Business Overview of Al-Arafah Islami Bank

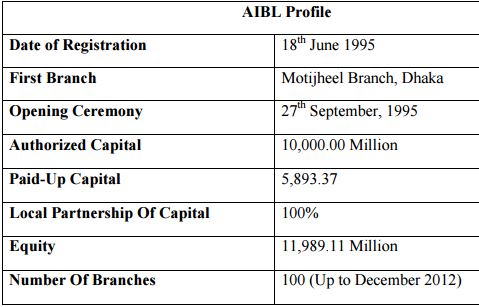

Al-Arafah Islami Bank started its journey on 18 June 1995 with the said in mind and to introduce a modern banking system based on Al-Quran and Sunnah. The opening ceremony took place on 27 September 1995. A group of established, dedicated and pious personalities of Bangladesh are the architects and directors of the bank. Among them a noted Islamic scholar, writer, economist and ex-bureaucrat of Bangladesh Government MR. A. Z. M Shamsul Alam is the founder and chairman of the bank. His continuous inspiration and progressive leadership provided a boost for the bank in getting a foothold in the financial market of Bangladesh. A group of 20 noted and dedicated Islamic personalities of Bangladesh are the member of Board of Director of the bank.

Wisdom of the directors, Islamic bankers and the wish of Almighty Allah make Al-Arafah Islami Bank Limited. It is most modern and leading bank in Bangladesh. New products are the tool of the bank to achieve success. The bank has diverse array of product and services to satisfy customer needs. The bank has achieved a continuous profit and declared a good technology. Now AIBL is one of the Best-Rated banks in Bangladesh. It is in 6th position in CAMELS rating.

The bank is committed to contribute significantly to the national economy. It has made a positive contribution towards the socio-economic development of the country with 100 branches.

Vision Of AIBL

To be a pioneer in Islami Banking in Bangladesh and contribute significantly to the growth of the national economy.

Mission Of AIBL

- Achieving the satisfaction of Almighty Allah both here & hereafter.

- Proliferation of Shariah Based Banking Practices.

- Quality financial services adopting the latest technology.

- Fast and efficient customer service.

- Maintaining high standard of business ethics.

- Balanced growth.

- Steady & competitive return on shareholders’ equity.

- Innovative banking at a competitive price.

- Attract and retain quality human resources.

- Extending competitive compensation packages to the employees.

- Firm commitment to the growth of national economy.

- Involving more in Micro and SME financing.

Commitments of AIBL

Ours is a customer focused modern Islamic Banking sound and steady growth in both mobilizing deposit and making quality Investment to keep our position as a leading Islami bank in Bangladesh.

To deliver financial services with the touch of our heart to retail, small and medium scale enterprises, as well as corporate clients through our branches across the country.

Our business initiatives are designed to match the changing trade & industrial needs of the clients.

Objective Of AIBL

Al-Arafah Islami Bank Limited believes in its uncompromising commitment to fulfill its customer needs and satisfaction and to become their first its customer choice in banking. The bank is committed to run all its activities as per Islamic Shariah. AIBL, its steady progress and continued success has earned lots of reputation that made AIBL is one of the leading Private Banks of the country.

Its aims are to introduce a welfare-oriented banking system and also establish equity and justifies in the field of all economic activities.

Investment is made through different mode permitted under Islamic Shariah

All the activities of AIBL are conducted on interest-free system according to Islamic Shariah.

It plays a vital role in human resource development and employment-generation, particularly for the unemployed youths.

Investment income of bank is shared with the Mudaraba depositors according to ensure a reasonably fair rate of return on their depositors.

Its aims are to achieve balanced growth & development of the country through investment operation, particularly in the less development areas.

It extends co-operative to the poor, helpless and low income group of people for their economic enlistment particularly in rural areas.

Main Focus of AILB In 2012 Is On

To reduce the non-performing assets

- Increase foreign remittance.

- Up-gradation of online banking.

- Introduce credit card.

- Diversify Business & product in case of both deposit and investment.

- Already establish 8 ATM booths in various important locations and want to open more.

- To maintain more shariah compliant.

- Opening of 5 SME Branches.

- Dividend is Stable.

- Developing skill man power through different training.

Special Features Of AIBL

All activities of AIBL are conducted according to Islamic Shariah where profit is is given to the client. In case of AIBL profit is legal alternative to interest.

According to the needs and demands of the society and the country as a whole the bank invests money to different Halal business, like creating jobs, implementing development projects taken by the Government and developing infrastructure.

The bank’s investment policy follow different modes that are approved by Islamic Shariah based on Quran & Sunnah.

The bank is committed towards establishing welfare oriented banking system, economic enlistment of the low income people, create employment opportunities.

The bank is committed to establish an economic system through social justice and equal distribution of wealth.

The bank is contributing to Al-Arafah English Medium Madrasha and AIBL Library.

Line Of Business Of AIBL

- Investment banking (capital market operation in DSC & CSE)

- International Foreign Trade Finance ( Import & Export)

- Foreign exchange dealing ( currency dealing & remittance)

- Corporate finance

- SME banking

- Personal Banking

- Transport Investments

- Broker house

- Merchant banking

- House building investments (staff &commercial)

Product of AIBL:

Deposit accounts of AIBL

Mudaraba Term Deposit Savings (MTDR)

- To open this account one have to must deposit minimum Tk.500/= as an opening deposit.

- Up to Tk.5000/= no charges are deducted from this account

- An estimate profit of 4% is given under this scheme.

Al-Walediah Current Accounts (AWCD)

This kind of account does not provide any profit on total balance; usually business persons or organizations open this kind of account. These kinds of accounts provide the facility of unlimited times of withdrawal of money.

- The current account is denoted as CD account.

- To open this account one have to must deposit minimum Tk.2000/= as an opening deposit.

- No profit is paid on current A/C holder.

- Statement of current A/C is provided monthly to the A/C holder. If needed they give it more than one time according to client. It is free of cost.

- Current A/C can be operated by cheque.

Monthly Installment Based Term Deposit (ITD)

- An exciting to save monthly a certain amount and get attractive return along with estimated profit after tenure.

- Duration of the deposit will be 2, 3, 5, 8, 10 or 12 years along with installment amount of either Tk 200/=, 300/=, 500/=, 1000/=, 2000/=, 5000/=, 10,000/=.

- Profit will be calculated on daily basis upon one’s deposit.

- Any person above 18 can open this scheme. ITD can be opened on behalf of a minor.

- Installments can be deposited in any working day that is not fixed. Even installment may be deposited in advance.

Saving Investment Deposit

- Deposit is accepted by monthly installment

- After expiry of the term double amount of such savings is given without any collateral security.

- By savings deposit any one can take business venture on utilization the amount saved.

Savings Bond Deposit

- Introduce savings bonds for tk. 10,000/=, tk.25,000/=, tk. 100,000/=

- It may be for 3, 5 or 8 years.

- Tax will be considered on the deposited amount along with profit.

Monthly Profit Based Term Deposit Scheme

- To get profit on monthly base.

- It is applicable for resident ( individual/ company) and non-resident

- Deposit amount is one lack or multiple

- Minimum duration is 5 years.

- Tax will be considered on the deposited amount along with profit.

- Profit will be given from the next month’s first working day.

Monthly Hajj Deposit (MHD)

- One can open only one Hajj account in his/her name.

- Duration is one year to 20 years.

- Installment amount depend on the duration.

Termed Hajj Deposit (THD)

- One can open Hajj account in his/her name or in the name of any predecessors or close relatives.

- One can open an account in the name of minor or a child.

- If the Hajj account is opened in the name of other person that person fails to go for unavoidable reason or dies, one can do Badla Hajj by withdrawing this deposit.

- Duration is 5 years to 20 years.

- Separate form has to be filled up to open Termed Hajj deposit.

- Tax will be considered on the deposited amount along with profit.

Monthly Installment Based Marriage Investment Scheme (MIS)

- Installment size from tk.250/=, tk.500/= or tk. 1000/= according to desire.

- Tax will be considered on the deposited amount along with profit.

- Profit is given according to daily-stay basis.

Mudaraba Lakhpoti Deposit Scheme (LDS)

- Maturity period 3, 5, 8, 10 or 12 years.

- Profit is given according to daily-stay basis.

- Tax will be considered on the deposited amount along with profit.

- Monthly installment can be deposited on any working day.

Mudaraba Millionaire Deposit Scheme (MMDS)

- Monthly installment can be deposited on any working day.

- Monthly installment may be tk.24,400/=, tk.17,530/=, tk.13,500/=, tk.10,800/=, tk.8,800/=, tk.5,400/=, tk.4,100/=, tk.2,870/=, tk.1,700/=

- Profit is given according to daily-stay basis.

- Tax will be considered on the deposited amount along with profit.

Mudaraba (Special) Pension Deposit Scheme (MSPDS)

- Maturity period 5, 10 or 15 years.

- Profit is given according to daily-stay basis.

- Tax will be considered on the deposited amount along with profit.

- Monthly deposit from tk. 500/=, tk. 1000/= or any multiple of tk. 1000/=.

Mudaraba Kotipoti Deposit Scheme (MKDS)

- Any person above 18 can open this scheme. MKDS can be opened on behalf of a minor.

- Tax will be considered on the deposited amount along with profit.

- One can take advantage of 80% of his/her deposit as investment.

Investment product of AIBL

Investment in Agriculture Sector

- Investment in Industrial Sector

- Investment in Business Sector

- Investment in Foreign Trade

- Investment in Construction and Housing

- Investment in Transportation Sector

- Hire Purchase Shirkatul Melk (HPSM)

- Investment Schenes in Masque and Madrasa (MMIS)

- Village and Small Investment Schemes (GSIS)

- Small Enterprise Investment Schemes (SEIS)

- Consumer Investment Schemes (CIS)

Services of AIBL

- ATM Card Service

- Online Banking

- Locker Service

Non-performing Loan

In short non-performing loan is called NPL. A sum of borrowed money debtor has missed his/her schedule payment for at least 90 days or 3 months is called non-performing loan.

Many loans become non-performing after being in default for 90 days, but this can depend on the contract terms and condition between client and bank. A non-performing loan is either default or close to being in default. If debtor start to pay his/her loan then it is not under nonperforming loan.

A loan is non-performing when payments of interest and principal are past due by 90 days or more, or at least 90 days or 3 months of interest payments have been capitalized, refinanced or delayed by agreement, or payments are less than 90 days or 3 months overdue. In other words, a loan is usually considered to be non-performing after it has been in default for three consecutive months

Non-performing loan is no longer producing income for the bank. Bank holds nonperforming loans in their portfolio. They choose right buyer to sell them to other investors in order to get rid of risky assets and clean up their balance sheet. Bank must be careful to sale of non-performing loan because they can have numerous financial implications, including affecting the company’s profit and loss and tax situation.

Consider NPL ratio, a smaller NPL ratio indicate smaller loss for the bank. If it is larger NPL ratio mean larger losses for the bank as it writes off bad loan. Some banks are interested to invest money in higher risk sector. They want to get more profit by disbursing high-quantity of loan and charging borrower higher interest rate. Higher risks takers earn more profit.

However, the large numbers of NPL have large number of side effects.

Reasons for Non-Performing Loan

Intentionally: One who intentionally do not repay the loan. As it is known to all they take this money for business purpose or buying-selling. But they do not do that. Instead he/she has intention to lout a big amount of money from the bank.

Mutual understanding with higher management: One takes loan from bank with the help of higher level officer. They divide loan money between them. Instead they have intention to lout a big amount of money from the bank. For example, Hallmark case with Sonali Bank.

Economy Fall of the Country:

Exchange rate fall: If dollar rate is increasing and taka rate is decreasing. That may cause economy fall of the country.

Political unrest: Because of political restrain economy fall of our country for example, Hortal hamper production, that’s why company are not able to shipment their product in time. As a result they don’t earn as much as they assume.

Lack of raw material: It is related with the political restrain. Political restrain cause obstacles in communication. That’s why raw material doesn’t reach timely according to the need of manufacturer.

From the above reasons, economy falls of the country.

Market down: One who take loan for any specific goods. But that goods market is down. Customers are not interested to buy those goods. Client is not able to earn that much money as they assume. Client who takes from the bank he is not able to repay his loan timely.

Natural Calamities: Sometimes natural calamities also cause loan to default. One takes loan from bank. Because of natural calamities he/she is not able to supply his/her goods to the client in time.

Same product in market: Now there is more than one company who produce same product. As a result debtor who takes loan from bank, he/she is not able to get success by that product.

Effect of NPL

There are some effects of NPL that are given below:

- There is a negative relationship between non-performing loan and performing loan. If there is increase of non-performing loan that hamper the performing loan.

- Non-performing loan cause efficient problem on banking sector. If non-performing loan increase that discourage bank’s management to invest money. They lend less money than demand.

- Non-performing loan stopped money cycling. After one party return money, bank management can lend money to the other party. If that party is failure to return money bank is not able to lend it another. Slow flowing of cash always has negative impact on any business.

- Non-performing loan cause earning reduction for the bank. If lender is not able to repay money that hamper bank’s earnings. Interest earning gets stopped. But cost of fund and cost of management are not stopped. The existing lending price has to be increased to run the management cost along with cost of fund. Suddenly increased rate of interest makes hard the return bank money for a performing borrower.

If non-performing loan is increasing that also cause capital erosion. Capital erosion also hampers economic growth. As a result of poor economic condition.

Non-performing loan affects opening of LC. International importers always healthy condition of the exporter’s bank. If bank’s health condition is worse that affects the opening of new LCs. Low rate of LCs makes low bank earning.

NPL creates the credit crunch situation. Credit crunch is a phenomenon that banks ration loan disbursement and new credit commitment that add more risk. Credit crunch also increase the rate of NPL.

As we know bank’s work is to take money from one and give it to another. That person who take loan from bank he is not able to repay it. After a certain period bank have to pay money that keep in bank. Because of NPL it affects bank’s re-balancing action.

Management of Non-performing Loan

Early Alert System

- An early alert account is one that has risks or potential weakness of a material nature requiring monitoring supervision or close attention by management.

- If the weaknesses are left uncorrected, they may result deterioration if the repayment prospects for the investment accounts at some future with prospect of being downgraded to IRG-file.

- Investment monitoring department will identify the weaknesses of the investment accounts, report promptly to the IRM, and take proactive corrective measures immediately on a continuous basis.

- Monitoring department will prepare an early alert statement within 7 days of identification of investment account and issue to concern branches and to the IRM.

- IRG cell will update the IRG grade as soon as possible and no delay should be taken to refer the problem accounts to IRM.

- The relationship management will contact regularly to the customers for developing account status.

- Monitoring department will identify the investment accounts which are going to be classified within next 30 days report to the IRM and managing direction for the prompt action.

- Monitoring department shall closely monitor early alert identified accounts and contact regularly and the investment clients so that the accounts can be regularized.

Non-Performing Account Management

Management of non-performing accounts will be assigned to recovery unit who will be responsible for coordinating and administering action plan for recovery of NPL account. Recovery management to serve as the primary customer contact after the investment account is downgraded.

The IRM will assist recovery management to implement the appropriate strategies.

Transfer of Non-Performing Account to recovery department

An investment account downgraded as sub-standard will be transferred to the Recovery Management/ Recovery Management from the Monitoring Department along with a request for action (RFA) in format and a handover/downgrade checklist.

- The recovery department / recovery unit will review all documents, meet the customer and prepare a review report within 15 days of transfer.

- The initial review report should include documentation issues; investment structuring weakness, proposed workout strategy, security issues as per Instruction Circular no.INV/130 dated 08022005 regarding Eligible Securities and should seek approval for provisioning that is necessary.

- The recovery unit should ensure that the following is carried out when an account as sub standard or worse.

- a) Facilities are withdrawn or repayment is demanded as appropriate. Any drawings or advances should be restricted and only approved after careful scrutiny and approval from appropriate executives within IRM.

- b) CIB reporting is updated according to Bangladesh Bank guideline and the Investment Client’s Risk Grade is changed as appropriate.

- c) Loan loss provisions are taken based on Force Sale Value (FSV).

- d) Loans are rescheduled in conjunction with the Large Loan Rescheduling guideline of Bangladesh Bank. Any rescheduling should be based on projected future cash flows and should be strictly monitored.

- e) Prompt legal action is taken if the client is uncooperative.

The recovery department / unit will prepare a quarterly review report to update the status of the action / recovery plan review and access the adequacy of provisions and modify the bank’s strategy as appropriate.

Non performing Investment Provisioning policy

Bangladesh Bank issued BRPD Circular No. 05 on June 2005 under the caption “Master Circular-Loan Classification and Provision” with detail guideline for provisioning against classification investment. The circular is enclosed in annexure-16.

AIBL follow the Bangladesh Bank’s master circular and its subsequent amendments in provisioning against classified investment.

Investment recovery department will ensure the implementation of investment write off policy.

Non-performing write off policy

- Bangladesh Bank issued BRPD Circular No. 02 on January 13, 2003 under the caption “Loan Write off Policy” with detail guideline for classification.

- Bank will follow the Bangladesh Bank’s circular and its subsequent amendments in write off classified investment.

- Investment recovery department will ensure the implementation of investment write off policy.

Rescheduling Of Non-Performing Investment

Bangladesh Bank issued BRPD Circular No 01 on January 13, 2003 under the caption “Loan Rescheduling Policy” with detain guideline for rescheduling of classified investment. The circular is enclosed in annexure-18.

Bank will follow the Bangladesh Bank’s circular and its subsequent amendments in rescheduling of classified investment.

Investment recovery department will ensure the implementation of investment write off policy.

Recommendation

Al-Arafah Islami Bank Limited has lacking of branches all over the Bangladesh. For this reasons, customers have to visit long distance to continue their bank activities. They can open more branches that can attract more customers.

As we know ATM card is the modern innovation in banking industry. ATM helps to get money as soon as possible. Recently they opened only 8 ATM booths in Dkaha. That is not sufficient. AIBL should concentrate on ATM card.

- AIBL should concentrate in increasing its profit earning capacity.

- Bank should provide more foreign exchange and other sort of facilities to new customers, new entrepreneurs, new businessmen or new companies.

- Bank should increase their office space and take more care in interior decoration.

- Al-Arafah Islami Bank should promote introduce its Unique Selling Proposition, the Islamic Visa Card service in order to obtain better customer response.

- AIBL should give more emphasize on their marketing effort and try to their sales force.

- AIBL should try to attend different type of target customers.

- Bank should introduce training courses for their employee in order to develop human resource according to the Islami Bank Training & Research Academy.

- AIBL should carry out more promotional activities to make aware about their offers.

- AIBL is absent in TV, print media, bill boards and sponsorships. The bank should advertise about itself and its offers so that it can attract more customers that will increase the business volume of the bank.

Conclusion

The management of Al-Arafah Islami Bank Limited is quite confident that, with their competitive market strategy, high standard of customer service and loyal employees, they shall continue to successfully grow and increase their business and profit. Al-Arafah Islami Bank Limited continues to accelerate its business growth through existing and new relationships. Its business units will function within the confines of policies and procedures which are consistent with its underlying values and principals as a leading banking institution.

Al-Arafah Islami Bank Limited is a premier banking institution of the country. It integrates the latest technology into every facet of its operations. But recently there have been a problem with their online banking functions. The online banking system of Al-Arafah Islami Bank Limited is being upgraded into a world class system. But the temporary loss of the online function is hampering its image. Even then the development of the bank is going on according to its goal.

One thing that I come to know from the employee in Gulshan Branch there was no nonperforming loan till 2012. That means its creditor is so smart they can repay their loan. As it has less the amount of loan losses, the more the income will be from credit operations. The more the income from credit operation the more will be the profit of the Al-Arafah Islami Bank Limited. The Bangladeshi banking market is a highly competitive market. In our country the banking sector is growing up very rapidly. So every bank faces this stiff competitive situation. In this competitive market, Al-Arafah Islami Bank Limited has done better to earn quite a good amount of profit in the banking sector.