Executive Summary

The report is made on analysis of accounting & a financial activity of Gurba Engineering Limited Which is one of the famous Engineering Company in Bangladesh. Guraba Engineering Limited established in 2002. Guraba Engineering Limited is one of the leading business organizations in Bangladesh.

Guraba Engineering Limited maintains their accounting activities by internet based softer. The main accounting activities of Guraba Engineering Limited are making voucher, Daily receipt & payment statement, Trial Balance Journal Book, Bank Book, Cash Book, Account Reconciliation, Depreciation, Schedule, Income Statement, Balance Sheet, Notes to the account.

Strategies used by Guraba Engineering Limited for its products are appropriate. For this several statistical tools are used for financial analysis like Horizontal Analysis, Vertical Analysis. The results are shown through graphs and charts. In assessing the financial condition of Guraba Engineering Limited, ratio analyses have been done and graphs and charts are given to show the results.

The major findings of this about accounting section are Guraba Engineering Limited use internet based software which is one of the latest accounting software which is one of the latest accounting software. Because of this software, activities are run more quickly the previous , factory does not start to use the software till the costing budget & production budget are usually made for six month, etc. After financial analysis it is clear that the company is moving positive through their financial condition and now they are highly liquid company and also can meet their current claims easily.

Guraba Engineering Limited has been registered as a limited company guarantee in of Joint Stock Companies on 18th February 2009. With a view to establish, maintain, conduct a Company for the trading, manufacturing, servicing of directors of the company, their clients and buyer with all the usual privileges, advantages and the solution of electro-mechanical products and services of telecom, factory, manufacturer, developer, financial institute and trading Company as well. Company share (Limited by person) holder are selected in every Annual General Meeting named the Board of Directors consisting of one Chairman and 2 (two) share holder for looking after the day to day affairs in department of the Company and to manage its movable and immovable property with operational activity. The Board of Director is empowered to frame the manual of procedure, financial and administrative rules and manual of purchase whenever is needed for smooth functions of the Company. One Share holder-in-Charge of Administration and one share holder-in-Charge of Finance are assigned by the Chairman from amongst the Board of Director directors as per the Company constitution alongside all other directors of the Board of Director who are also assigned with different portfolios by the Chairman to look after the day to day affairs of various departments of the Company. The monthly subscriptions of the directors are prescribed in the Articles and Associations of the Company, which is widely known as its Constitution, and other charges are fixed from time to time by the Board of Director. The Board of Director is authorized to spend up to the amount mentioned in the Articles of Association.

Introduction

In this competitive world practical experience is must which is not possible only by gathering the theoretical knowledge. For a BBA student, internship is the way to test skills in the work force. The report is made for fulfil the requirement of BBA program which is an indispensable part of this program that bridge the gap between academic and practice. The report is made on accounting and financial activities of Guraba Engineering Limited, which is one of the famous engineering companies in Bangladesh. Guraba Engineering Limited established in 2002. Guraba offer various types of product or service. Such as All types of distribution transformer, AVP, Online UPS, Rectifier, Circuit breaker, capacitor, PFC Relay, All kind of protection product. Financial and Development of employees is superseding importing to continued success of any organization. Financial is a learning process, which seeks relatively permanent change in an individual that will improve the ability to perform on the job. Financial involves the change of knowledge, skills, and attitude or behaviour.

Objectives of the Study

- To know about the Financial Mechanism of Guraba Engineering Limited

- To know about the Accounting Activities of Guraba Engineering Limited

- To know about the Budget and Budgetary Control of Guraba Engineering Limited

- To identify the problems of Financial and Accounting Activities of Guraba Engineering Limited

- To give some recommendations to solve the problems of Guraba Engineering Limited

Scope of the Study

This report is based on secondary data which were disclosed to the public by the company through annual report. The will attempt to covers the whole accounting and Financial activities of Guraba Engineering Limited. The purpose of the report to know the Financial and Accounting system of Guraba Engineering Limited. The environment of the organization is suitable to study and analyze. Here to be service properly and maintain whole life.

Methodology of the Study

The discussion paper contains data from both primary and secondary sources.

Primary data collection

Methods used for primary data collection;

i Physical interviews and informal discussion

ii Face to face discussion

iii Practical work

Secondary data collection

i. Finance and Accounting manual

ii. Annual Report

iii. Prospectus

Though pre-testing of the developed draft questionnaires in the field was the usual practise in order to test the validity of it in respect of objectives of the study. But due to time budget constraints pre-testing of the questionnaires could not be done and accordingly the draft questionnaires were finalized for data collection from the primary sources.

Limitations of the Study

The study was carried out engaging all available resources with sincerity, honesty integrity and the achieved knowledge on the research methodology. In spite of all out efforts the following limitations might affect up to some extent the degree of accuracy and generalization of the result of the study.

i This study has been conducted within a limited time. So, time constraint has played a key role for the whole study

ii Unpublished data have not considered for Lack of cooperation of the respondents.

iii I faced technological problem.

iv This report is based on solely company published data.

v Some data cannot be exposed because of privacy of the company.

vi Knowledge limitation also makes some shortcoming.

Infrastructure of Guraba Engineering Limited

We have a well equipped infrastructure that assists us in delivering the best possible product. We use modern machineries and techniques in the manufacturing process. Machineries like Electrometer EMC 80 D, Essex fort way high accuracy and Techno-max high accuracy coil winding machine is used for the manufacturing process. We are also equipped with 7 Digital meters, 7 Hi Voltage probes, etc. for the quality testing.

Mission of Guraba Engineering Limited

To materialize this vision we have undertaken a mission. Mission is-

i To profitably meet the needs of our present and prospective customer.

ii To get recognized as a candid reliable supplier.

iii To focus on our customer satisfaction by our prompt customer service.

iv To discover new business opportunities to become a world class organization.

Vision of Guraba Engineering Limited

We have set a clear vision for our company which is directing us to our definite goal of success. Our vision is to become the market leader and develop a brand image by creating a new model of excellence in the power and energy sector within 2020.

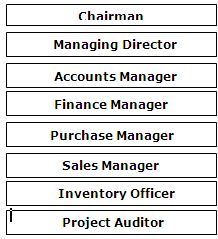

Structure of Management

Research Gap

The previous studies have made substantial contributions to the understanding to different aspects of Company, but till today on research work has been done on the Assessment of Financial and Accounting Activities of Engineering Companies: A Case Study of Guraba Engineering Limited.

It is also observe that current professional researcher emphasizes on the label of financial performance accounting activities of Guraba Engineering Limited. But on such researcher work has been under taken from financial performance to highlight the gap in the level of activities.

From the forgoing studies it may be concluded that no specific and on in depth research has so far been conducted on financial performance accounting activities of engineering company of Bangladesh.

Core Activities of Finance and Accounts

The Accounts Section is the vital part of the Organization that manages and control the entire financial and account keeping matters. This section shall be directly controlled by the Director-in-Charge of Finance who will have a Sub-committee duly approved by the Chairman. The responsibility of the section is to maintain the books of accounts of the Company and maintain the Banking accounts and their reconciliation statements and Accounts, Billings, Serving Monthly Bills to the Directors, Fixation & Disbursement of Salaries to employees, Management of Contributory Provident Fund, Payment & Disbursement of bills, Record of Income & Expenditures, Statement of Annual Accounts, Arranging Internal & External Audit, Supervision of Store including its Accounts etc.

Preparation of Daily Cash & Bank Balance Statement

Daily cash & bank balance statement usually contains the following data & information:

i Bank account balance of different banks;

ii Cash in hand;

iii Advance slip (IOU-Temporary Loan) balance (If any);

Prepared by cashier and will be checked by accounts personnel & authenticated by Director-In-Charge (Financial) through signing this statement at the end of the day as per format.

Passing Adjusting Journal and Closing Entries

i Adjustment entries for stores, advances, prepayments, outstanding expenses, deferred service charges, accrued income, receivables and depreciation shall be made at the end of each month / quarter / half year (as and when required) through journal vouchers.

ii All rectifications, transfers and adjustments and non-cash transactions are to be processed through journal voucher.

iii The adjusting journals will be prepared by the Assistant Manager Finance (AMF), duly checked by Finance Manger (FM), certified by the departmental manager and approved by Finance Director The journal vouchers will be filled in a chronological order.

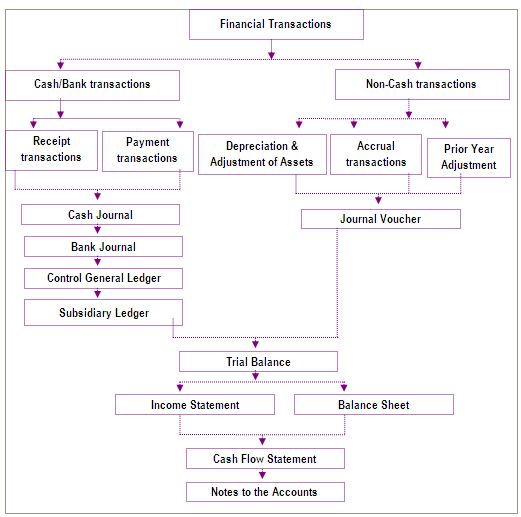

Preparation of Financial Statement

Preparation of Trial Balance

A trial balance should be prepared periodically (preferably monthly) from the general ledger. A trial balance is a listing of all general ledger accounts and their balances as of a particular date. The trial balance will verify that the general ledger accounts balance (debits equal credits) and serves as a work paper to make adjustments to any accounts to correct their balances.

Preparation of the Financial Statements

Accounts section of the Company is responsible for preparing financial statements. In preparing various Financial Statements, accounts section is allowed to take help from any other section of the Company. Accounts Section will prepare following Financial Statements:

i. Balance Sheet (Department wise & consolidated)

ii. Statement of Income and Expenditure (Department wise & consolidated)

iii. Cash Flow Statement

iv. Statement of Changes in equity

v. Notes to the Financial Statements.

This section prepares any other statements and reports required by management or any other legal authorities. A brief description of steps in preparation of financial statements has been states as under

An overview of Financial Statements

The components of required Financial Statements are briefly discussed below:

Balance Sheet: Balance sheet refers to such a statement, which portrays the financial position of Company i.e. the assets and liabilities of the Company on a specific point of time (such as 30th September each year)

Statement of Income and Expenditure: Statement of income and expenditure shows the financial results of the organization of an accounting period. It shows either excess/shortage of income over expenditure incurred for the accounting period.

Cash Flow Statement: This statement will show inflow and outflow of cash of the Company during the year and ending cash position as on last date of the year by grouping all activities of the organization into operating, financing and investing activities. Cash flow statement may be prepared by following either direct or indirect method.

Notes to the Financial Statements: Financial Statements discussed above provide information in abstract form. Additional information will be provided though notes to the financial statements for providing true and fair view of the financial information. A note to the Financial Statements provides narrative description of the amount shown in the face of the Balance sheet and Statement of Income and Expenditure.

Total Asset

Chart

| Year | 2010 | 2011 | 2012 |

| Total Asset (Tk.) | 17811564 | 35170558 | 25951929 |

Net Working Capital

Chart

| Year | 2010 | 2011 | 2012 |

| Net Working Capital(TK) | 8763643 | 13819782 | 9523345 |

Income

Chart

| Year | 2010 | 2011 | 2012 |

| Income(TK.) | 5518189 | 6719994 | 360325 |

Purpose of Financial Statement

The objective of financial statement is to provide information about the financial position, performance and changes in financial position of an enterprise that is useful to a wide range of users in making economic decision. Financial statements should be understandable, relevant, related to an organization’s financial position. Financial statement are intended to be understandable by readers who have “a reasonable knowledge of business and economic activities and who are willing to study the information diligently. Financial statements may be used by users for different purposes. Owners and managers require financial statements to make important business decisions that affect its continue operations. Financial analysis is then performed on these statements to provide management with a more detailed understanding of the figures. These statements are also used as part of management annual report to the stockholders. Employees also need these reports in making collective bargaining agreements (CBA) with the management, in the case of labor union or for individuals in discussing their compensation, promotion and rankings. Prospective investors make of financial statements to assess the viability of investing in a business. Financial analysis are often by professionals (financial analysis), thus providing them the basis for making investment decisions. Financial institutions (bank and other lending companies) use them to decide whether to grant a company with fresh working capital or extend debt securities (such as a long-term bank loan or debentures) to finance expansion and other significant expenditures. Government entities (tax authorities) need financial statement to ascertain the propriety and accuracy of taxes and other duties declared and paid by a company. Vendors who extend credit to a business require financial statement to assess the creditworthiness of the business. Media and the general public are also interested in financial statement for a variety of reasons.

Stages of Financial Analysis

Different states of Financial Statement analysis

Stage-1. Acquiring the company’s financial statements for several years as a minimum getting the following statements, for at least 3 to 5 years.

i. Balance sheets

ii. Income Statements

iii. Shareholders equity statements

iv. Cash flow statements

Stage2. Quickly scan all of the statements to look for large movements in specific items from one year to the next.

Stage3. Reviewing the notes accompanying the financial statement for additional information that may be significant for analysis.

Stage4. Examining the balance sheet. Look for large changes in the overall components of the company’s assets, liabilities or equity.

Stage5. Examine the income statement. Look for trends over time. Calculate and graph the growth of the following entries over the past several years. Revenues (sales), Net income (profit, earnings)

Stage6. Examine the shareholder’s equity statements. Has the company issued new shares, or bought some back? Has retained earning account been growing or shrinking? Why? Are there signals about the company’s long term strategy here?

Stage7. Examine the cash flow statement, which gives information about the cash inflows and outflows from operations, financing, and investing.

Stage8. Calculate financial ratios in each of the following categories, for each year.

Ratio Analysis

This is the method in which the ratio between two or more variables related to the business is compared. There are many ratios used to analyze financial statements

Current Ratio

| S.R. | Ratio | Calculation | Year 2010 | Year 2011 | Year 201 |

| 1 | Current Ratio | Current Asset/Current Liabilities (32799926/18980144),(16575207/7812564), (22234602/9832644) | 2.12 | 1.73 | 2.26 |

This ratio is concern to measure of a firm’s ability to meet its current liabilities. The current ratio provides the best single indicator of the extent to which the claims of short term creditors are covered by assets that are expected to be converted to cash fairly, quickly, it is the most commonly used measure of short term solvency. The higher this ratio, the greater short-term solvency. The above ratio indicates that (Guraba Engineering Limited.) has the capability to meet its short term obligations. It is encountered that, in year 2010; the current ration was higher than the current year 2011. On the one hand, its liquidity position is relatively weak to the previous year. On the other hand, a high current ratio could mean that the company has a lot of money tied up in non-productive asset such as excess cash or marketable securities or in inventory. So, it is concentrated that the inventory or cash was tied up as a non-productive frame of mind in year 2010.

Management, or Turnover, Measures

| S.R. | Ratio | Calculation | Year 2010 | Year 2011 | Year 2012 |

| 3 | Inventory Turn Over | (Cost of Goods Sold)/Inventory (42378857/12834415),(3184925/8248617), (11311100/7055493), | 0.39 | 3.30 | 1.60 |

Inventory Turnover: A high inventory turnover is often regarded as the signal of efficient management. This ratio indicates that how fast we can sell product. As a rough approximation, each item of “Guraba Engineering Limited” inventory is sold out and restocked or turnover 3.30 times in year 2011 and 0.39 times in year 2010. The above ratio is lustrated that the Inventory turnover gradually increasing by the year. Excess inventory is, of course unproductive, and it represents an investment with a low or zero rate of return. Low inventory turnover ratio also makes us question the current ratio. With such a low turnover, we must wonder whether the firm is actually holding damaged or obsolete goods not worth their stated value.

Receivables Turn Over and Days’ Sales in Receivables

| S.R. | Ratio | Calculation | Year 2011 | Year 2010 |

| 6 | Receivables Turnover | Sales/Accounts Receivable (72381017/16148855),(7675896/3451258) | 4.48 | 2.22 |

This ratio indicates that how fast we collect those sales. It is for guidance that the higher accounts receivable turnover, the greater the efficiency of credit management. The above ratio shows that in year 2011 the accounts receivable is 4.48 times and it is higher than the last year 2010 by 2.22 times. Nevertheless, the ‘Guraba Engineering Limited’ has the very poor efficient of credit collection management. So, it should be improved the credit collection policy.

| S.R. | Ratio | Calculation | Year 2011 | Year 2010 |

| 7 | Days’ sales in receivables | 365 days/ Receivable Turnover (365/4.48),(365/2.22) | 81 Days | 164 Days |

This ratio represents the average length of time that firm must wait after making sales before receiving cash or the average collection period. The “Guraba Engineering Limited” has 81 days sales outstanding for the year 2011 and 164 days for the year 2010.

We could say that we have 80 days worth of sales currently uncollected. The outstanding indicates that customers, on the average, are not paying their bills on time. This deprives Guraba Engineering Limited of funds which it could use to reduce debt or invest in productive assetsTherefore, if the trend in DSO (Days Sales Outstanding) is up, but the credit policy has not been changed, this would be strong evidence that steps should be taken to expedite the collection of accounts receivable.

Asset Turnover Ratio

| S.R. | Ratio | Calculation | Year 2010 | Year 2011 | Year 2012 |

| 8 | Total Asset turnover | Sales/Total Assets (72381017/35170558),(7675896/17811564), (44807834/25961929) | 0.43 | 3.30 | 1.73 |

The total assets turnover ratio measures the turnover of all the firm’s assets. This ratio measure how efficiently assets are employed overall. If we compare to the current ratio in 2011 with the last year 2010; the ratio indicates that the Guraba Engineering Limited is generating a sufficient value of business given its total asset investment. Sales should be increased, some asset should be disposed of or a combination of this step should be taken.

Horizontal Analysis

With the help of horizontal financial analysis, one can compare a business entity over different month or defined period within a fiscal year. For example, revenue generated over different months of can be compared to analyze the overall performance of business or a particular project. An accountant can follow one tow the given below methods to conduct a horizontal financial analysis. Dollar analysis is the first way method of horizontal financial in which the amounts in absolute of various items are compared for and entity over different periods of time. This type of analysis helps analyze the spending trend of a business. Besides, it also helps analyze the effects of external factors like rise in prices over business expenditures. Percentage analysis is based on the change in different items over different period of time calculated in terms of percentage. With the help of this type of analysis, the performance of a small business can be compared to that of a large business in the same industry.

Vertical Analysis

This involves the procedures of comparing different figures of separate entities to one specific figure of entity for one specific period of time. This type of analysis is of at significance in carrying out the decision making process. An also accountant can also expand the vertical analysis by comparing the figures of one specific period with those of another period. Analysis of the balance sheet is one good example of carrying out vertical financial analysis each item of the balance sheet can be compared to the total assets calculated. Vertical analysis is useful for answering the question related to business liabilities and equity. This type of analysis is also to as common-size analysis.

Accounting Policies & Procedure

The Accounts Section of the Company is responsible for conducting accounting and financial activities. This Section should be maintained and ensure the accounting policies & procedure. Accounts related vouchers, books and records are kept in this section. Preparation of Financial Statements is primary duty of this section. Director is the head of this department and Manager Finance & Accounts is the head of this section. There is a proper segregation of duties exists in this section i.e. cash section. Director billing, general accounts, store maintenance and fixed assets maintenance section are separated from account section. Accounting and financial activities are those activities, which are done for preparation of financial statements to ensure accountability, to safeguard the financial interest of the Company, to bring transparency and helping the management in the decision making process.

These activities consist of the following

i. Recording Transaction

ii. Maintenance of Books and records.

iii. Maintenance of Cash

iv. Maintenance of Bank accounts

v. Maintenance of Stock

vi. Maintenance of Fixed Asset

vii. Preparation of Financial Statements

- Preparation of budget and

ix. Variance Analysis

Basis of Accounting

Accounts of Guraba Engineering Limited should be maintained on acceptable basis, that is, all income actually received are to be considered as income and all expenditure / payments, actually made are to be taken as expenditure, with a few book adjustments for stock & stores, advances, prepayments, outstanding expenses, depreciation, deferred income, accrued income, receivables, etc.

As such accrual basis of accounting is being pursued. The Company shall apply, adopt, follow and implement the guidelines / instructions of the International Accounting Standards (IAS) for all purposes of accounting.

Accounting Responsibility

Finance & Accounts Department is entrusted with the responsibility to ensure the proper maintenance of the books of accounts of the Company. Timely and accurate presentation of the financial reports is the prime job of the accounts personnel in Guraba Engineering Limited Director-In-Charge. The Finance & Accounts Department will ensure the authenticity & recording for all payments and also responsible for recording of all receipts on time. It supervises the effective implementation of the internal control devices & assists the management in attaining financial management. Chief Financial Officer (Director) is responsible to preserve all books of accounts & supporting accounting records in a systematic and dynamic manner. Management will make job / duty allocations to the staff Directors of finance / accounts Department & ensure smooth function of his department. As a measure of management safe-guard, the required coverage and appropriate precautions must be exercised for handling of cash, handling of store materials, carrying of cash from and to bank and preservation of cheque books and overall financial discipline of Guraba Engineering Limited. Any staff Director of Guraba Engineering Limited who signs or countersigns in any primary documents, books of original entries, books of final entries and reporting etc. is personally, officially and professionally responsible for their completeness, correctness & for the facts as stated there-in so far as it is his / her duty to know or to extent to which he / she may be responsible or expected to be aware of them.

Accounting Policies of the Guraba Engineering Ltd.

Accounting system, selection and application of accounting policies and presentation of financial statements of Guraba Engineering Limited shall be in conformity with the international accounting standards. Accounting policies of Guraba Engineering Limited encompass the principles, bases, conventions, rules and procedures adapted by Guraba Engineering Limited management in preparing and presenting financial statements by using best management judgment in the circumstances. Guraba Engineering Limited shall use its judgment in selecting and applying its accounting policies keeping in view the following:

i The requirements and guidelines in Bangladesh Financial Reporting Standard (BFRS) dealing with similar and related issues;

ii The definitions, recognitions and measurement criteria for assets, liabilities, incomes and expenses set out in the International Accounting Standards Committee (IASC) framework for the principal and

iii Pronouncements of other standards setting bodies and accepted policies, but only to the extent, that these are consistent with the above.

Four considerations shall govern the selection and application of the appropriate accounting policies and the preparation of the financial statements of Guraba Engineering Limited.

Taxation

A Income Tax

i At present, Guraba Engineering Limited has been entitled to tax exempted from Income Tax as per SRO No. 298-Law/2000 as Company Law.

ii Guraba Engineering Limited has been completed the assessment activities in favour of foreigners but income tax shall be paid by the foreigners as per their agreement. If foreigner’s (if Guraba Engineering Limited hiring foreign staff) income tax paid by Guraba Engineering Limited then it shall be approved by Board of directors/ Working Committee.

iii Guraba Engineering Limited should be deducted the Income tax at source and deposited in Government Treasury in due time as per Income Tax Ordinance-1984.

B. Value added tax (VAT)

i Guraba Engineering Limited shall pay the VAT with maintaining a current account on their revenue as Sports Organization Institute, SRO-047 as per VAT Act. – 1991.

ii Guraba Engineering Limited shall deduct the VAT at source and deposited in Government Treasury in due time as per Value Added Tax (VAT) Act. 1991.

iii Capital fund is restricted to be exclusively used for the purpose of Guraba Engineering Limited only.

Flow Chart of Financial Accounting

Maintained Books of Accounting

In general, the following accounting forms and recording books could possibly be kept and maintained by Guraba Engineering Limited. These accounting forms and recording books would be used for documentation of various records, analysis and interpretation of daily financial transactions of Guraba Engineering Limited in terms of cash and accrual basis. Utilities and characteristics of different forms and recording books are described here in details for smooth functioning of processing the everyday financial transactions of Guraba Engineering Limited Management Office and its Unit Offices in systematically.

Cash Journal – Debit / Payment Voucher

Voucher is the primary source of information to the accounting process. Vouchers are prepared on the basis of invoice or memorandum that serves as evidence and appropriateness of a financial transaction. As soon as cash payment transaction is completed, it has to be documented with valid, authentic and authorized payment evidences as proof of appropriateness of expenditure and then, to be recorded in Cash Journal – Debit / Bank Voucher. To record the cash transactions, it is the primary and main evidence of processing transactions of Guraba Engineering Limited Board of directors.

Debit – Cash Journal

In case of cash expenses or payments or discharging of liabilities, it has to be recorded through Debit – Cash Journal. Debit / Bank vouchers shall be submitted for approval to the competent authority together with all supporting documents. Only duly approved and authorized vouchers can be posted to the books of accounts.

Cash Journal – Credit / Receipts

As soon as cash receipt or income transaction is completed, it has to be recorded in Cash Journal – Credit / Receipt Voucher. To record the cash receipt transactions, it is the primary and main evidence of processing transactions of Guraba Engineering Limited Board of directors.

Credit – Cash Journal

In case of cash receipts or incomes, it has to be recorded through Credit – Cash Journal. Credit / Receipts vouchers shall be submitted for approval together with all supporting documents. Only duly approved vouchers can be posted to the books of accounts.

Bank Journal – Debit / Payment Voucher

Voucher is the primary source of information to the accounting process. Vouchers are prepared on the basis of invoice or memorandum that serves as evidence and appropriateness of a financial transaction. As soon as bank payment transaction is completed, it has to be documented with valid, authentic and authorized payment evidences as proof of appropriateness of expenditure and then, to be recorded in Bank Journal – Debit / Payment Voucher. To record the bank transactions, it is the primary and main evidence of processing transactions of Guraba Engineering Limited Board of directors.

Debit – Bank Journal

In case of bank expenses or payments or discharging of liabilities, it has to be recorded through Debit – Bank Journal. Debit / Payment vouchers shall be submitted for approval to the competent authority together with all supporting documents. The voucher should be authorized through Expenditure Note Sheet, which will be mentioned the description of the nature of expenditure, VAT at source and TDS amount and shown the option of authorized personnel. Only duly approved and authorized vouchers can be posted to the books of accounts.

Vouchers Maintenance of Voucher

Voucher is the primary document for recording any transactions. These are the written authorization in a specific format prepared by the accountant and approved by the appropriate authority that is used before a transaction is recorded in the books. Voucher is prepared on the basis of supporting documents. The vouchers are pre-numbered and printed. No voucher will be entered in the ledger and Cash/Bank book before approval by the proper authority.

Types of Vouchers

Three types of vouchers are required in Guraba Engineering Limited. These are as follows:

i Debit voucher/payment voucher

ii Credit voucher/receipt voucher

iii Journal voucher

The formats of these vouchers are to be printed in different colour pages or to be printed from computer software.

Debit Voucher/Payment Voucher: Debit voucher is required to be prepared for every payment made. It is prepared for recording revenue & capital expenditure such as staff salary, travelling & transportation, etc. and plant & machinery, furniture & fixtures, etc. Necessary supporting documents should be attached with vouchers.

Credit Voucher: Credit/receipt voucher is required to be maintained to authorize record of money received in the books of accounts. Amount received from Company Directors, debtors, amounts received by means of sale, transfer or any other means is recorded in the books of accounts through credit vouchers. Before approving this voucher, it is important to ensure that all-necessary supporting documents are attached with it.

Journal Voucher: Transactions other than cash are generally recorded in the books of accounts through journal vouchers. Besides this adjusting entries and transfer entries, etc. is also recorded through journal vouchers. Necessary supporting documents are to be attached with this voucher before its approval.

Rules Regarding Preparation of Vouchers

i Voucher should be pre numbered, sequentially maintained. Blank vouchers should be under lock & key with DF.

ii All will check required support documents, e.g. purchase requisition, purchase order, receiving report and vendor bill/invoice and will prepare the payment voucher.

iii All the relevant documents in support of the payment must be attached to the payment voucher.

iv All supporting documentation should be signed by the DF indicating proper verification.

v All supporting documents attached to the payment voucher must be cancelled to prevent reuse by stamping each item “Paid” and the payment voucher number will be written on each of the supporting document.

vi Vouchers will be signed by as follows:

- AE as prepared by

- DF as checked by

- Concern Director-in-Charge as Recommended by

- The Secretary and Chairman/Director-Finance as Approved by.

vii All payments must be made after getting signature of above persons.

viii The amount to be paid through payment voucher should be written in word on the face of the voucher.

Approval of Journal Vouchers

The DF for completeness and coding/posting to the correct account should authorize all journal vouchers for entries into the general ledger.

Bank Journal – Credit / Receipts

As soon as bank receipt or income transaction is completed, it has to be recorded in Bank Journal – Credit / Receipt Voucher. To record the bank receipt transactions, it is the primary and main evidence of processing transactions of Guraba Engineering Limited Board of directors.

Credit – Bank Journal

In case of bank receipts or incomes, it has to be recorded through Credit – Bank Journal. Credit / Receipts vouchers shall be submitted for approval together with all supporting documents. Only duly approved vouchers can be posted to the books of accounts.

Journal Voucher – For Adjustments / Non Cash Transactions

Journal vouchers need to be prepared in order to reconcile different combinations of inter related accounts. Besides, transactions of some non-cash items will also be made through the preparation of Journal Voucher.

Preparation of journal voucher is generally necessary to record the posting of all financial transactions that are generally categorized as below:

i Depreciation of all fixed assets;

ii Provision created for the capital expenditures;

iii Provision created for the revenue expenditures;

iv All sorts of adjustment in inventory accounting;

v All sorts of adjustment of advances;

vi All sorts of income receivables;

vii Deferred service charges

viii Provision created for the bad debts;

ix To accounts for all sorts of accrued liabilities;

x Accounting of deduction of security deposit, Income Tax, & VAT

xi All sorts of rectification entries for appropriate corrections;

xii Other transactions not covered by any other vouchers.

Journal vouchers shall be submitted for verification to the Manager Finance (FM) and then for approval to the CFO, together with all supporting documents. Only duly approved and authorized journal vouchers can be posted to the books of accounts.

Cash Journal Register

Guraba Engineering Limited Account Department shall maintain Cash Journal Register. All cash transactions will be recorded in the cash journal register strictly on daily basis in computer. Cash debit journal will be recorded on the expenditure / payments side and cash credit journal will be recorded on the receipt side of the cash journal register strictly chronologically. Cash journal register must be balanced after daily operations are being completed. After balancing the cash journal, the balance amount will be physically verified and there after both accounts officer and cashier will put their signatures acknowledging the above balance as found correct. Thus, it is the primary and main book of the Guraba Engineering Limited that will give an accurate picture of the cash item transactions in a particular time.

Bank Journal Register

Guraba Engineering Limited account Department shall maintain Bank Journal Register. All Bank transactions will be recorded in the bank journal register strictly on daily basis in respective Bank name wise in separate page in the Bank Journal Register in computer.

Bank debit / Payment journal will be recorded on the expenditure / payments side and Bank credit journal will be recorded on the receipt side of the Bank journal register strictly chronologically. Bank journal register must be balanced in respective bank name wise at the end of the month. After balancing the Bank journal register, the respective bank account will be reconciled with Bank statement.

Control General Ledger

The control general ledger is the control book to summarize all financial transactions (cash items and non-cash items transactions) of Guraba Engineering Limited in accounts head and accounts code wise for easy preparation of financial statements. Recording of all the daily income and expenses transactions will be made in the control general ledger through computer. All transactions in cash journal register and through journal vouchers will have to be recorded in control general ledger under different accounting heads and codes.

General Ledger Activity

All valid general ledger entries and only those entries should be accurately recorded in the general ledger. The general ledger consists of control accounts for accounts in the company’s chart of accounts. These accounts are listed in the general ledger in numerical order with the account title. The general ledger should be maintained in computerized accounting system.

Posting to General Ledger

i At least monthly all activity should be posted to the general ledger. The postings to the general ledger accounts may come from any and all of the following sources:

ii General journal-adjusting journal for non-cash, adjustments, and correction entries should be posted at least on a monthly basis.

iii Cash receipts journal should be posted on a daily basis.

iv Cash disbursements journal should be posted on a daily basis.

v Accounts receivable journal, for earnings of contract revenue, should be posted as and when the revenue is earned, based on the percentage of completion method or completed contract method.

vi Accounts Payable Journal, for expenditure or cost incurred and obligation occurred, should be posted on a day to day basis.

vii Payroll journal-payroll summary should be posted on a monthly basis.

viii Posting of accounting entries should be done by the Account Executive under direct supervision of DF.

Bank Reconciliation Statement

Bank statement providing all details of bank transactions should be obtained from the bank by the fifth (5) day of the following month and scrutinize all the transactions recorded in bank statement and reconcile with the Bank Journal Register compulsorily on monthly basis. Bank reconciliation statement should be prepared by the tenth (10) day of the following month. Appropriate reconciliation would also be required for bank charges, which are generally accounted for only on receipt of bank statements. The official designated for verification should review the completed bank reconciliation statement very carefully on regular interval.

List of Books of Accounts

Following is a suggested list of books of accounts can be maintained in Computerized Accounting Software with following options by Guraba Engineering Limited:

i Cash Journal Register

ii Bank Journal Register

iii Control Ledger

iv Subsidiary ledger books

v Advance Register

vi Accounts Receivable Register

vii Accounts Payable Register

viii Stock & Store Register

ix Cheque Register

x Assets register

Backup Documents

Backup Documents mean documents that support the genuineness / approval / authorization of the receipts / income and payments / expenditures. Documents include Bills / Invoice / Cash Memos / Money Receipts given by the Vendors / Shop keepers / Suppliers / Contractors / Service Providers / the Vendors / Shop keepers / Suppliers / Contractors / Service Providers / Employees etc. All backup documents must be cancelled by using a “Paid and Canceled“ seal. Numbering of Documents, All payment vouchers, receipt vouchers, journal vouchers, money receipts, debit notes, credit notes and invoices must be printed and sequentially numbered. All these printed vouchers / documents must be used chronologically in order to keep track of any missing vouchers / documents. Any printed voucher / documents becoming unusable for any reason shall be crossed out and marked as “Voided” and shall be kept with the voucher file.

Cash Transaction & Cash Management

Proper management of cash is important for smooth running of an organization. The disbursement of cash, therefore, is a regular occurrence, and a sufficient level of cash should be kept available to meet these requirements, however cash is not a productive asset, as it earns no return. Therefore, only cash necessary to meet anticipated day-to-day expenditures plus a reasonable cushion for emergencies should be kept available. Any exceeds cash should be invested in liquid income producing instruments. To maximize return of idle funds cash not required for operations should be invested. Finance section is responsible for appropriate cash management.

Duration of Cash Transaction & Collection of Cash

All departments should deposited cash and credit sells vouchers day by day basis and cash sales money should not hold any more days and the departmental manager should ensure to deposit the cash sales money in due time that is previous days cash sales deposited today at the beginning of the office hours. In order to complete writing of Cash Scroll Books and their posting in the Cash Journal Register through computer, daily cash transactions shall be closed at least two hours before the close of the office.

Closing of Accounts

Each day, all cash receipts & payments shall be entered into the Cash Journal Register and it should be closed daily. Cash Officer (F&A) shall check and verify the cash balance and Cash Journal Register at the end of each day and duly signed. Manager (F&A) and Director-in-Charge (Finance) will verify the cash balance and verify the Cash Journal Register at the end of each month and signed duly.

Petty Cash and Payment Limit

Petty cash will be maintained on impress system. Each IOU slip should be adjusted within four (4) working days and any advances within one week after execution of the events or assignment. The Company provides various kinds of services to its Directors through some cost centre/ departments and the Directors enjoy the facilities and services from of those departments subject to payment of bill either in cash or in credit. The amount of cash / sale proceeds on account of availing the facilities or cost of items are collected by concerned section and the concerned salesmen/waters in turn should deposit the amount of cash to the Company-Cashier/Accounts Section on the next day of collection. Dues from Directors are collected by main cash counter/Accounts Section.

i Numerous small payments, which are usually required for day-to-day activities shall be paid out of the petty cash, which will be maintained as Petty Cash Impress form by the Accounts Officer.

ii Petty cash up to Tk. 50,000 (Taka twenty thousand only) will be maintained at the office of the Company to meet daily petty expenses

iii Replenishment of petty cash should be processed when the balance is reduced to Tk. 5,000 (Taka five thousand only)

iv Proper evidence for expenses must be submitted to the petty cash custodian at the time of payment.

v Petty cash custodian shall prepare a Statement of Petty Cash at the end of each day, which will be counter signed by the DF(Director).

vi Petty cash custodian shall be personally responsible for safe keeping of the petty cash.

Advances from Petty Cash

i Advance may be made from petty cash for an amount not exceeding Tk. 500.00 with the approval of the secretary.

ii The advances must be adjusted within 72 hours from the date the advance was given.

iii No advance will be given if the previous advance is not cleared.

iv All the supporting documents attached to the payment voucher must be cancelled to prevent reuse by stamping each item “Paid” and the payment voucher number will be written on each of the supporting document.

Cash deposited into Bank

The cashier, cash officer and Manager (F&A) will make sure of the deposition of the cash collected daily into bank and record the transaction immediately in the Cash Journal Register. The Cash Officer will prepare the pay-in slip. The Manager (F&A) and The Director-In-Charge (Finance) will make best arrangement to send the money in the bank.

Cross Checking of Cash Balance

i The cash balance in the main cash must be counted at least once a week and agreed to the cash book by someone other than the person who controls the cash. When the cash is counted, a record must be kept of the actual amount in the safe, split into the denominations of notes and coins.

ii In addition to routine weekly c ash counts, the Director of Finance (DF) or any person as authorized by DF should perform occasional surprise cash counts and agree the count to the cashbook at that time.

iii All cash that is received must be banked intact so that the total receipt can be traced to the bank statement.

iv Proper numbered receipts with sequential numbers must be used to record all income.

v No receipt number should be missing. In case of cancelled, voided receipt, the receipt should be kept with the receipt book.

vi Unused receipt books should be kept under lock and key with the responsibility of the Accounts.

vii Receipt should be used in sequential order and recorded in a receipt book register.

Bank Transaction & Bank Management

All funds (received) shall be deposited into the Guraba Engineering Limited’s accounts with the bankers of the Guraba Engineering Limited and shall not be withdrawn except by cheque signed by allowed personnel (as per Delegation of Financial Authorities). All receipts of money through cheque / draft / pay order / transfer advice, bank account shall be debited and relevant source / liability / income account is credited. Cheque / Draft / Pay order shall be deposited into bank through deposit slip of the bank. General financial policy of Guraba Engineering Limited is to encourage receipts and payments through bank.

Operation of Bank Accounts

The Constitution of Guraba Engineering Limited describes in provision 19 (4) that the bank transactions will be operated with joint signature of any two persons among the Chairman, Secretary and Director-In-Charge or as per decision of the Board of directors. Guraba Engineering Limited has decided that the Bank account will be operated as per decision of the Board of directors. A suggested bank signatories has been given in Delegation of Financial Authorities. Chairman has the authority to make any changes, amendments in the bank signatory powers with the consent of the Board of directors of Guraba Engineering Limited.

Withdrawal of Cash from Bank

For withdrawal of money (liquid cash) from the bank account for working cash or for any operational expenses, a requisition for fund must be prepared for approval in accordance with the delegated authority and withdrawal of cash from bank shall be in accordance with the guidelines of “Delegation of Financial Authority”. When cash to be withdrawn, cash cheques should denote “Account Payee Cancelled” Accounts personnel shall always keep in mind that the maximum closing cash balance in hand should not exceed Taka 150,000 (One hundred and fifty thousand) after the day transaction in Guraba Engineering Limited Director-In-Charge and Taka 10,000 in Unit Offices.

Bank Reconciliation Statement

After receiving the monthly bank statement, the bank balance shown in that statement as of last day of the month must be reconciled with the balance shown in the Bank Journal Register on the same day by preparing a bank reconciliation statement.Bank reconciliation statements shall be prepared by Assistant Manager (F/A) duly checked by Manager Accounts & Finance and he shall be submitted for approval of the Director-In-Charge. The bank charge or interest detected to be not incorporated earlier in the Bank Journal Register should be entered in the Bank Journal Register by preparing a voucher to this effect. Any deposit / interest, payment or cheques not recorded in the bank accounts or bank statement shall be reconciled by adding or deducting from the closing balance as shown by the bank statement. A reversal entry should be processed for cancelling the cheque issue entry if the cheque is found not presented within its validity period. Any difference should be thoroughly checked and investigated with the bank.

Ordering of New Cheque book

Respective Manager (Accounts) with the approval Manager (Accounts & Finance) and Director-In-Charge (Finance) shall initiate for ordering new cheque book on reaching the Cheque book order leaf. While receiving new cheque book from bank respective Cash Officer (F&A) shall count the cheque leaf and satisfy himself that the numbers of cheque leaves are found in order.

Fund Management & Risk Management

Fund Management:

Guraba Engineering Limited must issue a money receipt at the time of receipt of the money (cash / cheque / pay order / demand draft) from whatever source. Every single collection must be deposited with the finance department on the same day of receipt. Finance/Accounts department shall deposit all collection to the nominated bank account on the following day. The finance department shall immediately update the system for all such funds received and enter in the books of accounts on the same day.

Operation Bank Accounts

Separate operational bank accounts should be maintained by Guraba Engineering Limited for different purposes. The authorized signatories for these accounts should be nominated by the Company:

Development Fund Bank accounts

Guraba Engineering Limited shall maintain bank accounts to carry out Guraba Engineering Limited Development Fund activities. No transactions other then Development Fund Receipts / Payments / Advances can be made from this account.

Investment of Surplus Fund

Excess funds or otherwise as per decision of the Board of directors/ Director-In-Charge can be placed in short-term deposits, fixed deposits and other savings instruments/investment in any area which would be more effective use of fund that will increase the fund. The title of the investments must belong to. Guraba Engineering Limited These deposits should only be placed in a reputable bank. In no circumstances these investments can be pledged as security or guarantee without the approval of the Board of directors. Record of each investment should be maintained separately with information like Principal Amount of the Investment, Interest Accrued, Principal En-cashed, Interest En-cashed, and Closing Balance etc. At the end of each month balance confirmation for the investment should be obtained and differences (if any) must be reconciled immediately.

Budget & Budgetary Control

Budget is a pre-determined statement of income and expenditure of an organization for a specific period, which includes projection of resources and estimated expenditure, required to achieve organizational goals in numeric terms. The purpose of preparing a budget is to ensure proper utilization of limited resources to their maximum potential, for which adequate planning, organizing and controlling are essential. The following should be incorporated in the preparation of the budget.

i Estimates of Revenue

ii Estimates of Recurrent Expenditure

iii Estimates of Capital Expenditure

iv Cadres

v A Statement of projected Income and Expenditure

vi A Cash Flow Statement

vii A projected Balance Sheet

viii ICC calendar for the year of budget

ix Venues for ICC matches to be played in Bangladesh

Timing of Budget Preparation

The Annual budget is prepared for one year from October to September. Budget should be submitted by the all Board of directors, Directors, Sub-Committee and Departmental Head (where applicable) within mid-September to Director-in-Charge (Finance) will submit the consolidated budget with analysis and recommendation of Director-in-Charge (Finance) to the Budget Review Committee / Finance Committee within 30th September. After scrutiny and finalization of the budget, the Budget Review Committee / Finance Committee will place the budget within 1st October in the Board of directors Meeting for approval. After Board of directors approval the budget will be placed before the AGM for post facto approval. After finalization and approval of the budget the relevant portion of the budget will be given to the respective committee / Department.

Format of budget

i Accounts section of Guraba is responsible for preparing Budget annually i.e. for every financial year (October to September). Monthly budget should also be prepared for close monitoring of activities of the Company.

ii The budget shall be prepared for every financial year i.e. from October to September.

iii Preparation and submission of budget.

iv The Head of Finance & Accounts Section shall be responsible for preparation of budget on the basis of data and information collected from every section of the Company. He shall request every individual section to provide necessary data and information required for preparation of budget. He may require any information as necessary for preparing budget. Head of every department should be responsible for providing such information in due time to the Accounts Section.

v The budget should be signed by Head of Finance & Accounts, Secretary and Director -in-Charge, Finance before submission of the same to the Finance Sub-Committee.

vi The budget should be placed before Finance Sub-committee by 1st August of each year.

Budgetary Control

Budgetary Control is a system of planning and controlling cost, which starts with the establishment of budget relating to activities to be carried out in order to achieve the organizational goals and regular comparison between budget and actual results / costs; analysis of variances and taking corrective measures.

i Budget refers to “estimated statement” of income and expenditure of the Company for specific time period. Budget is an important tool for proper utilization of limited resources. Section-wise monthly budget will be prepared.

ii Budgetary control is a system of planning and controlling cost, which starts with the establishment of budget relating to activities to be carried out in order to achieve the organizational goals by regular monitoring of budgeted and actual results, analysis of variances and corrective measure.

iii Budgetary control will start with the preparation of budget in relation to activities of the Company. It will include the following:

- Monthly comparison between budgeted and actual results.

- Analysis of variances

- Taking corrective actions

Objectives of the Budgetary Control System

From the functional point of view, a system of Budgetary Control will serve the purpose of Planning, Co–ordination and Control. The objectives of the budgetary control are detailed below:

i Combining the ideas of all levels of management in the preparation of different functional budget

ii Coordinating all the activities of a program and organization

iii Helping to centralize control and de-centralize responsibilities

iv Planning and controlling income and expenditure to determine organizational needs

v Acting as a guide for management decisions

vi Providing a yardstick against which actual results are compared

vii A tool helping to point out the areas where management action is required

Budget Monitoring

Guraba Engineering Limited Finance Department shall closely control and monitor the budget with the actual results on quarterly basis. At all levels of Guraba Engineering Limited, the persons concerned with the Expenditure Process (requisition / authorization / disbursement / approval) will be responsible for ensuring that the expenses are incurred within the budgetary provisions. Before making any commitment for any expenditure, the concerned person shall ensure that disbursement and unpaid obligations do not exceed the budget limit. The Budget shall be closely monitored by the Finance Department of Guraba Engineering Limited, who are responsible for preparation of monthly Financial Statement, Variance Report showing Budget VS Actual amounts and reasons for major variances. The Diractor-in-Charge (Finance) will oversee the budget monitoring/controlling process. Monitoring of development budget shall be overseen by the program managers in collaboration with the financial staff Directors. Monitoring of Specific Tournament budget shall be overseen by the Concerned Chairman in collaboration with the financial staff Directors.

Budget Review

i After getting proposed budget Finance Sub-Committee shall review the budget. Finance Sub-Committee may recommend changing, amending, and modifying the budgets, if necessary. On the basis of Finance Sub-Committee’s recommendations the budget to be updated.

ii The Finance Sub-Committee shall finally forward the budget to the Board of directors by 30 September.

Approval of Budget:

i. The budget will be approved finally at the Board of directors meeting.

ii. After approval of the budgets, Head of Accounts Department shall send a copy of approved budget to the concerned department for budgetary control purposes.

Findings of the Study

i Guraba Engineering Limited used internet based software which is one of the most latest accounting software. Because of this software, activities are run more quickly than the previous. As it is a net based software management can access any time for information. Sometime software makes disturbances in work when server does not work.

ii Personnel have lack knowledge about software.

iii Sometime information gap occur between head office and factory.

iv Guraba Engineering Limited performs their activities with responsibility.

v Guraba Engineering Limited has capacity to meet its short term obligation because Guraba Engineering Limited current ratio increases than before year.

vi Guraba Engineering Limited Current assets are highly liquid.

vii Inventory Turnover increase. High inventory turnover is offer regard as the signal of efficient management. This ratio indicates that haw fast we can sell product.

viii Fixed asset, current asset, profits are increased than before year.

ix Guraba Engineering Limited has good policies and procedure for conducting accounts and finance department.

x The costing budget and production budget are usually made for three month.

xi Guraba Engineering Limited does transaction with voucher.

Recommendations

From the assessment of the Financial and Accounting Activities of Guraba Engineering Limited, following recommendations should be focused for the smooth running of the renowned concern of Guraba Engineering Limited group and higher management should take robust initiatives in this regard. These are highlighted below.

For accounts section

- Accounting information should be updated within soonest possible time.

- Personal should be well trained in use of software.

- The payment of bills should be more quick than the present.

- Shortcoming of current software should be resolved as quick as possible.

- Guraba Engineering Limited should start to run the software as soon as possible.

For finance section

- Company should try to maintain standard ratio like; current ratio, Quick ratio, leverage ratio, profitability ratio etc.

- Management need to apply cost control mechanisms.

- Return should higher than cost of fund.

- Source of financing should be justifiable.

- The trend of higher import growth should be maintained.

- Tax holiday period should be unchanged.

Conclusion

The report has attempted to find out the shortcomings of accounting system and financial statements of Guraba Engineering Limited. I am able to collect information from Accounts and Finance department but it is very difficult to make a rich report in such a limited time. I have to ignore some confidential data. I also take support from internet and some finance books and some finance books for secondary.

Only existence of a good accounting rule does not ensure its application to the organization. The result of a system depends on the manner in which it is applied. We hope that proper implementation of this rule will help the Company to achieve its objectives. Though the Accounts Section of the Company is not accustomed to follow specific rules and regulations, it may take time to implement all the sections of this rule. But the authority should take it positively and the rules and regulations should be applied carefully.

Guraba one of the prominent engineering business house in Bangladesh, have been continuing its business. The most important thing is that Guraba Engineering Limited is honest in maintaining its quality, efficacy, warranty, time schedule, after sales service and transparency with its customers. Because of its superior quality, dedicated commitment and prompt customer services Guraba Engineering Limited. has succeeded to create a brand image in the heart of its customers.

After the data analysis it can be said that the accounting of Guraba Engineering Limited is very strong and the finance condition of the company are changed positively