Executive Summary

Credit risk is one of the most vital risks for any commercial bank. Credit risk arises from non performance by a borrower. It may arise from either an inability or an unwillingness to perform in the pre-commitment contracted manner. The real risk from credit is the deviation of portfolio performance from its expected value. The credit risk of a bank also affects the book value of a bank. The more credit of a particular is in risk, the more probability of a bank to be insolvent. Therefore, the status of depositor in the bank is at risk and probability of incurring loss from their deposited value. In other way the risk of a commercial bank is calculated through long term and short term rating by the credit rating agencies.

In my whole report, I have worked on the credit risk of Eastern Bank Limited. During the preparation of the report, I provide the last five years information of City Bank from 2006 to 2010. In the whole report I have also explained the credit policy and credit risk management of City Bank.

Finally, I like to conclude that City Bank is one of the most promising and fast growing banks in our country. According to its operational excellence, it is now competing with some renowned foreign commercial banks which are operating in our country. Hopefully it may achieve its target to simplify the banking system in Bangladesh.

Introduction

The BBA internship program is a mandatory requirement for the students who are graduating from the BBA program of International Islamic University Chittagong, Dhaka campus In the internship program, I was attached to a host organization named ‘The City Bank Limited’, for three months. During this period I learned how the host organization works with the help of the internal supervisor. As a result, I have decided to make a report on “Credit Risk Management System: A Study on The City Bank Limited”. As a student, I have learned about the activities of a bank. I also have learned the report writing as a great deal of theory is included in this report. It will be also benefited for the people who are interested to know about CBL.

Objective of the Study

This research paper has put emphasized to identify the existing and probable risks on credit management systems of the commercial banks in Bangladesh. Meanwhile, I have analyzed the risk on lending for minimizing the risks at an acceptable extent. The objectives behind this research paper are pointed below:

Broad Objective

The broad objective of the research is to get an idea about the credit risk management system in Bangladesh. Moreover, this study tried to reveal the impact of credit risk management process on the institution’s financial performance

Specific objective

Specific objective of the report are to be determined:

- To review the existing credit risk management systems, tools & techniques use in banks and financial institutions.

- To identify the weakness and limitations of the existing credit risk management systems and tools.

- To review the existing and probable core risk factor for the banks.

- To identify the existing and future credit risk of the bank.

- To find out a common standard credit risk management systems for the banks.

- To examine the influencing factor for deteriorating the loans.

- To find out ways and means to recover deteriorate loans & advances of the banks.

Rationale of the Study

Credit risk is most simply defined as the potential that a bank borrower or counterpart will fail to meet its obligations in accordance with agreed terms. The goal of credit risk management is to maximize a bank’s risk-adjusted rate of return by maintaining credit risk exposure within acceptable parameters. The effective management of credit risk is a critical component of a comprehensive approach to risk management and essential to the long-term success of any banking organization.

During internship in CBL in Credit Risk Management department, it was observed that the credit decisions are taken while Risk managers (RM) examine a client’s loan proposal through various steps. Thus, in this research report it has been tried to explain all the risk analyzing factors and the steps that a financial institution works for granting a credit which affects the institution’s financial performance.

Methodology

Methods of Data Collection

Data has been collected from secondary sources. Reviewing the materials i.e. policy and guidelines regarding Credit Risk Management (CRM), visiting to the concern internet website was the methods of data collections.

Sources of Data /information

Data has been collected from secondary sources. Necessary data and information has been collected by the following sources:

- Credit Policy Manual of the Banks.

- Credit Instruction Manual of the Banks.

- Circulars, letters and memos issued by the Banks and regulatory organization i.e. Bangladesh Bank and Govt.

- Prudential Guidelines on Credit Risk Management issued by Bangladesh Bank.

- Annual report of city bank.

- Annual report of Bangladesh bank.

- News papers and journals

- Internet and websites.

Limitation of the study

- The main limitation for conducting this report is time limitation and resources. The given time was not enough to understand all the activities of a bank and how they handle their clients.

- Lack of experience has also acted a constraint for the exploration of the topic.

- Another limitation of the study is lack of sufficient work experience in the credit division during my internship.

Overview on the City Bank Limited

The City Bank Limited was incorporated as a public limited company in Bangladesh under Companies Act, 1913. It commenced its banking business from March 14, 1983 under the license issued by Bangladesh Bank. Presently the bank has 83 branches as at 31 December 2008. Out of the above 83 Branches, 01(one) bank is designated as Islamic Banking Branch complying with the rules of Islamic Shariah, the modus operandi of which is substantially different from other branches run on conventional basis. The bank is listed with Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited as a publicly traded company for its general class of shares.

The City Bank Limited is a leading first generation private commercial Bank in Bangladesh. The bank is committed to provide high quality services to its constituents through different financial products and profitable utilization of fund and contribute to the growth of GDP of the country by financing trade and commerce, helping industrialization, boosting export, creating employment opportunities for the educated youth and encouraging micro-credit leading to poverty alleviation and improving the quality of life of the people and thereby contributing to the overall socio-economic development of the country.

Information of the City Bank Limited at a glance:

| Legal Status | Public Limited Company |

| Date of Incorporation | March 14, 1983 |

| Formal Inauguration | March 27, 1983 |

| Purpose | To run banking business under the umbrella of Banking Company Act 1994 |

| Number of Branches | 83 on December 31, 2008 |

| Total Manpower | 3500 |

| Authorized Capital | Tk.1,750.00 million |

| Paid up Capital | Tk.1,188.00 million |

| Reserves | Tk.1,686.37 million |

| Total Asset | Tk.48,755.40 million |

| Credit Deposit Ratio | 84 : 16 (approximate) |

| Net Profit | Tk. 1700.00 million on December 31, 2008 |

| Growth Rate | 28% |

| Cost of Fund | 9.50% |

| EPS | 39.10 |

| Price Earnings Ratio | 12 times |

| Governing Law | Laws of Bangladesh |

History of the City Bank Limited

City Bank is one of the oldest private Commercial Banks operating in Bangladesh. It is a top bank among the oldest five Commercial Banks in the country which started their operations in 1983 as a public limited company in Bangladesh under Companies Act, 1913. It commenced its banking business from March 14, 1983 under the license issued by Bangladesh Bank. The Bank started its journey on 27th March 1983 through opening its first branch at B. B. Avenue Branch in the capital, Dhaka city. It was the visionary entrepreneurship of around 13 local businessmen who braved the immense uncertainties and risks with courage and zeal that made the establishment & forward march of the bank possible. Those sponsor directors commenced the journey with only Taka 3.4 crore worth of Capital, which now is a respectable Taka 330.77 crore as capital & reserve.

Vision, Mission, Objective

Vision:

‘To be a leading bank in the country with best practices and highest social commitment’- this is the vision of CBL.

Mission:

- To contribute to the socioeconomic development of the country.

- To attain highest level of customer satisfaction through extension of services by dedicated and motivated team of professional.

- To maintain continuous growth of market share ensuring quality.

- To maximize bank’s profits by ensuring its steady growth.

- To maintain the high moral and ethical standards.

- To ensure participative management system and empowerment of Human Resources.

- Nurture an enabling environment where innovativeness and performance is rewarded.

CBL Objective

Strategic Objectives

- To achieve positive Economic Value Added (EVA) each year.

- To be market leader in product innovation.

- To be one of the top three Financial Institutions in Bangladesh in terms of cost efficiency.

- To be one of the top five Financial Institutions in Bangladesh in terms of market share in all significant market segments we serve.

Financial Objectives

To achieve a return on shareholders’ equity of 20% or more on average.

Product profiles

The City Bank Limited is continuously introducing diversified, customize and derivatives products along with usual Banking Products. At present CBL offers the following facilities:

SL. No. | Particulars | |

01. | Trade Finance | |

| Funded | |

| A. | Letter of Credit |

| B. | Acceptance |

| C. | Bank Guarantee |

| Non Funded | |

| A. | Loan against Trust Receipt (LTR) |

| B. | Payment against documents (PAD) |

| C. | Inland Bill Purchase (IBP) |

| D. | Foreign Documentary Bill Purchase (FDBP) |

| E. | Inland Documentary Bill Purchase (IDBP) |

| F. | Short Term Loan (STL) |

| G. | Short Term Revolving Loan (STRL) |

02. | Project Finance | |

| Funded | |

| A. | LC for import of Machinery |

| B. | Acceptance |

| C. | Bank Guarantee |

| Non Funded | |

| A. | Short Term Loan (STL) |

| B. | Short Term Revolving Loan (STRL) |

| C. | Term loan |

| D. | Hire Purchase |

| E. | Lease Finance |

| F. | Loan General |

| G. | House Building Loan (Commercial) |

03. | Working Capital (For Industrial Finance) | |

| A. | Overdraft (Hypo), |

| B. | Overdraft (Pledge), |

| C. | Payment against documents (PAD) |

| D. | Loan against Trust Receipt (LTR) |

| E. | Short Term Loan (STL) |

| F. | Short Term Revolving Loan (STRL) |

| G. | Inland Bill Purchase (IBP) |

H. | SODSE | |

Islamic Banking Products (Corporate)

SL. No. | Name of the Credit Products |

01. | Murabaha Import Bill (MIB) |

02. | Muarabaha Post Import (MPI) |

03. | Musharaka pre-shipment |

04. | Bai muazzaal (Industrial) |

05. | Bai muazzaal (Others) |

06. | Ijara (Lease) |

07. | Murasha (Commercial) |

08. | HPSM -Real estate |

09. | Bai-salam |

10. | Quard against TDR |

11. | Bai muazzaal (Real estate) |

12. | Bai muazzal (Trust receipt) |

13. | Bai muazzaal (Commercial) |

14. | Bai muazzaal (Commercial PC) |

15. | Bai muazzaal (Demand invest) |

General Activities

The principal activities of the Bank are to provide all kinds of commercial banking, consumer banking trade services, custody and clearing to its customers through its branches in Bangladesh. City Bank is among the very few local banks which do not follow the traditional, decentralized, geographically managed, branch based business or profit model. Instead the bank manages its business and operation vertically from the head office through 4 distinct business divisions namely-

- Corporate & Investment Banking;

- Retail Banking (including Cards);

- SME Banking; &

- Treasury & Market Risks.

Retail Banking (including cards)

Retail banking includes the tasks for the following purposes-

- Deposits

- Loans

- Cards- debit card, credit card etc.

- NRB- foreign remittance

- Schedule of charges

- Interest rate on Lending

Treasury & Market risks

City Bank Ltd. has a dedicated Treasury team who is capable of providing all treasury Solutions. Through their foreign correspondent business partners CBL is providing a wide range of Treasury products. In CBL Treasury, there are four teams who are specialized in their own area to ensure the best possible solution to our customer requirement. CBL has following teams in the Treasury:

- Foreign Exchange (local & G7)

- Money Market

- Corporate Sales

- Market research

Employment structure

To attain a diversified and competent workforce is the human resource policy of City Bank. City Bank has a group of efficient Executive & Officers. Skilled personnel have taken into the Bank as a leading Bank in Bangladesh. At present 2,163 number of capable and knowledgeable workforce has been working in City Bank. The ratio of Male and female workforce are now 73:27. The ratio of High level, mid level and Lower level are 15%, 35% and 50% respectively.

Credit Risk Management – Brief Description of the System

A comprehensive and accurate appraisal of the risk in every credit proposal of the Bank is mandatory. No proposal can be put on place before approving authority unless there has been a complete analysis. In order to safeguard Bank’s interest over the entire period of the advance, a comprehensive view of the capital, capacity, integrity of the borrower, adequacy, nature of security, compliance with all regulatory /legal formalities, condition of all documentation and finally a continuous and constant supervision on the account are called for. It is absolute responsibility of the Credit Risk Manager / RM to ensure that all the necessary documents are collected before the proposal is placed for approval. Where Loans/Advances/Credit facilities are granted against the guarantee of the third party, that guarantor must be subject to the same credit assessment as made for the principal borrower.

CBL performs the following steps in credit risk management division-

- Loan administration

- Loan disbursement

- Project evaluation

- Processing and approving credit proposals of the branches

- Documentation, CIB (Credit Information Bureau) report etc

- Arranging different credit facilities

- Providing related statements to the Bangladesh Bank and other departments

Credit Risk Assessment Procedure

A thorough Credit and Risk assessment shall be conducted for all types of credit proposals. The results of this assessment to be presented in the approved Credit Appraisal Form that originates from the Credit Risk Manager / Relationship Manager (RM) and is to be approved by the Credit Committee / Executive Committee of the Board of Directors / Board of Directors. The Credit Risk Manager / RM are the owner of the customer relationship and must be held responsible to ensure the accuracy of the entire credit application / proposal submitted for approval. The Credit Risk Manager / RMs must be familiar with Bank’s Lending Guidelines and should conduct due diligence on new borrowers, principals and guarantors in line with policy guidelines.

Credit Appraisal should summarize the results of Credit Risk Managers / RMs risks assessment and includes, as a minimum, the following details:

- Amount and type of loan(s) proposed

- Purpose of Loan(s)

- Results of Financial analysis

- Loan structure (Tenor, Covenants, Repayment schedule, Interest)

- Security Arrangements

KYC Concept:

The Credit Risk Managers / RM must know their customers and conduct due diligence on new borrowers, principals and guarantors to ensure such parties are in fact who they represent themselves to be i.e., Know Your Customer (KYC).

The Banker – Customer relationship would be established first through opening of CD/ STD / SB accounts. Proper introduction, photographs of the account holders / signatories, passport, Trade License, Memorandum and Articles of the Company, certificate of incorporation, certificate of commencement of business, List of Directors, resolution, etc. i.e. all the required papers as per Bank’s policy and regulatory requirements are to be obtained at the time of opening of the account. A declaration regarding approximate transaction to the account is to be obtained during opening of account. Information – regarding business pattern, nature of business, volume of business, etc. to be ascertained. Any suspicious transaction must be timely addressed and brought down to the notice of Head Office / Bangladesh Bank as required and also appropriate corrective measures to be taken as per the direction of Bank Management / Bangladesh Bank.

Basics of Credit Risk

The following risk areas shall be considered for analyzing a credit proposal.

- Borrower Analysis (Management/Ownership/Corporate Structure Risk):

The majority shareholders, management teams and group or affiliate companies shall be assessed. Any issues regarding lack of management depth, complicated ownership structures or inter-group transactions shall be addressed, and risks to be mitigated.

- Industry Analysis (Business and Industry Risk):

The key risk factors of the borrower’s industry shall be assessed. Any issues regarding the borrower’s position in the industry, overall industry concerns or competitive forces (demand supply gap) shall be addressed and the strengths and weaknesses (SWOT Analysis) of the borrower relative to its competition to be identified. For the above purpose the Credit Risk Managers/RM may obtain / collect data from the statistical year book / economic trends of Bangladesh Bank / public report / newspaper/ journals etc

- Supplier/Buyer Analysis/Market Risk:

Any customer or supplier concentration shall be addressed, as these could have a significant impact on the future viability of the borrower.

- Market Risk:

The sufficient market data is to be obtained to identify clients/borrowers’ market share in the industry/demand-supply gap in the market.

- Technological Risk :

The product that is manufactured must be technologically viable i.e. whether the technology applied is updated. The product’s stage in its life cycle must be understood. Technical Aspects of the products must be addressed. The Credit Risk Manager / RM must be satisfied with the mitigating factors of technical and technological risk, associated with the products.

- Financial Analysis (Historical / Projected):

An analysis of a minimum of 3 years historical financial statements of the borrower should be presented. Where reliance is placed on a corporate guarantor, guarantor’s financial statement should also be analyzed. The analysis should address the duality and sustainability of earnings, cash flow and the strength of the borrower’s balance sheet. Specifically, cash flow, leverage and profitability must be analyzed. In this regard the Credit Risk Manager / RM must look into the status of chartered accountant audit firm.

Where term facilities (tenor > 1 year) are being proposed, a projection of the borrower’s future financial performance should be provided, indicating an analysis of the sufficiency of cash flow to service debt repayments. Loans shall not be granted if projected cash flow is insufficient to repay debts. In this regard the possibilities of cost overrun and sensibility analysis shall be done.

- Account Conduct:

For existing borrowers, the historic performance in meeting repayment obligations (trade payments, cheque, interest and principal payments, etc.) shall be assessed. In this regard the Credit Risk Manager / RM may look into the account turnover like debt summation / credit summation / highest debit balance/ highest credit balance (or lowest debit balance), no. of debit entries/ no. of credit entries for last three years (year-wise).

- Adherence to Lending Guidelines :

The Credit Applications/ Appraisals must be prepared in line with Bank’s lending guidelines. It must be clearly stated whether or not the application/proposal is in compliance with Bank’s Credit Policy lending guidelines.

- Interest Rate Risk :

The interest rate must be fixed based on different risk factors associated with the type of business such as liquidity risk, commodity risk, equity risk, and loan period risk. Interest rate also arises from the movements of interest rate in the market. In assessing the pricing and profitability, the Credit Risk Manager/RM must consider the income from ancillary business like foreign exchange business, group business, volume of business etc.

- Foreign Exchange Risk :

The foreign exchange transaction is associated with foreign currency fluctuation risk. Therefore the Credit Risk Manager/RM must take care of for the Foreign exchange risk.

- Cost overrun Risk :

This type of risk is generally involved in taking project finance decision. A high degree of cost overrun may cause the failure of the project. Therefore the Credit Risk Manager must consider the cost components of the project and their chance of devaluation.

- Security :

A current valuation of collateral must be made by Bank’s approved enlisted surveyors and the quality and priority of security being proposed shall be assessed properly.

Loan shall not be granted solely on security consideration. Adequacy and the extent of the insurance coverage shall be assessed. The Credit Risk Manager/RM must look into the client’s interest / dependability on the collateral offered as security.

- Name lending (Relationship Assessment) :

Credit proposals shall not be unduly influenced by an over reliance on the sponsoring principal’s reputation, reported independent means, or their perceived willingness to inject funds into various business enterprises in case of need. These situations shall be discouraged and treated with great caution. Rather, credit proposals and the granting of loans will be based on sound fundamentals supported by a thorough financial and risk analysis.

Risk Grading

Risk grading is a key measurement of a Bank’s asset quality and as such, it is essential that grading is a robust process. All facilities should be assigned a risk grade. Where deterioration in risk is noted, the Risk Grade assigned to a borrower and its facilities should be immediately changed. Borrower Risk Grades should be clearly stated on Credit Applications.

Significance of Credit Risk Grading (CRG)

Credit risk grading is an important tool for credit risk management as it helps the Banks & financial institutions to understand various dimensions of risk involved in different credit transactions. The aggregation of such grading across the borrowers, activities and the lines of business can provide better assessment of the quality of credit portfolio of a bank or a branch. The credit risk grading system is vital to take decisions both at the pre-sanction stage as well as post-sanction stage.

At the pre-sanction stage, credit grading helps the sanctioning authority to decide whether to lend or not to lend, what should be the loan price, what should be the extent of exposure, what should be the appropriate credit facility, what are the various facilities, what are the various risk mitigation tools to put a cap on the risk level.

At the post-sanction stage, the bank can decide about the depth of the review or renewal, frequency of review, periodicity of the grading, and other precautions to be taken.

Having considered the significance of credit risk grading, it becomes imperative for the banking system to carefully develop a credit risk grading model which meets the objective outlined above.

Definition of Credit Risk Grading (CRG)

- The Credit Risk Grading (CRG) is a collective definition based on the pre-specified scale and reflects the underlying credit-risk for a given exposure.

- A Credit Risk Grading deploys a number/ alphabet/ symbol as a primary summary indicator of risks associated with a credit exposure.

- Credit Risk Grading is the basic module for developing a Credit Risk Management system.

Functions of credit risk grading

Well-managed credit risk grading systems promote bank safety and soundness by facilitating informed decision-making. Grading systems measure credit risk and differentiate individual credits and groups of credits by the risk they pose. This allows bank management and examiners to monitor changes and trends in risk levels. The process also allows bank management to manage risk to optimize returns.

Use of Credit Risk Grading

- The Credit Risk Grading matrix allows application of uniform standards to credits to ensure a common standardized approach to assess the quality of individual obligor, credit portfolio of a unit, line of business, the branch or the Bank as a whole.

- As evident, the CRG outputs would be relevant for individual credit selection, wherein either a borrower or a particular exposure/facility is rated. The other decisions would be related to pricing (credit-spread) and specific features of the credit facility. These would largely constitute obligor level analysis.

- Risk grading would also be relevant for surveillance and monitoring, internal MIS and assessing the aggregate risk profile of a Bank. It is also relevant for portfolio level analysis.

Regulatory Definition on Grading of Classified Accounts

Irrespective of credit score obtained by a particular obligor, grading of the classified names should be in line with Bangladesh Bank guidelines on classified accounts, which is extracted from “Prudential Regulations for Banks: Selected Issues” (updated till August 07, 2005) by Bangladesh Bank are presently as follows:

Basis for Loan Classification:

(A) Objective Criteria:

Any Continuous Loan if not repaid/renewed within the fixed expiry date for repayment will be treated as irregular just from the following day of the expiry date. This loan will be classified as Sub-standard if it is kept irregular for 6 months or beyond but less than 9 months, as `Doubtful’ if for 9 months or beyond but less than 12 months and as `Bad & Loss’ if for 12 months or beyond.

Any Demand Loan will be considered as Sub-standard if it remains unpaid for 6 months or beyond but not less than 9 months from the date of claim by the bank or from the date of forced creation of the loan; likewise the loan will be considered as ‘Doubtful’ and ‘Bad & Loss’ if remains unpaid for 9 months or beyond but less than 12 months and for 12 months and beyond respectively.

In case any installment(s) or part of installment(s) of a Fixed Term Loan is not repaid within the due date, the amount of unpaid installment(s) will be termed as `defaulted installment’.

Computation of Credit Risk Grading

The following step-wise activities outline the detail process for arriving at credit risk grading.

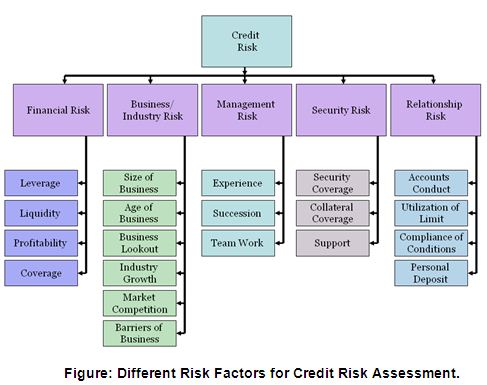

Step I: Identify all the Principal Risk Components

Credit risk for counterparty arises from an aggregation of the following:

- Financial Risk

- Business/Industry Risk

- Management Risk

- Security Risk

- Relationship Risk

Each of the above mentioned key risk areas require be evaluating and aggregating to arrive at an overall risk grading measure.

a) Evaluation of Financial Risk:

Risk that counterparties will fail to meet obligation due to financial distress. This typically entails analysis of financials i.e. analysis of leverage, liquidity, profitability & interest coverage ratios. To conclude, this capitalizes on the risk of high leverage, poor liquidity, low profitability & insufficient cash flow.

b) Evaluation of Business/Industry Risk:

Risk that adverse industry situation or unfavorable business condition will impact borrowers’ capacity to meet obligation. The evaluation of this category of risk looks at parameters such as business outlook, size of business, industry growth, market competition & barriers to entry/exit. To conclude, this capitalizes on the risk of failure due to low market share & poor industry growth.

c) Evaluation of Management Risk:

Risk that counterparties may default as a result of poor managerial ability including experience of the management, its succession plan and team work.

d) Evaluation of Security Risk:

Risk, that the bank might be exposed due to poor quality or strength of the security in case of default. This may entail strength of security & collateral, location of collateral and support.

e) Evaluation of Relationship Risk:

These risk areas cover evaluation of limits utilization, account performance, conditions/covenants compliance by the borrower and deposit relationship.

Credit Risk Grading Process

- Credit Risk Grading should be completed by a Bank for all exposures (irrespective of amount) other than those covered under Consumer and Small Enterprises Financing Prudential Guidelines and also under The Short-Term Agricultural and Micro – Credit.

- For Superior Risk Grading (SUP-1) the score sheet is not applicable. This will be guided by the criterion mentioned for superior grade account i.e. 100% cash covered, covered by government & bank guarantee.

- Credit risk grading matrix would be useful in analyzing credit proposal, new or renewal for regular limits or specific transactions, if basic information on a borrowing client to determine the degree of each factor is

- Readily available,

- Current,

- Dependable, and

- Parameters/risk factors are assessed judiciously and objectively.

- The Relationship Manager as per Data Collection Checklist as shown in Appendix-A should collect required information.

- Relationship manager should ensure to correctly fill up the Limit Utilization Form as shown in Appendix-B in order to arrive at a realistic earning status for the borrower.

- Risk factors are to be evaluated and weighted very carefully, on the basis of most up-to-date and reliable data and complete objectivity must be ensured to assign the correct grading. Actual parameter should be inputted in the Credit Risk Grading Score Sheet as shown in Appendix–C.

- Credit risk grading exercise should be originated by Relationship Manager and should be an on-going and continuous process. Relationship Manager shall complete the Credit Risk Grading Score Sheet and shall arrive at a risk grading in consultation with a Senior Relationship Manager and document it as per Credit Risk Grading Form as shown in Appendix-D, which shall then be concurred by the Credit Risk Manager in consultation with a Senior Credit Risk Manager.

- All credit proposals whether new, renewal or specific facility should consist of

- Data Collection Checklist,

- Limit Utilization Form

- Credit Risk Grading Score Sheet, and

- Credit Risk Grading Form.

- The Credit Risk Managers then would pass the approved Credit Risk Grading Form to Credit Administration Department and Corporate Banking/Line of Business/Recovery Unit for updating their MIS/record.

- The appropriate approving authority through the same Credit Risk Grading Form shall approve any subsequent change/revision i.e. upgrade or downgrade in credit risk grade.

Early Warning Signals

Early Warning Signals (EWS) indicate risks or potential weaknesses of an exposure requiring monitoring, supervision, or close attention by management.

If these weaknesses are left uncorrected, they may result in deterioration of the repayment prospects in the Bank’s assets at some future date with a likely prospect of being downgraded to classified assets.

Early identification, prompt reporting and proactive management of Early Warning Accounts are prime credit responsibilities of all Relationship Managers and must be undertaken on a continuous basis.

Despite a prudent credit approval process, loans may still become troubled. Therefore, it is essential that early identification and prompt reporting of deteriorating credit signs be done to ensure swift action to protect the Bank’s interest. The symptoms of early warning signals as mentioned below are by no means exhaustive and hence, if there are other concerns, such as a breach of loan covenants or adverse market rumors that warrant additional caution, a Credit Risk Grading Form (Appendix-D) should be presented.

Irrespective of credit score obtained by any obligor as per the proposed risk grade score sheet, the grading of the account highlighted as Early Warning Signals (EWS) accounts shall have the following risk symptoms-

- Marginal/Watch list (MG/WL – 4): if –

- Any loan is past due/overdue for 60 days and above.

- Frequent drop in security value or shortfall in drawing power exists.

- Any loan is past due/overdue for 90 days and above

- Major document deficiency prevails (such deficiencies include but not limited to; board resolution for borrowing not obtained, sanction letter not accepted by client, charges/hypothecation over assets favoring bank not filed with Registrar, Joint Stock Companies, mortgage not in place, guarantees not obtained, etc.)

- A significant petition or claim is lodged against the borrower.

- Special Mention (SM – 5): if –

The Credit Risk Grading Form of accounts having Early Warning Signals should be completed by the Relationship Manager and sent to the approving authority in Credit Risk Management Department. The Credit Risk Grade should be updated as soon as possible and no delay should be there in referring Early Warning Signal accounts or any problem accounts to the Credit Risk Management Department for their early involvement and assistance in recovery.

Exceptions of Credit Risk Grading

- Head of Credit Risk Management may also downgrade/classify an account in the normal course of inspection of a Branch or during the periodic portfolio review. In such event, the Credit Risk Grading Form will then be filled up by Credit Risk Management Department and will be referred to Corporate Banking/Line of Business/Credit Administration Department/Recovery Unit for updating their MIS/records.

- Recommendation for upgrading of an account has to be well justified by the recommending officers. Essentially complete removal of the reasons for downgrade should be the basis of any upgrading.

- In case an account is rated marginal, special mention or unacceptable credit risk as per the risk grading score sheet, this may be substantiated and credit risk may be accepted if the exposure is additionally collateralized through cash collateral, good tangible collaterals and strong guarantees. These are exceptions and should be exceptionally approved by the appropriate approving authority.

- Whenever required an independent assessment of the credit risk grading of an individual account may be conducted by the Head of Credit Risk Management or by the Internal Auditor documenting as to why the credit deteriorated and also pointing out the lapses.

- If a Bank has its own well established risk grading system equivalent to the proposed credit risk grading or stricter, then they will have the option to continue with their own risk grading system.

Credit Risk Grading Review

Credit Risk Grading for each borrower should be assigned at the inception of lending and should be periodically updated. Frequencies of the review of the credit risk grading are mentioned below-

| Number | Risk Grading | Short | Review frequency (at least) |

01 | Superior | SUP | Annually |

02 | Good | GD | Annually |

03 | Acceptable | ACCPT | Annually |

04 | Marginal/Watchlist | MG/WL | Half yearly |

05 | Special Mention | SM | Quarterly |

06 | Sub-standard | SS | Quarterly |

07 | Doubtful | DF | Quarterly |

08 | Bad & Loss | BL | Quarterly |

CIB Report:

To ensure the credit discipline and to maintain the customer’s CIB data base henceforth the Management of City Bank has set up a centralized CIB Unit. The major function of CIB is to provide credit information to the Bank’s/Financial institutions to know the credit status of their prospective customers. This report helps the banker’s/lenders for credit appraisal, risk assessment and finally make the decisions for lending with a prudent manner.

Under the existing laws the banks and financial institutions are not permitted to extend new credit facilities or renew existing credit facilities to defaulting borrowers. In order to enable the banks and financial institutions to ascertain the loan status of the borrowers/owners fully automated Credit Information Bureau was established in 1992 to collect all credit related information in respect of each borrower/owner. Credit Report of CIB is a significant risk measuring factor for credit risk management. By the CIB report Bank can understand about the loans and repayment behavior of a customer.

Physical Visit of the Project:

Before approval of a loan physical visit of the project, it is very important to make lending decisions. Risk Managers and some time the third party agency has visit the project whether the project viable or not. It is an important credit risk management techniques.

But the fact is Risk Manager’s are so busy with there desk work it is quite impossible for them to visit all the projects. They usually visit to the big projects.

Account Transaction:

The customer who has no audited balance sheet examine the account transaction statements is very important for credit decisions. Upon turnover times risk managers have takes the lending decisions.

Sometimes account transactions are not found timely and meticulously. So, credit decisions may vary.

Analysis & Findings

In this chapter, the analysis is done as experiments that will reveal the effectiveness of credit risk management. These experiments will show the effects of credit decisions on the financial performance of the CBL. 4 different analysis have been exposed, these are-

- SWOT Analysis

- Performance Analysis

- Trend Analysis

- Findings

SWOT (Strengths, Weaknesses, Opportunities & Threats) Analysis

Every organization is composed of some internal strengths and weaknesses, also has some external opportunities and threats in its whole life cycle. The following will briefly introduce the customers to the City Bank’s internal strengths and weaknesses, and external opportunities and threats as explored in the past few years.

Strengths:

- Superior quality:

City Bank Ltd. Provides its customers excellent and consistent quality in every service. It is of priority that customer is totally satisfied.

- Efficient Management:

All the levels of the management of City Bank Limited are solely directed to maintain a culture for the improvement of the quality of the service and development of a corporate brand image in the market through organization wide team approach and open communication system

- Effective Strategy:

City Bank takes many effective strategies for the achievement of the organizations goals.

- Experts:

The key-contributing factor behind the success of City Bank Ltd. Is its employees, who are highly trained and most competent in their own field. City Bank Ltd. Provides their employees training both in-house and outside job.

- Centralized Banking systems:

City Banks has introduced centralized banking systems. Credit Risk assessment is done by the highly skilled Risk Managers of Head office.

- Strong Policy and Guidelines:

City Bank’s has introduced a strong Credit policy and Credit Instruction Manual for Credit Risk Management.

- Quality Risk Assessment Tools:

CBL provides a number of quality risk assessment tools, techniques and software’s for Credit Risk Assessment.

- Highly Skilled Workforce:

The key-contributing factor behind the success of City Bank Ltd. Is its employees, who are highly trained and most competent in their own field. City Bank Ltd. Provides their employees training both in-house and outside job.

Weaknesses:

- Strategic Business Unit (SBU) is not properly well organized. Planning and decision making is still the concern of Head Office. Branch has a limited opportunity to access the power.

- Less number of workforces: City Bank Ltd. Has limited human resources compared to its financial activities. There are not many people to perform most of the tasks. As a result many of the employees are burdened with extra workloads and work late hours without any overtime facilities. This might cause high employee turnover that will prove to be too costly to avoid.

- Excess Divisions and Departments.

- Lack of coordination.

Opportunities:

- Strong Managerial Team:

They can take any desperate initiatives to make well of the organization.

- Government Support:

Government of Bangladesh has rendered its full support to the banking sector for a sound financial status of the country, as it has become one of the vital sources of employment in the country now. Such government concern will facilitate and support the long-term vision of City Bank Ltd.

- Evolution of E-Banking:

Emergence of e-banking will open more scope for City Bank Ltd. To reach the clients not only in Bangladesh but also in the global banking arena. Although, the bank has already entered the world of e-banking yet it has to provide full electronic banking facilities to its customer.

- Banking & information technology:

Nevertheless there are ample opportunities for City Bank Ltd. To go for product innovation in line with the modem day need. The Bank has yet to develop credit card facility, lease financing and merchant banking

Threats:

- Mergers and Acquisition:

The worldwide trend of merging and acquisition in financial institutions is causing concentration. The industry and competitors are increasing in power in their respective areas.

- Inadequate Research and Development works and budget.

- Poor Telecommunication Infrastructure:

As previously mentioned, the world is advancing e-technology very rapidly. Though City Bank Ltd. Has taken effort to join the stream of information technology; it is not possible to complete the mission due to the poor technological infrastructure of our country.

- Frequent Currency Devaluation:

Frequent devaluation of Taka and exchange rate fluctuations and particularly Southeast Asian currency crisis adversely affects the business globally.

- Emergence of Competitors:

Due to high customer demand, more and more financial institutions are being introduced in country. There are already 52 banks of various types are operating in the country. Many banks are entering the market with new and lucrative products. The market for banking industry is now a buyer-dominated market. Unless City Bank Ltd. Can come up with attractive financial products in the market; it will have to face steep competition in the days to come.

- Global Economic Recession:

Global economic recession is a big threat for the business people of Bangladesh. Recession helps to reduce the profit margin of the business organization.

- Loan defalcation Culture:

Loan defalcation Culture is a major threat for the banks.

Performance Analysis

Performance analysis explains an institution’s financial position that is depended upon various factors as like assets utilization, capitalization, loan disbursement, cash management etc. even managerial decisions like credit decisions derived from credit risk management. In this analysis section, performance analysis is executed to determine how credit risk management can affect an organization’s financial position.

For 5 years some related financial measures of credit are shown below:

| Particular | 2007 | 2008 | 2009 | 2010 |

| Credit Deposit Ratio | 76.57% | 76.11% | 75.31% | 66.08% |

| Cost of Funds | 5.63% | 5.34% | 6.94% | 7.55% |

| Yield on Loans & Advances | 13.32% | 12.67% | 13.30% | 13.15% |

| Return on Assets | 1.52% | 1.75% | 0.58% | 0.71% |

| Return on Equity | 34.34% | 32.05% | 10.69% | 12.71% |

Trend Analysis

Trend analysis is a forecasting technique that relies primarily on historical time series data to predict the future. For this research report the trends are discussed for the credit related factors like total loan disbursements, position of unclassified and classified loans amount etc.

Total Loans & Advances

Tk in Millions

Particulars | 2006 | 2007 | 2008 | 2009 | 2010 |

| Total Loans & Advances | 17027.84 | 23326.34 | 30789.022 | 26788.47 | 34420.94 |

The above table representation indicates that the amount of total loans and advance of CBL in the year of 2006 to 2010 was respectively BDT 17027.84, 23326.34, 30789.002, 26788.47, and 34420 million taka . Over the five years from the year 2006 to 2010 almost all the years the amount of loans and advance has been increased except the year 2009. In this year their total amount of loans and advance had decreased from the previous three years. So overall it can be said that there is an increasing trend or upward trend over the last five years in the total loan facility provided by the CBL.

Findings of Analysis

Based on the previous chapter analysis segments and the brief description of credit risk management system of CBL following findings are originated:

- Credit Policy:

- City bank has introduced a credit policy and credit instruction manual which encompasses all credit risk components as well as mitigate factor of the probable risks. Risk managers have strictly follows the credit policy accordingly to on lending. But the Management and the board of the Bank have the authority for exceptional credit approval.

- Credit Risk Grading:

- At the time of risk assessment the risk managers are used to obtain an integrated CRG for all Corporate and Small & Medium (SME) customer.

- Insufficient time for risk assessment:

- The risk managers have often insufficient time for credit risk management. Huge workload and hurries for loan approval prevent them from through assessment. So, it is very troublesome to manage the risk in a prudent manner for the risk managers.

- Lack of Training:

- Training of the risk managers is extremely essential for better risk management. Most of the banks have not any regular training program. Lack of proper training on Credit Risk Management risk managers often does the mistakes on credit risk management.

- Few numbers of tools and techniques for Risk Management:

- Banks has a few number of tools and techniques for credit risk assessment i.e. CRG, FSS, CIB which are not sufficient for all kinds of risk management.

- Illegal Pressure from Political persons, Directors and Management of the Bank:

- The Banks in Bangladesh has faces a lot of illegal pressure from Political persons, Directors and Management of the Bank for approval of loan. in that cases Risk managers are bound to approve the loan without any assessment and rationality.

- Lack of Co-ordination with other related Division:

- City Bank has maintains a few co-ordinations with the related divisions and departments. Lack of co-ordination caused a lot of suffer of the risk managers as well as the customers.

- Lack of information in the Credit Proposal:

- Risk Managers often could not found all necessary documents and information for credit risk assessment. That’s why risk managers use their assumption on risk management. Data collection checklists are not duly filled by the Relationship Managers.

- Problems of Financial Analysis:

- Most of the borrower has not audited financials. They provide financial statements which does not follow the rules of accounting. On the other hand credit proposal has not provided a financial summary. Risk Managers has to go through the financial statements for pick up the necessary ratio. So it is very time consuming.

- Limited Security Coverage:

- Customers have offered limited collateral securities against credit facility. So there is a significant risk for loan defalcation. Bank may lose in case of defalcation.

- Limited Insurance Coverage:

- An insurance coverage should obtain for both funded and non funded credit facility. But reality is very few borrowers confirm their insurance coverage. So Banks has no security in case of any uncertainty like fire, strike, riot etc.

- Lack of Customer Banker relationship:

- Due to centralization of banking systems City Bank has maintain a very week relationship with the valued customer. The customers are very much dissatisfied with this worst situation.

- Lack of follow-up and monitoring:

- Credit quality depends on close follow-up and monitoring of loans. The follow-up and monitoring of loans is not strong here. As a result Special Mention Accounts and deteriorating credit are increasing day by day.

Recommendation:

For effective Credit Risk Management of CBL, credit monitoring & judgmental decision after efficient analysis is important that would result in good customer relationship with greater profit earning for the institution with fulfilling NPL target. Some Researchers have also drawn a sort of recommendations that should be considered necessary for effective credit risk management; these are as follows:

- Introduce an easy understandable Credit Policy:

- The Credit Policy of the Bank is very complicated. It should be easy understandable and user friendly. So that all the credit concerns can understand the instruction and follow it meticulously at the time of credit risks management.

- Improvement of Credit Risk Grading Systems:

- An industry wise integrated Credit Risk Grading system should be developed. So that risk can measure for different industry of business.

- Sufficient Workforce & allocate a standard Risk Assessment time:

- Sufficient risk managers should recruit in Credit Risk Management Division and a standard time should allocate for a credit proposal analysis. So that, risk managers could go through the credit proposal for risk managers and have sufficient time for better analysis and assessment.

- Development of tools and techniques for Credit Risk Management:

- Banks has a few numbers of tools and techniques for credit risk assessment i.e. CRG, FSS, CIB which are not sufficient for all kinds of risk management. So, new and effective credit risk management tools and techniques should be introduced by the help of IT Division.

- Reduce of Political pressure & influence of the Directors and Management:

- It is unavoidable of Political pressure & influence of the Directors and Management. Consequently some techniques should introduce so that those pressure and influence will be reduced.

- Financial Analysis:

- An analysis of a minimum of 3 years historical financial statements of the borrower should be presented. Where reliance is placed on a corporate guarantor, guarantor’s financial statement should also be analyzed. The analysis should address the duality and sustainability of earnings, cash flow and the strength of the borrower’s balance sheet. Specifically, cash flow, leverage and profitability must be analyzed. In this regard the Credit Risk Manager / RM must look into the status of chartered accountant audit firm. Financial ratios and important financial figures should be provided as summarize format. So that risk managers could analyze the financials in an easy way.

- Industry Analysis (Business and Industry Risk):

- The key risk factors of the borrower’s industry shall be assessed. Any issues regarding the borrower’s position in the industry, overall industry concerns or competitive forces (demand supply gap) shall be addressed and the strengths and weaknesses (SWOT Analysis) of the borrower relative to its competition to be identified. For the above purpose the Credit Risk Managers/RM may obtain / collect data from the statistical year book / economic trends of Bangladesh Bank / public report / newspaper/ journals etc.

- Follow-up and monitoring:

- Credit quality depends on close follow-up and monitoring of loans. The follow-up and monitoring of loans is not strong here. As a result Special Mention Accounts and deteriorating credit are increasing day by day.

Conclusion:

In Bangladesh 48 scheduled banks has been operating their services. According the annual report of Bangladesh Bank-2007 total loans and advances of those banks is BTD.147600.06 crore, among the total loans and advances BDT.23040.52 crore is the classified/ non-performing loans. The ratio of default/non-performing loans has come into 13.21% which is an alarming situation for the whole economy.

Bangladesh Bank has introduce a good numbers of circulars, guidelines, tools and techniques for managing the credit risk in a prudent manner as well as to minimize the rate of default/ non-performing loans at a standard level. Banks have also some internal policy, guidelines, tools and techniques for better risk management. Despite a prudent credit approval process, loans may still become troubled.

The success of credit risk management has resulted from dedication, commitment, dynamic leadership, effective strategy, planning and decision making, motivating and controlling of bank’s management. In formulating a credit judgment and making quality Credit Decisions, the lending officer must be equipped with all information needed to evaluate a borrower’s character, management competence, capacity, ability to provide collaterals and external conditions which may affect his ability in meeting financial obligations. So, it is obvious that prudent management of these risks is fundamental to the sustainability of a bank.

The research paper encompasses with the existing credit risk management systems, tools and techniques and methodology of the Banks in Bangladesh. In this internship research report an effort has taken to identify the problems and limitations of credit risk management systems as well as find out the causes of loan defalcation tendency of Bangladesh. Eventually, researcher figured out a sort of findings and recommendation for improvement of credit risk management systems so that banks may attain a common standards for credit risk management as a result classified/ non-performing loans in banking sector may diminish.