Preference shares are used by big corporate as a long-term source of funding for their projects. These shares are one of the important sources of hybrid financing. It is a hybrid security because it has some features of equity shares as well as some features of debentures. The holders of these shares enjoy preferential rights with regard to receiving dividends and getting back of capital in case the company winds-up. It is important to analyze the benefits and disadvantages of affixed by using preference shares as a medium of financing.

Advantages:

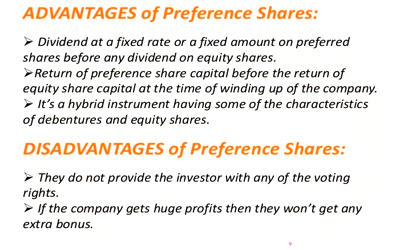

Owners of preference shares receive fixed dividends, well before common shareholders see any money. The advantages of preference shares are:

(a) The earnings per share of existing preference shareholders are not diluted if fresh preference shares are issued.

(b) The issue of preference shares increases the earnings of equity shareholders, i.e. it has a leveraging benefit.

(c) Preference shareholders do not have any voting rights and hence do not affect the decision making of the company.

(d) The preference dividend is payable only if there is profit.

(e) Suitable to Cautious Investors, this is suitable for investors who do not like to take a risk and who like to get fixed dividends.

(f) Attractive Types, redeemable, convertible, and participating preference shares are more attractive. They are very helpful to investors and so they have a ready market.

Disadvantages:

The main disadvantage of owning preference shares is that the investors in these vehicles don’t enjoy the same voting rights as common shareholders. Preference shares suffer from the following disadvantages:

(a) Heavy Dividend, usually, preference shares carry a higher rate of dividend than the rate of interest on debentures. The preference dividend is not tax-deductible and hence it is costlier than a debenture.

(b) In the case of cumulative preference share, the arrear dividend is payable when the company earns profit, which creates a huge financial burden on the company.

(c) The redemption of preference share again creates a financial burden and erodes the capital base of the company.

(d) Preference shareholders get dividends at a constant rate and it will not increase even if the company earns a huge profit, which makes this form of finance less attractive.

(e) Preference shareholders do not enjoy voting rights and hence their fate is decided by the equity shareholders.

(f) Costly, comparing to debentures, financing of preference shares is more costly.