long-term economic policies are what are needed for industrial growth. Such stable policies can emanate only from stable political systems as economic and political factors are inter-linked. A stale government with clear cut long-term economic policies will be conductive to good performance of the economy.

ü Risk Tolerance Risk refers to the volatility of portfolio’s value. The amount of risk the investor is willing to take on is an extremely important factor. While some people do become more risk averse as they get older; a conservative investor remains risk averse over his life-cycle. An aggressive investor generally dares to take risk throughout his life. If an investor is risk averse and he takes too much risk, he usually panic when confronted with unexpected losses and abandon their investment plans mid-stream and suffers huge losses.

ü Return Needs This refers to whether the investor needs to emphasize growth or income. Most younger investors who are accumulating savings will want returns that tend to emphasize growth and higher total returns, which primarily are provided by equity shares. Retirees who depend on their investment portfolio for part of their annual income will want consistent annual payouts, such as those from bonds and dividend-paying stocks. Of course, many individuals may want a blending of the two Þ some current income, but also some growth.

ü Investment Time Horizon The time horizon starts when the investment portfolio is implemented and ends when the investor will need to take the money out. The length of time you will be investing is important because it can directly affect your ability to reduce risk. Longer time horizons allow you to take on greater risks Þ with a greater total return potential Þ because some of that risk can be reduced by investing across different market environments. If the time horizon is short, the investor has greater liquidity needs Þ some attractive opportunities of earning higher return has to be sacrificed and the result is reduced in return. Time horizons tend to vary over the life-cycle. Younger investors who are only accumulating savings for retirement have long time horizons, and no real liquidity needs except for short-term emergencies. However, younger investors who are also saving for a specific event, such as the purchase of a house or a child’s education, may have greater liquidity needs. Similarly, investors who are planning to retire, and those who are in retirement and living on their investment income, have greater liquidity needs.

ü Tax Exposure Investors in higher tax brackets prefer such investments where the return is tax exempt, others will have no such preference.

3.01 Preliminary Discussion

In this study, we use panel co-integration methods to investigate the relationship between stock prices and earnings-per-share (EPS). Furthermore, we consider whether stock prices respond to EPS under the different level of growth rate of operating revenue. The empirical result indicated that the co-integration relationship existed between stock prices and EPS in the long-run. Furthermore, we found that for the firm with a high level of growth rate, EPS has less power in explaining the stock prices; however, for the firm with a low level of growth rate, EPS has a strong impact in stock prices.

The phenomenon of the mean-reversion discussed from the literatures explore whether the stock price followed random walk. If the stock prices violate the trend of random walk, one possibility is the stock prices followed mean-reversion process. If the stock prices followed mean reversion in the long-run, the price movements should be predictable from the movements in firm fundamental values. In this sense, determining whether stock prices are mean-reversion is a very important issue for investors. Consequently, to analysis equity fundamentals, what is important is to verify whether the stock price moves with its firm’s fundamental. Proxies for firm’s fundamental values used in previous studies include earnings-per-share (EPS), earnings, dividends and net asset values (NAV).

The price to earnings, or P/E, ratio is a widely used stock evaluation criteria. The major purpose of a corporation centers on earning a profit, or in the stock market parlance, earnings. For many stocks, the primary factor in the determination of the share price represents the amount of earnings the company will earn. Many investors use the relationship between the share price and earnings in their stock research and selection process.

Identification: – Corporations with publicly traded stocks report their financial results quarterly, or four times per year. At this time, investors hold a high interest in the reported earnings per share (EPS) —the net income for the quarter divided by the total number of company shares outstanding. The total of four quarters earnings makes up the annual earnings per share, while the annual is the number reported by financial websites such as Yahoo Finance and Google Finance on the stock price screens for the individual companies.

Function: – The current stock share price divided by the sum of the past four quarters EPS is called the price-to-earnings or P/E ratio. (The stock price pages of the financial websites also provide the P/E ratio). The ratio is widely used to get a quick idea of the relative value of a stock. If one stock has a share price of $20 and the other has reached $50, but both have the same P/E ratio, the two company shares have the same relative value in the eyes of investors.

Considerations: – In all cases, P/E remains a relative value measurement. Investors can use it to check a company’s current P/E to the historic average, or they can compare P/E with that of competitors or the overall market, or analyze it in relation to the growth in earnings per share. Growth stocks have high P/Es, as investors bid up the share price to participate in the future growth of the company.

Types: – The classic P/E ratio is based on trailing earnings, or the earnings from the past four quarters. This P/E ratio shows the relationship of the current share price to the previous year’s net earnings. Many investors like to look at the forward P/E—the current share price divided by the projected earnings for the next four quarters. The forward P/E gives the investor an idea of the company’s value based on its probable future profits. Not all companies can make the projected earnings. However, so forward P/E gives just a possibility of the stock’s future performance.

Significance: – Investors use P/E to get a first indication of whether the stock meets their investment criteria and goals. They need to conduct further research to determine the quality of the earnings and whether the company can produce the earnings growth rate the P/E ratio is forecasting. A one-time positive or negative charge to earnings can make the P/E ratio an unreliable indicator. Also, companies with negative earnings have no P/E ratio because they have no “E.”

3.02 General View

If we think about our capital market that time we will found rumor is the main factors based on this share price rise or decline. In normal sense when a company is going to offer dividend, it may be stock or cash dividend, the share price will increase. But in our country the price will increase at abnormal rate. Suppose, the dividend declared 10% of a Tk. 100 (Par value), the price is increase more than 10% that should not be consider as a good sign. Bangladeshi people are not so fond of dividend because they invest their money for a short period. EPS is the one of major factor for which price rise and sometimes rise unexpectedly.

3.03 Formulation of the Analysis

Here, we have shown an empirical study that shows the relationship between shares price and earnings per share that means profitability. We have shown two things that are share price before declaring dividend and after declaring dividend. To do this, we have taken DSE-20 shares as sample data. Our total process is as following:-

- Our sample data is DSE-20 shares.

- Here, we have taken moving average to calculate the average price and average EPS.

- We have converted some par value into Tk. 10 for our convenience.

- First, we have shown how strongly share price is related to without EPS.

- Secondly, we have shown how strongly share price is related to with EPS.

- Then we have analysis this relationship by coefficient of correlation [r] and coefficient of determination [r2].

3.04 Sample Data

Company | Before EPS Price(X) | After Eps Price(Y) | EPS Avg |

| Islami Bank Bd Ltd | 61.9 | 64.04 | 4.75 |

| NBL | 82.5 | 73.15 | 15.57 |

| Prime Bank | 53.8 | 69.78 | 5.96 |

| Southeast Bank | 37.93 | 48.7 | 5.42 |

| Dhaka Bank | 55.5 | 48.67 | 6.31 |

| Uttara Finance | 251.4 | 305.8 | 12.76 |

| Bangladesh Lamps | 193.5 | 241.74 | 4.3 |

| Singer Bangladesh | 614.38 | 573.88 | 12.38 |

| BATBC | 628.1 | 632.5 | 47.58 |

| AMCL (Pran) | 126.6 | 170.7 | 4.8 |

| BOC Bangladesh | 577.15 | 684.1 | 32.23 |

| Square Textile | 164.9 | 175 | 6.01 |

| Beximco Pharma | 268.8 | 347.65 | 36.3 |

| ACI Limited. | 259.45 | 372.35 | 5.88 |

| Square Pharma | 308.5 | 360.48 | 13.56 |

| Meghna Cement | 228.3 | 221 | 5.4 |

| Apex Tannery | 124.25 | 168.75 | 4.05 |

| Bata Shoe | 532.4 | 636.2 | 30 |

| Monno Ceramic | 63.28 | 99.66 | 8.14 |

| GQ Ball Pen | 152.25 | 208.7 | 4.03 |

Source: DSE monthly review.

Before EPS Price: These prices are taken 3 months later after giving dividend by the moving average.

After EPS Price: These prices are taken after declaring dividend by the motioned company over the year using moving average (Cash, Bonus Share or Right Issue)

3.05 Coefficient of determination R2:

In statistics, the coefficient of determination R2 is used in the context of statistical models whose main purpose is the prediction of future outcomes on the basis of other related information. It is the proportion of variability in a data set that is accounted for by the statistical model. It provides a measure of how well future outcomes are likely to be predicted by the model.

The “variability” of the data set is measured through different sums of squares:

the total sum of squares (proportional to the sample variance);

the regression sum of squares, also called the explained sum of squares.

, the sum of squares of residuals, also called the residual sum of squares.

In the above is the mean of the observed data:

Where n is the number of observations.

The notations SSR and SSE should be avoided, since in some texts their meaning is reversed to Residual sum of squares and Explained sum of squares, respectively.

The most general definition of the coefficient of determination is

The coefficient of determination, r 2, is useful because it gives the proportion of the variance (fluctuation) of one variable that is predictable from the other variable. It is a measure that allows us to determine how certain one can be in making predictions from a certain model/graph.

v The coefficient of determination is the ratio of the explained variation to the total variation.

v The coefficient of determination is such that 0 < r 2 < 1, and denotes the strength of the linear association between x and y.

v The coefficient of determination represents the percent of the data that is the closest to the line of best fit. For example, if r = 0.922, then r 2 = 0.850, which means that 85% of the total variation in y can be explained by the linear relationship between x and y (as described by the regression equation). The other 15% of the total variation in y remains unexplained.

v The coefficient of determination is a measure of how well the regression line represents the data. If the regression line passes exactly through every point on the scatter plot, it would be able to explain all of the variation. The further the line is away from the points, the less it is able to explain.

3.06 Correlation coefficient R:

Also, known as r, R, or Pearson’s r, a measure of the strength of the linear relationship between two variables that is defined in terms of the (sample) covariance of the variables divided by their (sample) standard deviations. The correlation coefficient a concept from statistics is a measure of how well trends in the predicted values follow trends in past actual values. It is a measure of how well the predicted values from a forecast model “fit” with the real-life data.

The quantity r, called the linear correlation coefficient, measures the strength and the direction of a linear relationship between two variables.

The mathematical formula for computing r is:

Where n is the number of pairs of data. (Aren’t you glad you have a graphing calculator that computes this formula?)

The value of r is such that -1 < r < +1. The + and – signs are used for positive linear correlations and negative linear correlations, respectively.

Positive correlation: If x and y have a strong positive linear correlation, r is close to +1. An r value of exactly +1 indicates a perfect positive fit. Positive values indicate a relationship between x and y variables such that as values for x increases, values for y also increase.

Negative correlation: If x and y have a strong negative linear correlation, r is close to -1. An r value of exactly -1 indicates a perfect negative fit. Negative value indicates a relationship between x and y such that as values for x increase, values for y decrease.

No correlation: If there is no linear correlation or a weak linear correlation, r is close to 0. A value near zero means that there is a random, nonlinear relationship between the two variables.

Note that r is a dimensionless quantity; that is, it does not depend on the units employed.

A perfect correlation of ± 1 occurs only when the data points all lie exactly on a straight line. If r = +1, the slope of this line is positive. If r = -1, the slope of this line is negative.

A correlation greater than 0.8 is generally described as strong, whereas a correlation less than 0.5 are generally described as weak.

3.07 R & R2 Calculation

Company | Before EPS Price(X) | After Eps Price (Y) | ||

| Islami Bank Bd Ltd | 61.9 | 64.04 | ||

| NBL | 82.5 | 73.15 | ||

| Prime Bank | 53.8 | 69.78 | ||

| Southeast Bank | 37.93 | 48.7 | ||

| Dhaka Bank | 55.5 | 48.67 | ||

| Uttara Finance | 251.4 | 305.8 | ||

| Bangladesh Lamps | 193.5 | 241.74 | ||

| Singer Bangladesh | 614.38 | 573.88 | ||

| BATBC | 628.1 | 632.5 | ||

| AMCL (Pran) | 126.6 | 170.7 | ||

| BOC Bangladesh | 577.15 | 684.1 | ||

| Square Textile | 164.9 | 175 | ||

| Beximco Pharma | 268.8 | 347.65 | ||

| ACI Limited. | 259.45 | 372.35 | ||

| Square Pharma | 308.5 | 360.48 | ||

| Meghna Cement | 228.3 | 221 | ||

| Apex Tannery | 124.25 | 168.75 | ||

| Bata Shoe | 532.4 | 636.2 | ||

| Monno Ceramic | 63.28 | 99.66 | ||

| GQ Ball Pen | 152.25 | 208.7 |

Correlation coefficient R: 0.980445635 (From excel sheet)

Coefficient of determination R2: 0.961273643(From excel sheet)

3.08 Interpretation Part

Interpretation R2: R2 is a statistic that will give some information about the goodness of fit of a model. In regression, the R2 coefficient of determination is a statistical measure of how well the regression line approximates the real data points. An R2 of 1.0 indicates that the regression line perfectly fits the data. Values of R2 outside the range 0 to 1 can occur where it is used to measure the agreement between observed and modeled values and where the “modeled” values are not obtained by linear regression and depending on which formulation of R2 is used. If the first formula above is used, values can never be greater than one. If the second expression is used, there are no constraints on the values obtainable. In our study the result is 0.961273643. So it expresses two variable perfectly.

Interpretation R: The correlation coefficient is a number between 0 and 1. If there is no relationship between the predicted values and the actual values the correlation coefficient is 0 or very low (the predicted values are no better than random numbers). As the strength of the relationship between the predicted values and actual values increases so does the correlation coefficient. A perfect fit gives a coefficient of 1.0. Thus the higher the correlation coefficient the better.

Here, our result is 0.980445635 which is near about 1.Therefore, EPS and share price is highly correlated. Indeed, we can say when one company declared dividend then the price increases.

The value -1 represents a perfect negative correlation (when one increases, the other decreases in exactly the same proportion.

The value +1 represents a perfect correlation (when one increases, the other increases in exactly the same proportion.

The value 0 represents a lack of correlation.

5.01 Recent Crash in DSE

Dhaka Stock Exchange (Generally known as DSE) is the main stock exchange of Bangladesh. It is located in Motijheel at the heart of the Dhaka city. It was incorporated in 1954. Dhaka stock exchange is the first stock exchange of the country. As of 18 August 2010, the Dhaka Stock Exchange had over 750 listed companies with a combined market capitalization of $50.28 billion. Dhaka Stock Exchange (DSE) is a public limited company. Now-a-days DSE has become attractive source but not in a knowledgeable way or for a sustainable future. Due to different problems and decisions of authority recent fall is occurred in DSE price.

Stock prices at the country’s main capital market -the Dhaka Stock Exchange (DSE) witness Sunday the steepest ever single-day fall 551 points or 6.71 per cent, forcing angry retail investors to stage rowdy street protests in Dhaka and some other district towns. With market indices nose-diving soon after the start of the day’s trading at the DSE, angry investors came out of the brokerage houses, blocked the main street and, at one stage, turned mildly violent. They clashed with police, leaving several people, including a photo-journalist, injured. The protesters also demanded resignation of heads of a few national institutions whom they blamed for the stock market debacle. Business activities in the business district Motijheel were disrupted for about two hours until 2.0pm on the day. Out of 243 issues traded Sunday, only 05 gained, 236 declined and two remained unchanged. Banking and insurance issues were the major losers on the day when total turnover stood at Tk. 14.90 billion, up by 17 per cent compared to that of the last trading session.

Following the massive erosion, the Securities and Exchange Commission (SEC) reversed some of its earlier decision, taken to rein in the soaring market. But those could hardly leave any impact on the sliding stock prices. The general index (DGEN) at the DSE has lost 2264 points or 25 per cent since December 05 last after hitting the highest ever level-8918. The market shed 547 points within 80 minutes from the start of the day’s trading on December 08. But stock prices started regaining mysteriously as a section of investors took to the streets and resorted to violent protests and ended the day with 105 points lower. On December 13, Sunday, the market went through major price correction-285 points. Stock prices at the DSE more than doubled over period of last one year with the active participation of both institutional and general investors

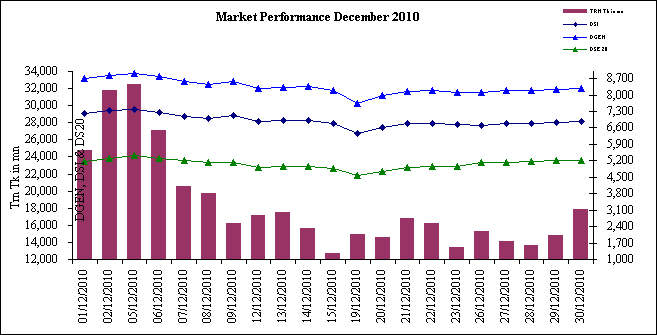

Figure: Market Performance December-2010

Look behind Dcember-09,10 to March-03,11

Date | Total Trade | Total Volume | Total Value in Taka(mn) | Total Market Cap. in Taka(mn) | DSI Index | DSE General Index |

3/3/2011 | 129253 | 56275877 | 5038.247 | 2506932.35 | 4507.832 | 5428.405 |

3/2/2011 | 134730 | 65191754 | 5915.011 | 2448837.83 | 4392.487 | 5292.175 |

3/1/2011 | 88811 | 44104562 | 4317.105 | 2565830.05 | 4646.669 | 5601.599 |

2/28/2011 | 121467 | 52798795 | 4894.189 | 2413072.93 | 4317.893 | 5203.085 |

2/27/2011 | 121536 | 54911094 | 5012.711 | 2512870.94 | 4533.65 | 5463.352 |

2/24/2011 | 121372 | 52813261 | 5592.521 | 2641734.01 | 4810.408 | 5800.939 |

2/23/2011 | 122350 | 50953170 | 5736.74 | 2726898.73 | 4989.904 | 6018.484 |

2/22/2011 | 171487 | 80487415 | 9629.592 | 2785241.82 | 5119.72 | 6173.386 |

2/20/2011 | 93814 | 52954618 | 5777.112 | 2871495.97 | 5295.597 | 6389.625 |

2/15/2011 | 148795 | 61150304 | 6893.952 | 2710495.46 | 4915.62 | 5926.354 |

2/14/2011 | 128807 | 68769464 | 6630.694 | 2580007.08 | 4633.473 | 5579.505 |

2/13/2011 | 151499 | 63834810 | 7156.832 | 2760886.01 | 5020.484 | 6052.412 |

2/10/2011 | 115894 | 50547928 | 5631.425 | 2938380.39 | 5409.103 | 6527.19 |

2/9/2011 | 137064 | 59936623 | 6736.779 | 2980849.16 | 5528.803 | 6673.409 |

2/8/2011 | 151890 | 67956526 | 7876.879 | 3042013.32 | 5651.798 | 6822.854 |

2/7/2011 | 125723 | 54764424 | 6099.751 | 2884763.78 | 5306.469 | 6394.531 |

2/6/2011 | 134030 | 58785679 | 7052.2 | 2996982.5 | 5571.631 | 6719.045 |

2/3/2011 | 127285 | 56203580 | 7365.884 | 3146170.01 | 5903.103 | 7125.332 |

2/2/2011 | 130565 | 56983718 | 7414.894 | 3195106.51 | 6054.671 | 7309.137 |

2/1/2011 | 154977 | 76524275 | 9384.959 | 3190829.26 | 6032.426 | 7280.981 |

1/31/2011 | 174940 | 82706203 | 10776.391 | 3267387.07 | 6198.818 | 7484.228 |

1/30/2011 | 166422 | 81048070 | 10020.206 | 3281198.74 | 6271.533 | 7572.61 |

1/27/2011 | 168305 | 83621580 | 10302.428 | 3215308.2 | 6120.923 | 7385.914 |

1/26/2011 | 87165 | 50456101 | 5875.937 | 3190844.78 | 6040.702 | 7280.014 |

1/25/2011 | 29281 | 18809573 | 2064.118 | 3027192.23 | 5666.203 | 6821.082 |

1/20/2011 | 10433 | 5876358 | 680.842 | 2836111.63 | 5263.116 | 6326.345 |

1/19/2011 | 87234 | 41535858 | 5374.047 | 3046261.51 | 5739.293 | 6913.39 |

1/18/2011 | 96581 | 43987076 | 6098.611 | 3132511.05 | 5925.458 | 7140.249 |

1/17/2011 | 130525 | 60127469 | 8485.532 | 3215868.31 | 6120.89 | 7377.581 |

1/16/2011 | 181206 | 86958845 | 11666.187 | 3227842.73 | 6168.627 | 7434.591 |

1/13/2011 | 166425 | 75519908 | 10633.668 | 3276320.22 | 6288.262 | 7575.888 |

1/12/2011 | 238201 | 123177139 | 16497.662 | 3296604.58 | 6380.79 | 7690.69 |

1/11/2011 | 116518 | 111019521 | 9771.417 | 3261083.65 | 6249.359 | 7512.094 |

1/10/2011 | 60350 | 30222420 | 4003.136 | 2877729.78 | 5420.118 | 6499.436 |