Introduction:

Now a days, education is not just limited to books and classrooms. In today’s world, education is the tool to understand the real world and apply knowledge for the betterment of the society as well as business. From education the theoretical knowledge is obtained from courses of study, which is only the half way of the subject matter. Practical knowledge has no alternative. The perfect coordination between theory and practice is of paramount importance in the context of the modern business world in order to resolve the dichotomy between these two areas. Therefore, an opportunity is offered by Daffodil international university, for its potential business graduates to get three months practical experience, which is known is as “Internship Program”. For the completion of this internship program, I was placed in a bank namely, “The BASIC Bank Limited”. Internship Program brings a student closer to the real life situation and thereby helps to launch a career with some prior experience.

ORIGIN OF THE REPORT:

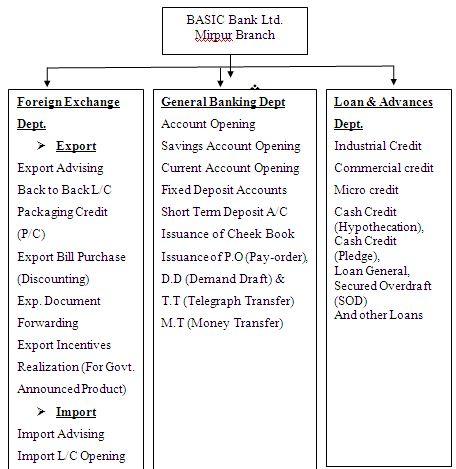

The title of the report is “Foreign Exchange operations of The BASIC Bank Limited” originated from the fulfillment of the BBA program under Daffodil international university. For the internship program, each student is attached with an organization. I have worked under the department of foreign exchange of BASIC Bank limited (Mirpur Branch) from 24th September, 2011 to 24th December 2011 and prepared this report under the supervision of Mr. Rafiqul Islam,

OBJECTIVES OF THE STUDY:

- To describe foreign exchange activities of Basic Bank Ltd,Mirpur Branch.

- To identify the problems related to Foreign Exchange activities of Basic Bank Ltd,Mirpur Branch .

- To make some recommendations to solve the problems.

Scope of the Report:

This report will cover Foreign Exchange Operations of BASIC Bank Limited. It will give a wide view of the different stages of foreign exchange operational procedure of BASIC Bank Limited, starting from the Import, Export and Remittance with total Foreign Exchange Procedures.

METHODOLOGY OF THE STUDY:

Nature of the study: The report is descriptive in nature. The report mainly describe the process that is followed by the BASIC Bank.

Data sources: There are two types of data used to prepare this report. They are primary sources of data and secondary sources of data. No structured questionnaire is used to prepare this report.

- a. Primary Sources of Data:

- Officers.

- Clients.

- Supervisors.

- b. Secondary Sources of Data:

- Annual Report of BASIC Bank Ltd;

- Periodicals published by the Bangladesh Bank;

- Different publications regarding foreign exchange operation;

- From Newspapers and Internet.

- Different Official Records of BASIC Bank Limited.

LIMITATIONS OF THE STUDY:

Despite all out co-ordination from the bank officials, I faced some limitations. The main problem I faced in preparing the paper was the inadequacy and lack of availability of required data. This report is an overall view of Foreign Exchange Operations of The BASIC Bank Ltd. But there is some limitation for preparing this report. These barriers, which hinder my work, are as follows:

- Difficulty in accessing latest data of internal operations.

- Another limitation of this report is Bank’s policy is not to disclose some data and information for obvious reason, which could be very much useful.

- Lack of confidential information regarding Import System.

- Lack of experience on preparing these types of report.

- Time constraints to prepare this report.

With all of this limitation I tried my best to make this report as best as possible. So readers are requested to consider these limitations while reading and justifying any part of my study.

Management:

Background of The BASIC Bank:

The BASIC Bank Limited (Bangladesh Small Industries & Commerce Limited) registered under the Companies Act 1913 on the 2nd of August 1988, started its operations from the 21st of January 1989. It is governed by the Banking Companies Act 1991. In 2001 the bank has changed its earlier name Bank of Small Industries and Commerce Bangladesh Limited and the changed name has been registered with the Register of Joint Stock Companies.

At the outset, the Bank started as a joint venture enterprise of the Bangladesh Credit Commerce (BCC) foundation with 70 percent shares and Government of Bangladesh (GOB) with the remaining 30 percent shares. The BCC Foundation being non functional following the closure of the BCCI, the Government of Bangladesh took over 100 percent ownership of the Bank on 4th June 1992. Thus the bank is state-owned. However, the Bank is not nationalized; it operates like a private bank as before. The bank was established as the policy makers of the country felt the urgency for a bank in the private sector for financing Small scale Industries (SSI).

BASIC is unique in its objectives. It is a blend of development and Commercial Banks. The memorandum and Articles of Association of the Band stipulate that 50% of loan able funds shall be invested in Small and Cottage industries Sector.

CAPITAL POSITION:

Authorized capital : Tk. 2,000 million

Paid up capital : Tk. 1964.65 million

Total Reserve and Surplus : Tk. 2509.78 million

The Bank is requested to transfer 20 percent of its net profit before tax to Capital Fund as per the Banking Companies Act 1991.

Mission, Vision, Objectives & Strategies of the Organization:

Organizational Goals and Objective:

BASIC Bank is unique in its objectives. It is blend of development and commercial banks. The Bank is entrusted with the responsibility of providing medium and long term loans and other financial assistance for promotion and development of small-scale industries.

- To employ funds for profitable purposes in various fields with special emphasis on small scale industries (SSI).

- To undertake project promotion on identify profitable areas of investment.

- To search for newer avenues for investment and develop new products to suit such needs.

- To establish linkage with other institutions those are engaged in financing micro enterprises.

- To cooperate and collaborate with institutions entrusted with the responsibility of promoting and aiding SSI sector.

Vision of BASIC Bank:

Provide the best banking services to all kinds of people and contribute for economic development of the country.

Mission of BASIC Bank:

To provide best development and commercial banking services to the common people of Bangladesh. And provide special support to the small scale business enterprises.

Corporate Strategy:

The corporate strategy of any organization plays a vital role on the company’s performance and lead to the way of being in growth prospect of the company. The corporate strategy of BASIC Bank is as follow-

- Financing establishment of small units of industries and business and facilitate their growth.

- Small Balance Sheet size composed of quality assets.

- Steady and sustainable growth.

- Investment in a cautious way

- Adaptation of new banking technology

product and services:

Foreign Exchange- its meaning and definition:

Foreign exchange refers to the process or mechanism by which the currency of one country is converted into the currency of another country. Foreign exchange is the means and methods by which rights to wealth in a country’s currency are converted into rights to wealth in another country’s currency. In banks when we talk of foreign exchange, we refer to the general mechanism by which a bank converts currency of one country into that of another. Foreign trade gives rise to foreign exchange. Modern banks facilitate trade and commerce by rendering valuable services to the business community. Apart from providing appropriate mechanism for making payments arising out of trade transactions, the banks gear the machinery of commerce, especially in case of international commerce, by acting as a useful link between the buyer and the seller, who are often too far away from and too unfamiliar with each other. According to foreign exchange regulation act 1947, “Anything that conveys the right to wealth in another country is foreign exchange”. Foreign exchange department plays significant roles through providing different services for the customers. Opening or issuing letters of credit is one or the important services provided by the banks.

Foreign Exchange :

Foreign Exchange means foreign currency and it includes any instrument drawn, accepted, made or issued under clause (13), Article 16 of the Bangladesh Bank Order, 1972. All deposits, credits and balances payable in any foreign currency and draft, travelers cheque, letter of credit and bill of exchange expressed or drawn in Bangladeshi currency but payable in any foreign currencies.

Bangladesh Bank issues Authorized Dealer (AD) license by observing the bank’s performance and also the customers associated with the bank for conducting foreign dealings.

Export Section:

Foreign Exchange Regulation Act, 1947 nobody can export by post and otherwise than by post any goods either directly or indirectly to any place outside Bangladesh, unless a declaration is furnished by the exporter to the collector of customs or to such other person as the Bangladesh Bank (BB) may specify in this behalf that foreign exchange representing the full export value of the goods has been or will be disposed of in a manner and within a period specified by BB.

Bangladesh exports a large quantity of goods and services to foreign households. Readymade textile garments (both knitted and woven), Jute, Jute-made products, frozen shrimps, tea are the main goods that Bangladeshi exporters exports to foreign countries. Garments sector is the largest sector that exports the lion share of the country’s export. Bangladesh exports most of its readymade garments products to U.S.A and European Community (EC) countries. Bangladesh exports about 40% of its readymade garments products to U.S.A. Most of the exporters who export BASIC Bank are readymade garment exporters. They open export L/Cs here to export their goods, which they open against the import L/Cs opened by their foreign importers.

SCRUTINY AND NEGOTIATION OF EXPORT BILL

Bank deals with documents not with goods. The bankers are to ascertain that the documents are strictly as per terms of L/C. Before negotiation of the export Bill the bankers are to scrutinize and examine each and every document’s with care. Negligence on that part of the bankers may result in non repatriation or delay in realization of export proceeds are incorrect documents may put the importers abroad into unnecessary troubles.

Export performance of Basic Bank Mirpur Branch for the Month of December–2011:

Total Export = FDBC + LDBC = TK.33, 061.10 million

| Year | 2007 | 2008 | 2009 | 2010 | 2011 |

| Volume(L) | 16,794.96 | 22,270.87 | 19,887.70 | 23,998.80 | 33,061.10 |

Import Section:

Imports are foreign goods and services purchased by consumers, firms & Governments in Bangladesh. To import, a person should be competent to be a ‘importer’. According to Import and Export Control Act, 1950, the Office Of Chief Controller Of Import and Export provides the registration (IRC) to the importer.

BASIC Bank checks the documents. The usual documents are:-

- Invoice

- Bill of lading

- Certificate of origin

- Packing list

- Weight list

- Shipping advice

- Non-negotiable copy of bill of lading

- Bill of exchange

- Pre-shipment inspection report

- Shipment certificate

Import Procedures:

- Registration with CCI&E

- For engaging in international trade, every trader must be first registered with the Chief Controller of Import and Export.

- By paying specified registration fees and submitting necessary papers to the CCI&E. the trader will get IRC (Import Registration Certificate).After obtaining IRC, the person is eligible to import.

- Now the importer has to contact with the seller outside the country to obtain the proforma invoice / indent which describes goods.

- Indent is got through indenters a local agent of the sellers.

- After the importer accept the preformed invoice, he makes a purchase contract with the exporter declaring the terms and conditions of the import.

- Import procedure differs with different means of payment. In most cases import payment is made by the documentary letter of credit (L/C) in our country.

- Purchase Contract between importers and exporter:

- Collection of LCA form:

Then the importer collects a Letter of Credit Authorization (LCA) form BASIC Bank, Shanti Nagar Branch.

- Opening a Letter of Credit (L/C)

In international environment, buyers and sellers are often unknown to each other. So seller always seek guarantee for the payment for his goods exported. Here is the role of bank. Bank gives export guarantee that it will pay for the goods on behalf of the buyer. This guarantee is called Letter of Credit. Thus the contract between importer and exporter is given a legal shape by the banker by its ‘Letter of Credit’.

- a. Parties to Letter of Credit:

- Importer ( Buyer)/ Applicant

- The issuing Bank (Opening Bank)

- The Advising Bank ( Notifying Bank)

- Exporter /Seller ( Beneficiary)

- Confirming Bank

- Negotiating Bank

- The paying/Reimbursing? Accepting/Remitting Bank

Letter of credit (L/C)

L/C is on instrument issued by a bank on behalf of one of its customers authorizing an individual or firm to draw drafts on the bank or one of its correspondents on its account under certain condition stipulated in the credit.

Parties of a Letter of Credit:

- Importer/ Buyer/ Applicant: This is the person who requests the opening bank to open L/C.

- Opening Bank/ Issuing Bank: The bank that opens/issues letter of credit on behalf of the applicant/importer.

- Advising Bank/ Notifying Bank: The bank through which the L/C is advised to the beneficiary (exporter).

- Exporter/ Seller/ Beneficiary: Beneficiary of the L/C is the party in whose favor the letter of credit is issued. Usually they are the seller or exporter.

- Confirming Bank: The bank, which under instruction in the letter of credit adds their irrevocable undertaking to that of the issuing bank. It is done at the request of the issuing bank having arrangement with them. The confirmation constitutes a definite undertaking on the part of confirming bank in addition to that of issuing bank.

- Negotiating Bank: The bank that negotiates document and pays the amount to the beneficiary when presented complying credit terms. If the negotiation of the documents is not restricted to a particular bank in the L/C, normally negotiating bank is the banker of the beneficiary.

- Reimbursing / Paying Bank: The bank nominated in the credit by the issuing bank to make payment against stipulated documents, complying with the credit terms. Normally issuing bank maintains account with the reimbursing bank.

- b. Application For L/C limit:

Before opening L/C, importer applies for L/C limit. To have an import L/C limit, an importer submits an application to the Department of BASIC Bank Limited furnishing the following information:

- Full particulars of bank account maintained with BASIC Bank Mirpur branch.

- Nature of business

- Required amount of limit

- Payment terms and conditions

- Goods to be imported

- Offered security

- Repayment schedule

A credit Officer scrutinizes this application and accordingly prepares a proposal (CLP) and forwards it to the Head Office Credit Committee (HOCC). The Committee, if satisfied, sanctions the limit and returns back to the branch. Thus the importer is entitled for the limit

- The L/C Application:

After getting the importer applies to the bank to open a letter of credit on behalf of him with required papers.

- Documentary Credit Application Form:

- BASIC Bank provides a printed form for opening of L/C to the importer. This form is known as Credit Application form. A special adhesive stamp is affixed on the form. While opening, the stamp is cancelled. Usually the importer expresses his desire to open the L/C quoting the amount of margin in percentage.

- Proforma Invoice: It states description of the goods including quantity, unit price etc.

- The insurance cover note: The name of issuing company and the insurance number are to be mentioned on it.

- The Letter of credit authorization (LCA) form: LCA form should be duly attested.

- The Form-IMP.

- Tax Information Certificate

- Forwarding for Pre-Shipment Inspection (PSI):

- Importer sends forwarding letter to exporter for Pre-Shipment Inspection. But all types of goods do not require PSI.

- Securitization of L/C Application:

The BASIC Bank Official scrutinizes the application in the following manner: –

- The terms and conditions of the L/C must be complied with UCPDC 500 and Exchange Control & Import Trade Regulation.

- Eligibility of the goods to be imported.

- The L/C must not be opened in favor of the importer.

- Radioactivity report in case of food item.

- Survey report or certificate in case of old machinery

- Carrying vessel is not of Israel or of Serbia- Montenegro

- Certificate declaring that the item is in operation not more than 5 years in case of car.

Examination of shipping documents:

One of the basic principles of documentary credit is that all parties deal with document and not with goods (Articles 6 of UCPDC-600). That is why the documents should be scrutinized properly. If any discrepancy in the documents is found, that is to be informed to the party. A checklist may be followed for examining the documents.

Import performance of Basic Bank for Mirpur Branch for the Month of December–2011:

Total Import = Cash L/C (sight) + Cash L/C (Usance) + Inland B/B L/C (sight) + Inland B/B L/C (Usance) + Foreign Inland B/B L/C (sight) + Foreign Inland B/B L/C (Usance) + L/C under AID/Loan + L/C under STA + Import from EPZ (Cash L/C) (sight) + Import from EPZ

Total Import = TK. 47,087.80 million.

| Year | 2007 | 2008 | 2009 | 2010 | 2011 |

| Volume(million) | 21,266.57 | 27,359.77 | 33,976.60 | 42,205.90 | 47,087.80 |

Foreign Remittance Section:

The basic function of this department are outward and inward remittance of foreign exchange from one country to another country. In the process of providing this remittance service, it sells and buys foreign currency. The conversion of one currency into another takes place at an agreed rate of exchange, in where the banker quotes, one for buying and another for selling. In such transactions the foreign currencies are like any other commodities offered for sales and purchase, the cost (convention value) being paid by the buyer in home currency, the legal tender.

Inward Foreign Remittance:

Inward remittance covers purchase of foreign currency in the form of foreign T.T., D.D, T.C. and bills etc. sent from abroad favoring a beneficiary in Bangladesh. Purchase of foreign exchange is to be reported to Exchange control Department of Bangladesh bank on Form-C

Outward Foreign Remittance:

Outward remittance covers sales of foreign currency through issuing foreign T.T. Drafts, Travelers Check etc. as well as sell of foreign exchange under L/C and against import bills retired. Sale of foreign exchange is reported to Exchange control Department of Bangladesh Bank on form T/M.

Foreign exchange means foreign currency and includes all deposits, credits and balances payable in foreign currency as well as foreign currency instruments such as Drafts, T.C.s, bill of exchange, and Letters of Credit Payable in any Foreign Currency. All foreign exchange transactions in Bangladesh are subject to exchange control regulation of Bangladesh Bank.

Identification of Documents Used in Foreign Exchange Banking:

The following Documents are used in Export:

- Bill of Exchange or Draft

- Bill of Lading

- Commercial Invoice

- Insurance Policy/Certificate

- Certificate of origin

- Inspection Certificate

- Packing List

- Courier Receipt

- EXP from

The following Documents are used in Import:

- Invoice

- Bill of lading

- Certificate of origin

- Packing list

- Weight list

- Shipping advice

- Non-negotiable copy of bill of lading

- Bill of lading

- Certificate of origin

The following documents are used in Foreign Remittance:

- Certificate of origin

- Remittance application

- ID card

Instruments of Inward & Outward Remittance:

- International money order (I.M.O)

- Cash

- Telegraphic Transfer (T.T)

- Mail transfer (M.T)

- Foreign Demand Draft (F.D.D)

- Payment order (P.O)

- Travelers cheque (T.C)

- Foreign Currency Notes.

Foreign Remittance Section performs the following function:

Selling

- Selling of foreign exchange to non-resident stock investor.

- Selling of Travel’s cheque to Bangladeshi travelers

- Selling of foreign currency to Bangladeshi for medical expense

Buying

- Buying of foreign currency from FC account of Bangladeshi individual as well as from exporters.

- Buying of international currency from foreigner and Bangladeshi

- Buying of cash foreign currency from foreigner and Bangladeshi

- Buying of foreign currency from non-resident investing in shares and stocks of Bangladesh.

Different Foreign Currency Account:

There are some accounts where customers can deposit and withdraw foreign currency-

- a. NFCD (Non- Resident Foreign Currency Deposit): Travelers or visitors who are traveling other countries may open it.

- FC (Foreign Currency) account: Exporters or importers for the purpose of their business may open it.

- RFCD (Resident Foreign Currency Deposit): Any person in a country who is working and staying in abroad can open it.

Remittance performance of Basic Bank for Mirpur Branch for the Month of December– 2011:

Total Remittance = Tk 22,897.88 milion

| Year | 2007 | 2008 | 2009 | 2010 | 2011 |

| Volume(M) | 17,456.78 | 19,487.59 | 21,678.08 | 25,457.04 | 22,897.88 |

Findings:

In recent years, the foreign exchange business of BASIC Bank ltd is increasing at a faster rate. As a state owned scheduled bank, BASIC Bank Ltd is playing an important role toward the growth and economic development of Bangladesh. BASIC bank is rendering a stable support to the national foreign exchanges business. Although the foreign exchange business is increasing day by day there are also some obstacles around it which are as follows:

- One problem relates to technology, the bank must try to adopt new technologies. Otherwise the profitability of the bank may hamper.

- To meet the challenges in the banking industry and to help employees to adapt to the changes and new working condition, training is essential but no such training center has yet been established in BASIC Bank. Moreover, training given to employees is not adequate.

- Besides, SWIFT is being used in some branches and the head office of the bank for trade finance related operations like documentary credit, documentary collections, fund transfer, guarantee, etc. with optimum security, but not in all branches.

- The officers are very helpful to the business men. Some of our business men do not know exactly the procedures of opening L/C. the officers of BASIC bank help them properly to execute their business.

- To make the process easy, bank should give emphasis to use the modern communication media like e-mail, fax, internet etc.

- Modern technical equipment like computer, ups, modem etc. is not sufficient in foreign exchange department, which results in the delay of exchange process.

- The data base system of foreign exchange department is not very systematic. Also documentation and filing process of foreign exchange operation is not user friendly, which sometimes wastes valuable time.

- Letter of credit (L/C) opening system for the importer is easy. it consumes time and money as well.

RECOMMENDATIONS:

I had the practical exposure in BASIC Bank Ltd. for just twelve weeks, with my little experience in the bank in comparison with vast and complex banking system, it is very difficult for me to recommend. We have observed some shortcomings regarding operational and other aspects of their banking. On the basis of my observation we would like to recommend the followings :

- The branch need to set up well designed IT section by using more updated technology and information.

- Adequate on the job training is required for the newly employed personnel.

- SWIFT service should be introduced in each and every branch of the bank, which will help to smoothen the foreign exchange operations of the bank.

- Some officers of the bank are not self motivated. They should be self- motivated by training.

- The bank should do more advertisement for attracting new customers.

- Bank needs sufficient computer, ups, modem etc for foreign exchange department.

- The bank should develop an effective database system to analyze the data of foreign exchange business.

- Bank should provide emphasis to make the documentation and filing process of foreign exchange operation user friendly.

- Letter of credit L/C opening system for the exporter should be easier.

I think the Management should employ at least few more employee in foreign trade department as I have seen from my practical experience that many customers wait for a long time for any service as they see that only one concerned official is doing their best to meet the requirements of the customers.

CONCLUSION:

BASIC Bank Ltd. is committed to Boost up export, reduce import, raising of Gross Domestic Product (GDP) and increase employment.

All the branches of BASIC Bank Limited are authorized dealer of Foreign Exchange Business. The authorized dealer motivates the importer to import Raw materials, Fabrics, Frozen fish, jute items, and electronics goods, Accessories, Chemicals, and Vegetable Fat etc.

The import or exports are motivated by the BASIC Bank Limited to the foreign exchange business, particularly to open the letter of credit. A letter of credit offer advantages both to the importer and exporter. The advantages accruing to either of the parties differ depending upon the nature of credit opened. There are certain Common benefits accruing from the use of credit as under.

BASIC Bank Limited is playing a vital role in financing import and exports of the country. Without Bank’s co-operation, it is not possible to run any business or production activity in this age. Exports and import need finance in various stages of their activities. Export and import financing are letter of credit (L/C), payment against documents (PAD), loan against imported merchandise (LIM) etc. All these facilities are being provided by BASIC Bank Limited. For this purpose Bank considers the borrower’s business standing, integrity, liability with the bank and term and conditions of the L/C. There is lot of risks involved in foreign exchange business. So, the Basic Bank Limited has to clearly serve the customers from a neutral point and gather the current information about the market.