Social accounting is the process of communicating the social and environmental effects of organizations’ economic actions to particular interest groups within society and to society at large. It is a method of studying the structure of the body economic. Social Accounting is different from public interest accounting as well as from critical accounting. It measures the environmental and social impact of an organization.

Social accounting is commonly used in the context of business, or corporate social responsibility (CSR), although any organization, including NGOs, charities, and government agencies may engage in social accounting. This approach goes beyond the normal formulation of financial statements to also measure a firm’s impact on stakeholders. Social Accounting can also be used in conjunction with community-based monitoring (CBM). Social accounting is an expression of a company’s social responsibilities.

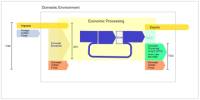

In the words of Edey, Peacock and Cooper: “Social accounting is concerned with the statistical classification of the activities of human beings and human institutions in ways which help us to understand the operation of the economy as a whole.

Social accounting emphasizes the notion of corporate accountability. The principal forms of economic activity are production, consumption, capital accumulation, government transactions and transactions with the rest of the world. These are the components of social accounting. D. Crowther defines social accounting in this sense as “an approach to reporting a firm’s activities which stresses the need for the identification of socially relevant behavior, the determination of those to whom the company is accountable for its social performance and the development of appropriate measures and reporting techniques.”

The concept of ‘Social Accounting’ has gained importance as a result of high-level industrialization which has brought prosperity as well as many problems to society. This approach is an especially useful tool for nonprofits and government entities since their missions are more targeted at improving socially and environmentally relevant activities. It is an important step in helping companies independently develop CSR programs which are shown to be much more effective than government-mandated CSR.

Social accounting is a broad field that can be divided into narrower fields. It should owe a responsibility towards solving many of the social problems. It is concerned with the study and analysis of the accounting practice of those activities of an organization. Environmental accounting may account for an organization’s impact on the natural environment. Sustainability accounting is the quantitative analysis of social and economic sustainability. National accounting uses economics as a method of analysis. The International Standards Organization (ISO) provides a standard, ISO 26000, that is a resource for social accounting. It addresses the seven core areas to be assessed for social responsibility accounting. Similar to traditional accounting, it is a method of quantifying a company’s performance.