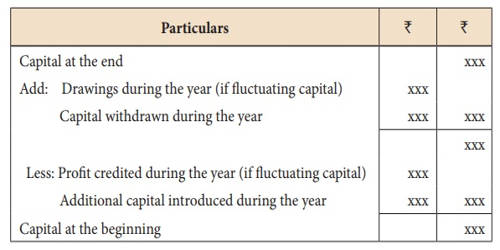

Concept of Goodwill

The name and fame of an organization can be termed as goodwill. It is an intangible asset associated with the purchase of one company by another. Goodwill is the benefit and merit of a good name and reputation. Creating goodwill among people is important in almost every area of your life. Goodwill refers to a measure of the capacity of a business to earn an excess profit. Therefore, goodwill can be defined as an intangible asset of the business. The value of a company’s brand name, solid customer base, good customer relations, good employee relations, and any patents or proprietary technology represent some examples of goodwill. In business, creating goodwill can help you to build relationships that ensure the long-term success of your business.

Thus, goodwill may also be defined as the “value of the reputation of business”. It is a valuable asset if the concern is profitable. Actively take the time to search out ways to build goodwill with your customers. It is an investment in your company. It is useless if the concern is a losing concern. Goodwill can be described as the extra saleable value attached to a prosperous business beyond the intrinsic value of net assets. This reputation translates in monetary terms into expected future profits above-normal profits. Thus the existence of goodwill can be felt through extra earning power. The amount of goodwill is the cost to purchase the business minus the fair market value of the tangible assets, the intangible assets that can be identified, and the liabilities obtained in the purchase. Because of such a nature, it seems like a real asset. But since it is invisible such as patents, trademark, copyrights, etc. goodwill is termed as intangible assets. It depends on several factors, like brand name, relation with related authority but the most thing is the difference between book value and the face value of shares.

To calculate goodwill, we should take the purchase price of a company and subtract the fair market value of identifiable assets and liabilities.

Goodwill Formula: Goodwill = P−(A+L)

where:

- P=Purchase price of the target company,

- A=Fair market value of assets,

- L=Fair market value of liabilities.