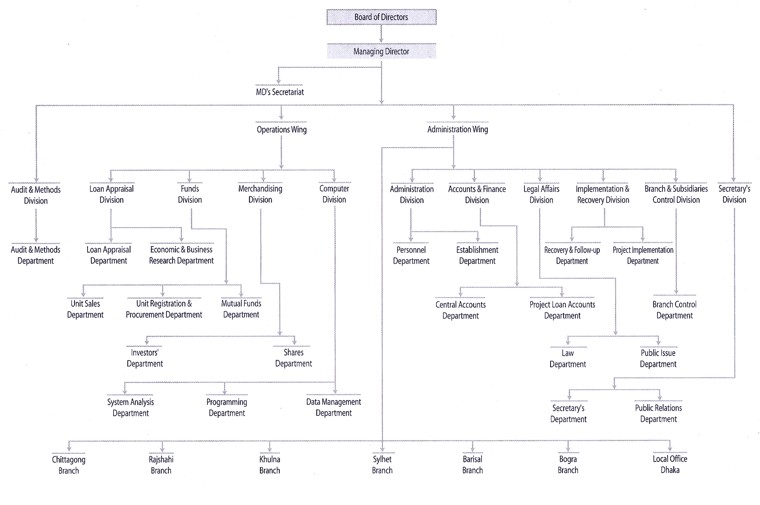

3.6. Organization Manpower:

The general direction and superintendence of corporation is created in a board of directors, which consists of clever (11) persons including the chairman and managing director of ICB. This is the most powerful board compare to other govt. financial institutions in terms of their experience and knowledge. The managing director is the chief executive of the organization. Two general managers assist him, viz. G.M. (Operation) and G.M. (Admin). Total manpower of ICB at present is 372, of which 241 were officers & 131 subordinate staff. As on 30 June 2005, the total numbers of female e4mployees were 54, including 43 officers, representing 14.52% of the total manpower.

3.7. Organogram of ICB:

4. FINANCIAL ASPECTS OF ICB

4.1. Capital Structure:

The particulars and capital structure of ICB are as follows-

(Tk. in Crore)

| Particulars | As on 30 June | Increase / decrease (Percentage,) | |

| 2005 | 2004 | ||

| Authorized Capital | 100.00 | 100.00 | |

| Paid-up Capital | 50.00 | 50.00 | – |

| Reserves | 84.11 | 69.11 | 21.70 |

| Retained Profit | 5.36 | 3.24 | 65.43 |

| Long-Term Govt. Loan | 5.25 | 5.25 | – |

| Debentures | 61.80 | 76.03 | -18.72 |

| Others | 24.89 | 27.40 | -9.16 |

| Total | 231.41 | 231.03 | 0.16 |

4.2. Shareholding Position:

The shareholding position as on 30 June 2005 was as follows –

| Serial No. | Shareholders | No. of shareholders | No. of shares | Percentage of shareholdings |

| 1. | Government of Bangladesh | 1 | 1350000 | 27.00 |

| 2. | Nationalized Commercial Banks | 4 | 1137220 | 22.74 |

| 3. | Development Financial Institutions | 2 | 681550 | 13.63 |

| 4. | Insurance corporations | 3 | 618286 | 12.37 |

| 5. | Bangladesh Bank | 1 | 600000 | 12.00 |

| 6. | Denationalized Private Commercial Banks | 2 | 454263 | 9.08 |

| 7. | Private Commercial Banks | 3 | 28286 | 0.57 |

| 8. | Foreign Commercial Banks | 2 | 26531 | 0.53 |

| 9. | First BSRS Mutual Fund | 1 | 6900 | 0.14 |

| 10. | Other Institutions | 9 | 26949 | 0.54 |

| 11. | General Public | 927 | 70015 | 1.40 |

| Total | 955 | 5000000 | 100.00 |

4.3. Share Price:

Share price of ICB varied from lowest Tk. 122.0 to highest Tk, 219.5 in the stock exchanges during the year. as on 30 June 2005, the market price of share was Tk. 200.0 and Tk. 201.25 in the DSE and CSE respectively. The price movements of ICB’s share on DSE are shown graphically in below:

4.4. Transfer of Shares:

The volume of shares transferred increased substantially during the year. 36269 shares were transferred during 2004-05 as against 16085 shares transferred in 2003-04 showing an increase of 125.48 percent.

4.5. Achievements of ICB during 2004-2005: (Tk. In Crore)

Particulars | Consolidated position | Growth (percentage) | |

| 2004-05 | 2003-04 | ||

| Income | 187.82 | 143.49 | 30.89 |

| Net profit | 31.68 | 21.68 | 46.13 |

| Earning per share (Tk.) | 63.36 | 46.41 | 36.52 |

| Return on Equity (%) | 20.91 | 16.94 | 23.44 |

| Net Asset Value (Tk.) | 305.65 | 279.17 | 9.49 |

| Value Added | 116.28 | 111.04 | 4.72 |

| Provisions made | 65.50 | 27.25 | 140.37 |

| Debt-Equity ratio | 30:70 | 38:62 | |

| Capital Adequacy ratio | 18.59 | 15.33 | 21.27 |

| Transaction of Securities: | 1065.63 | 1057.59 | 0.76 |

| Trustee to the issue of bonds: | |||

| No. of Companies | 4 | 1 | 300.00 |

| Amount | 104.86 | 30.00 | 249.53 |

| Trustee to the issue of debentures: | |||

| No. of companies | 5 | – | |

| Amount | 140.00 | – | |

| Recovery of loans & advances and others | 263.81 | 181.56 | 45.30 |

| Dividend performance (Tk): | |||

| ICB | 12.00 | 10.00 | 20.00 |

| ICB Capital Management Ltd. | 15.00 | 10.00 | 50.00 |

| ICB Asset Management Company Ltd. | 18.00 | 12.00 | 50.00 |

| ICB Securities Trading Company Ltd. | 30.00 | 25.00 | 20.00 |

| ICB Unit fund | 12.00 | 11.50 | 4.35 |

| First ICB Mutual Fund | 210.00 | 200.00 | 5.00 |

| Second ICB Mutual Fund | 55.00 | 50.00 | 10.00 |

| Third ICB Mutual Fund | 52.00 | 50.00 | 4.00 |

| Fourth ICB Mutual Fund | 48.00 | 45.00 | 6.67 |

| Fifth ICB Mutual Fund | 27.00 | 24.00 | 12.50 |

| Sixth ICB Mutual Fund | 18.50 | 17.50 | 5.71 |

| Seventh ICB Mutual Fund | 16.00 | 15.00 | 6.67 |

| Eighth ICB Mutual Fund | 15.00 | 14.00 | 7.14 |

| ICB AMCL First Mutual Fund | 16.00 | 12.00 | 33.33 |

| ICB AMCL Unit Fund | 12.00 | 10.00 | 20.00 |

| ICB AMCL Islamic Mutual Fund | 5.00 | – | |

| ISB AMCL Pension Holders’ Unit Fund | 9.00 | – | |

5.1. Capital Market of Bangladesh:

Capital market includes and refers to a number of institution and organizations whereby the suppliers of long-term fund make transactions. Included among these are transactions in the debt and equality issues of business houses as well as the debt instruments of Government agencies and similar other bodies. Participants in the capital markets include individuals, business house and the Government. Capital markets are immense importance to the long-term growth and prosperity of business and Government organizations as well as in the mobilization of savings and long-term investment in an economy,. It is capital markets, which help generate funds needed to acquire fixed assets and implement programmers aimed at ensuring an organization’s continued existence the backbone of the capital markets is the various security exchanges that provide the market for debt and equity transactions. Capital markets aid those segments of the economy that need capital to acquire plant and equipment to obtain funds from numerous savers in the economy. Just as financial intermediaries collect and mobilize savings from persons and parties in an economic society for advancing loans to acceptable borrowers, so too the capital markets permit the convention of savings into investment in today’s market economy. The capital markets permit individuals, business houses, government and financial institutions to channel their savings into long-term investments in the form of equates or long-term loans in business, government and financial institutions. The securities markets that make up the capital markets perform a number of important functions, such as allocating scarce capital, creating a continuous market, determining and publicizing security price and aiding in new financing. Thoughts on developing securities markets in Bangladesh came up immediately after the liberation through activating the “dormant” Dhaka Stock Exchange. Towards this a series of measures were taken from time to time. This will be obvious through a study of the growth of the country’s stock markets in retrospect.

5.2. Dhaka Stock Exchange:

Dhaka Stock Exchange, as we know it today, was incorporated as East Pakistan Stock Association Limited on 28th April, 1954. Subsequently it was renamed as east Pakistan Stock Exchange Ltd on 23rd June, 1962 and Dhaka Stock Exchange Ltd. on 14th May 1964. Through incorporated in 1954, the formal trading was started in 1956 at Narayangang. It was shifted to Dhaka and started full functioning at the Narayangang Chamber Building, Motijheel C/A, in 1958. The Dhaka Stock Exchange purchased a plot of land measuring 8.75 kathas at 9/F, Motijheel C/A, Dhaka in the year 1957 on 1st October, and constructed a building thereon and shifted the Stock Exchange to its own building in 1959. Prior to the emergence of Bangladesh that is, in the erstwhile East Pakistan, as at 1971 there were 190 companies with a total paid-up capital of Tk 4000.00 million listed on the Stock Exchange. After emergence of Bangladesh the operation of the Stock Exchange remained suspended till 1976. The Dhaka Stock Exchange is registered as a Public Limited Company with limited liabilities under company Act 1913 and Securities and Exchange Ordinance, 1969. The DSE is a self-regulatory body in the conduct of its own affairs empowered to deal in securities as per Securities and Exchange Ordinance 1969, Company Act 1994, and rules of Securities and Exchange Commission 1993. As on 30th June, 2000 there were 239 securities listed with DSE against which Total issued capital and debentures of all listed securities was Tk. 30517 million and Market capitalization of Tk. 54004 million as against Tk. 28684 million and Tk. 50748 million respectively on 30th June 1999. The DSE is a self regulated non-profit organization. At present there are 195 members. Membership is open for the foreigners also.

The objectives of the Dhaka stock Exchange is to provide the information towards establishment of securities market to be governed by just equitable principles of trade as well as to conduct the business in securities with due regards to the public interest and for the protection of investors. This is a non-profit organization and as such the income and property of the Exchange are supposed to be applied solely towards attainment of the objectives of the Exchange and no portion is paid or distributed to its member in the form of dividend or so.

5.3 Chittagong Stock Exchange:

The second stock exchange in the country was incorporated in the name of Chittagong Stock Exchange Limited as a public company under the Company Act, 194 on 1st April, 1995 and formal trading was started on 10th October, 1995. As on 30th June, 200 there were 163 securities listed with CSE and Market capitalization of all securities was Tk.44840 million which was Tk. 40950 million on 30th June, 1999. Total issued capital in CSE in FY 1999-2000 stood at Tk. 26655 million which was Tk. 24519 million in the 1998-1999. CSE is also a self-regulated non-profit organization with its own regulations.

5.4. Problems of Capital Market in Bangladesh:

There are many problems prevail in the capital market of Bangladesh. I would like to analyze the problems to the best of my knowledge which are given below:

5.4. A. General Problems:

- Lack of Confidence: Number one problem of our capital market is lack of confidence of investors. Because if the lose every thing in the market in 1996. In that time investors converged at the DSE and CSE but after a certain period market did not behave according to their exception.

- Liquidity: Liquidity also a problem for our capital market. We don’t liquidate our securities whenever we desire. There is a fear for liquidation that the share value may fall or we loose the capital.

- Good and new shares in the market: Blue chips are not available in the market for investment.

- Government initiative: There is also lacking for government initiative for floating blue chips share in the market Multinational companies share’s are lucrative to the investors. But the companies don’t float the share in the market. Berger paint, Unilever listed in the Mumbai Security Exchange. But this type of company is not listed in DSE. If such company is listed in DSE, I believe that it will help to accelerate the growth of the DSE transaction.

- Regularity Bodies: Regularity bodies also not concern take the action when companies do not executed the AGM or declared dividend.

- Transferent Management: Transferency in Management also absent for many companies. Sometime they show overestimated budget to get the loan and they don’t used they found or transfer the fund.

- Market Maker: There is no market maker in the capital market of Bangladesh those who ensure the buy and selling the securities at a specified rate.

- Lack of knowledge: Most of the educated people also ignore about the capital market or shares or debentures or other fiancé instrument. They don’t know how to transact with them.

- Policy: Just I want to mention the policy of government now listed companies of DSE enjoy 5% tax exemption. There is lacking of incentive to the companies that they will be more interest to the offering or listing themselves with DSE or CSE.

- . Infrastructure: There is also prevail infrastructure problem in Bangladesh. The financial system is not strong that a remote area doesn’t have investment opportunity, if he desire.

5.4. B. ICB Related Problems:

- 1. Bridge financing: ICB has stopped bridge financing from 1998. It has also a negative impact on the capital market. In this reason, new entrepreneur has also faced problem to called fund for investment.

- 2. Bureaucratic Problem: It is also a long term process to get permission for permission for issue, or set up a new industry. Such kinds of obstacle help the investors to reluctant from investment.

- 3. Sale of Unit Fund: Now ICB has stopped to issue new unit fund certificates to the public.

- 4. Issue of new Mutual Fund: There is no Mutual fund offer by ICB From 1996.

- 5. Investors Scheme: Now this scheme does not allow new investor to open new accounts. Only existing accounts holder can execute the transaction through their accounts, the flow of fund also declining day by day for this reason.

6.1. The Role of ICB in the Development of Capital Market of Bangladesh:

The development of capital market depends largely on financing deepening which, in turn hinges on elective financial intermediation as well as on the availability of wide array of financial instruments. Over the years, the Investment Corporation of Bangladesh (ICB) has actively & undyingly helped the capital market through effective intermediation as well as by creating supply of financial instruments in the form of marketable securities & by enthusing demand for such financial instrument.

6.1. A. Performance of ICB in Bangladesh:

The establishment of ICB was a major stem in a series of measures undertaken by the government to accelerate the pace of Industrialization and develop as well as organized and vibrant capital market in Bangladesh, particularly securities market. It caters to the need of institutional support to meet the equity gap of the industrial enterprise having public limited company status in view of national policy of increasing the rate of marginal savings and investment to foster self-reliant economy. ICB assumes an indispensable and far-reaching role. The following roles are playing ICB in our capital market:

i) Financial Assistance and portfolio Investment: ICB plays pivotal role to develop the country’s capital market. ICB as the National investment house was the lone organization to perform the activities by creating demand of securities, and on the other hand to ensure the supply of securities in the stock market.

- Private Placements.

- Custodian and Banker to the issues.

- Managers and Acquisitions.

- Corporate Financial Advice.

- Investment portfolio of ICB.

ii) Creating Investors Account: The Investors Scheme was introduced in 1977 with the objective of broadening the base of equity investment through mobilizing savings of small and medium size savers for investment in the securities market. In addition to Head Office, investment Accounts are also operated at the 7 branch offices of ICB located at Dhaka, Chittagong, Rajshahi, Khulna, Barisal, Sylhet, and Bogra. However in view of strategic changes in policy reform, 01 July 20002 ‘ICB capital Management Ltd.’ started opening and managing investment accounts. ICB will continue to provide services to its old accounts only.

Further steps were undertaken to enhance the quality and speedy service under the scheme like computerization of all activities and installation of merchandizing operation management software. This enables the management to offer better and quick service to the investors including instant supply of the financial statement, portfolio, balance of accounts, etc. Installation of telephone banking system in Investors’ Account enabling investors to collect information and operate their account over telephone was at the final stage of operations. Besides, installation Electronic display system of DSE online trading on the floor of ICB was in progress.

iii) Secondary Market Transactions: The total turnover in Dhaka Stock Exchange (DSE) in 2004-2005 was Tk. 3493.56 Crore compared to his total turnover of Tk. 4909.40 Crore in 2003-2004 showing a decrease by 28.84 percent. On the other hand, the volume of turnover increased from 108, 85, 37,180 securities in 2003-2004 to 124, 62, 72,000 securities in 2004-2005 showing an increase by 14.49 percent.

The total turnover in Chittagong Stock Exchange Ltd. in 2004-2005 was Tk. 1584.13 Crore compared to the total turnover of Tk. 1448.17 Crore in 2003-2004 showing an increase by 9.39 percent Similarly, the volume of turnover also increased from 46,12,20,000 securities in 2003-2004 to 67,08,39,940 securities in 2004-2005 showing an increase by 45.45 percent.

6.1. B. Other Roles:

Investment Corporation of Bangladesh is virtually the only investment Bank in country engaged in underwriting of public issue, management of Mutual Funds (Both open end and close end) and in opening investment accounts the corporation has completed about two decades of operations in fulfillment of its objects. During its long period of operations, the cooperation has a success story on the one hand and also has some failure on the other hand. In this part an attempt has been made to measure briefly the performance of ICB from its inception.

The Investment Corporation of Bangladesh has been successful in the creation of large investor class in the country thro ugh the launching of investors’ scheme. The scheme was introduced in 1977 with the objective of mobilizing savings and encouraging the full and medium investors to invest in the securities and thereby benefit from such investment, which would help develop capital market, industrialization and economic development. Over the last to decades it has been proved to be one of the schemes the ICB office inspires the investors to open and maintain investors’ account by knocking from door to door. But today, investors are coming spontaneously to open the account and participate in the purchase and sales of securities in the both primary and secondary market. Thus the operation of investor’s scheme creates demand for the securities and the companies find it easier to move-up capital by issue of securities because of the existence of large investor class. Here lies the success of ICB. A cumulative comparative operational position of investors Scheme is given in ensures.

At the beginning of its operation ICB worked mainly to develop the capital market. In order to assure the supply of securities in the capital market ICB provide underwriting and bridge financing facilities to the public limited company. Side by side, ICB worked to mobilize savings of small investors to create demand for securities in the market, to mobilize savings of small investors to create demand for securities in the market, to mobilize small investors savings ICB launched Investors scheme in 1977 through which investors were encourage investing their savings in the capital market. By providing margin loan at a low interest rate ICB succeed to make this schemer a success. From then on, to hunt for smaller investors’ savings, ICB gradually introduced its Eight Mutual Fund and developed its own portfolio. By now has achieved success in managing these portfolios, which is clear from the following picture of dividend declared.

The reason rate of dividend on ICB own portfolio is that initially all expenses of the funds used to be borne by ICB, for which dividend income and capital gain of ICB’s own portfolio was not sufficient to cope with the increased revenue expenditure presently all expenses of funds fee charged against the respective funds, which help ICB to provide a healthy return in the future to its shareholders.

ICB develops the entire individual portfolio by investing in shares, shares from secondary market and accepting right share if found viable. To invest in primary share and right shares, ICB goes for in-depth analysis of prospectus and offer documents sometimes overall position of the particular sector, to do this, ICB has to go for ratio analysis of the particular company. Considering all aspects, investment decision is taken. In case of secondary purchase, company’s performance and its present market price play a vital role. ICB keeps company wise update information at least for the past five years. Moreover DSE review DSE’s daily quotation also helps in taking daily sale or purchase decision for the portfolio. Presently ICB goes for direct equity participation for its portfolios. Presently ICB goes for direct equity participation for its portfolios which helps it to have securities.

6.2. Recent Development of Security Market:

Government will soon establish National Stock Exchange (NSE). It will be fully computerized and trading will be all over the country. It will augment the number of quality investors and transparency of the stock market. The depth, liquidity and professionalism will be increased. Another development is the approval of, Merchant Bank. It will strengthen the capital market more. Moreover, improve the liquidity and stability of the stock market in which ICB will have more impact to formulate the Capital Market too strong and developed.

7.1. Findings:

In case of ICB’s role in the capital market, I find out the following topics:

The securities segments of the capital market embraces the mechanism for bingeing securities to the public and providing for them to treated there in a manner that permits the establishments of fair and orderly prices. The intermediary between the originating issuer and the public buyers is usually the investment bankers who plays a major role in determining which effecting their distribution and underwriting the securities in the event is not a primary offering unless there is a reasonably liquid secondary market where indispensable adjunct of the primary market. The overall market mechanism specific mechanism must be geared to the social and economic environment to particular country involved.

Both demand for securities and supply of securities must be needed sufficiently in order to produce an effectively functioning security market. Creating demand for securities is only a part of the equation. There must be a body of companies that furnishes the offsetting supply of good securities to supply of securities is also pray of equation. There must absorb the demand that come to the market. On the other hand, creating investors that furnishes the offsetting demand to absorb the securities that come to the market.

The Investment Corporation of Bangladesh (ICB) has been successful in the creation of large investors’ class in the country though the lunching of investors’ Scheme. The Scheme was introduced in 1977 with the objectives of mobilizing savings and thereby benefits from such investments, which would help develop capital market, industrialization an economic development. Over the last decades it has been proved to be one of the most popular and successful investment schemes in the country. At the beginning of the scheme, the ICB officials inspire the investors to open and maintain investor’s account by knocking from door to door. But today, the purchase and sale of securities are in both primary and secondary market. Thus the operation of Investors’ Scheme creates demand for securities and the companies find it easier to mop-up capital issue of securities because of the creation the demand for securities. But it needs the support of sufficient supply of good securities.

Investors’ Scheme has close relation with the securities segment of the capital market. The target of this scheme is to mobilize small and medium savers fund and to make channel of these to the capital market. Through this activity this scheme had a great impact on the security market by creation demand for securities. So this scheme has a great impact on the security market. On the other hand, if number of saver will become interest to invest in this market and thus demand for securities through the scheme will be increased. The market will bad securities and price falling tendency can hamper the activities of investors’ scheme. in this scheme, deposit receive is the first stump of saving mobilization. Moreover, loan sanction and investment made against the Schemes is also very important tool for creating demand of securities, which ultimately strengthen the capital market.

It is revealed that ICB maintains investors’ accounts, flats and manages close-end, open-end mutual funds to ensure supply of securities as well as generate market. Despite unfavorable stock market condition for the last few years, the Corporation has declared attractive dividends on all of its mutual funds. The investor’s scheme of the Corporation provide the enquired impetus to capital market by creating class of investors who are oriented towards investing in corporate stock.

8.1 Financial Results:

The International Accounting Standards (IAS)-17 and IAS-27 have been adopted by the Institute of Chartered Accounts of Bangladesh (ICAB) in the recent past, which are related to Lease Financing and Consolidation of Accounts of Subsidiaries. The IAS-17 and IAS-27 have been followed while preparing accounts for 2004-05 along with other applicable rules as adopted in Bangladesh. For the purpose of comparison, the accounts for 2003-2004 has been restated after incorporating changes resulted from the adoption of IAS-17 relating to Lese Financing. As a result, net profit after tax for the year 2003-04 has been increased by Tk. 1.48 Crore, which has ultimately been transferred to retained profit of that year.

8.1. A. Total Income:

ICB earned a total income of Tk. 170.38 Crore in 2004-05 which was 24.05 per cent higher than that of Tk. 137.35 Crore earned in 2003-04. This is the highest level of income ICB has thus far earned. The major heads of income of ICB are interest income, capital gain, dividend income and income from fees and commissions. During 2004-05 income from all heads increased significantly except dividend income as compared to the previous year. Out of total income of Tk. 170.38 Crore, the income from capital gain was Tk. 70.53 Crore (41.4 per cent), followed by Tk. 67.88 Crore (39.84 per cent) from interest income, Tk. 20.67 Crore (12.13 per cent) from dividend and interest on debentures, Tk. 9.42 Crore (5.53 per cent) from fees and commissions and Tk. 1.88 Crore (1.1 per cent) from other sources. During the year under review, the highest level of income was from capital gains being Tk. 70.53 Crore, which was 66.93 per cent higher than the capital gains of previous year. Income from capital gains increased significantly because of up-trend of security market prevailing in 2004.05 Dividend incomes has decreased slightly compared to previous year because of declaration of stock dividend by a number of companies listed in stock exchanges.

8.1. B. Total Expenditure:

During 2004-05, total expenditure stood at Tk. 148.45 Crore compared to Tk. 119.21 Crore in 2003-04, showing an increase of 24.52 per cent. Interest expense stood at Tk. 70.18 Crore which was 80.98 Crore in the previous year showing a decrease of Tk. 10.8 Crore (13.34 per cent). Other operating expenses, except interest, were Tk. 12.54 Crore compared to Tk. 11.12 Crore in 2003-04, showing an increase of 12.77 per cent. In 2004-05, ICB made a substantial amount of provision against margin loan and investment in marketable securities. An amount of Tk. 65.73 Crore has been made as provision in 2004-05, against bad and doubtful debts and investments for strengthening the future financial base of the Corporation which was Tk. 27.11 Crore in 2003-04. With the provision made in 2004-05, ICB has been able to fulfill the required provision of project loan, margin loan and investments.

8.1. C. Net Income:

During 200405, ICB’s net profit after tax stood at Tk. 21.93 Crore compared to net profit of Tk. 18.14 Crore (Restated) earned in 2003-04, showing an increase of 20.91 per cent.

8.1. D. Dividend:

The Board of Directors of ICB recommended dividend at the rate of Tk. 12.0 per share for 2004-05. Tk. 10.0 per share was paid against the profit of the previous year.

8.1. E. Appropriation of Profit:

The Board of Directors of ICB recommended appropriation of profit of Tk. 21.93 Crore in the manner as stated below:

(Tk. in Crore)

Particulars | 2004-05 | 2003-04 |

| Dividend: 12.0 per cent (proposed)(2003-04: 10.0 per cent ) | 6.00 | 5.00 |

| General Reserve | 1.00 | 2.00 |

| Reserve for Building | 14.00 | 8.00 |

| Benevolent Fund | 0.30 | 0.15 |

| Retained Profit | 0.63 | 2.99 |

| Total | 21.93 | 18.14 |

8.1. F. Financial Analysis:

The overall financial position of ICB has improved during the year, compared to that in the previous year. Financial results of ICB’s own and those of consolidation of accounts with its subsidiaries and some key financial ratios relating to profitability liquidity and solvency are given below:

Particulars | ICB | Consolidated (ICB & Subsidiaries) | ||

2004-05 | 2003-04 | 2004-05 | 2003-04 | |

| Financial Results : | ||||

| Total income (Tk in Crore) | 170.38 | 137.35 | 187.82 | 143.49 |

| Total Expenses (Tk. in Core) | 87.72 | 92.10 | 86.29 | 93.83 |

| Profit Before Provision (Tk. in Crore) | 87.66 | 45.25 | 101.53 | 49.66 |

| Provision Made (Tk. in Crore) | 65.73 | 27.11 | 69.85 | 27.98 |

| Net Profit (Tk. in Crore) | 21.93 | 18.14 | 31.68 | 21.68 |

| Financial ratios: | ||||

| Net profit to total income (%) | 12.87 | 13.21 | 16.87 | 15.27 |

| Return on total investment (%) | 9.27 | 6.64 | 12.75 | 7.82 |

| Return on Equity (%) | 15.73 | 14.65 | 20.91 | 16.94 |

| Earning per share (Tk.) | 43.87 | 38.84 | 63.36 | 46.41 |

| Book Value per Share (Tk.) | 281.63 | 270.33 | 305.65 | 279.17 |

| Dividend yield (%) | 6.00 | 8.15 | – | – |

| Dividend payout Ratio (%) | 27.35 | 25.75 | 26.75 | 30.96 |

| Price Earning Ration (Time) | 4.56 | 3.16 | 2.16 | 2.64 |

| Current Ratio | 1.11:1 | 1.10:1 | 1.15:1 | 1.14:1 |

| Debt Equity Ratio | 32:68 | 39:61 | 30:70 | 38:62 |

8.2. Future Directions of the Corporation:

ICB is going to float two new Mutual Funds. ICB AMCL, a subsidiary of the state owned institutional investor, will launch and operate the funds. The Funds are:

I)ICB AMCL Pension Holder Unit Fund and

II)ICB AMCL Islamic Mutual Fund, each worth Tk. 10 Crore.

A great deal of planning effort of the corporation has been towards future IT structure and related operations. In the roadmap the following goals have been set:

- Establishing ICB firmly on IT industry not only as a consumer but also as a formidable IT solution provider especially in the financial sector.

- In the long run, ICB may consider establishing a separate business entity on IT, if found viable.

- ICB is considering going for starting full pledge activity in the field of IT area.

ICB is actively considering to provide web-based online services to its clients and to connect all its branches through WAN with head office. So that customers at any corner of the country can get instant services.

9.1. Conclusion:

ICB is a unique name in our country as an investment Bank. It has skill and experienced labor force and professional and dedicated management team that enable to pursue the ICB’s goals and objectives. ICB is helping to the industrial growth in our country by mobilizing the small savings from investors to the capital market. ICB should be concerned about its investors, because the investors are less risk takers. ICB has great influence in the capital market. ICB should play its important role for the gaining of the investors’ confidence on the capital market and further industrial growth in our country and the development and stabilization of the capital market in country.

To conclude this report it can be said that it was a great opportunity for me to study the operational activities of the biggest investment bank as well as merchant bank in Bangladesh. I have learned a lot about investment and the capital market of the country.

The Investment Corporation of Bangladesh (ICB) is virtually the only investment bank in Bangladesh. In a broader sense ICB is both Investment bank and Development Financial Institution (DFI). ICB plays a vital role to encourage and broaden the base of investments and thereby to help develop the capital market in Bangladesh.

The study is the first time for me to get the opportunity for conducting such and elaborate study in a different field. Hence, I do not know how far I am successful in writing this report. But it is true; I have tried sincerely to discharge my duties with zeal and enthusiasm and to the best of my satisfaction. However, I express my deepest regret for any error or omission which may have happened unwillingly.

9.2. Recommendations:

- To mobilize the savings of the small and medium investors, it is necessary to inform them through different media.

- Should prepare a booklet on rules and regulations of Capital Market, which will help investors to take proper steps.

- Should give percentage to the staff of the ICB who will bring investors.

- Should increase the activity in stock market.

- Many investors is now dissatisfied as the dividend payment ratio is decreasing. So, should try to increase the dividend payment ratio by keeping a strong portfolio.

- Officers dealing with the investors should give more attention and should behave well with them.

- The procedure to obtain Bank loan against Unit Certificate should be easy and should inform all investors about this opportunity.

- Should have the facility to make nominee of the Unit Certificate though it has the opportunity to buy Certificate in a Joint name.

- The corporation should have a training institute.

- Records, documents, paper of share department should be eliminated. Therefore, it must be computerized.

- The Central Depository System (CDS) is essential in ICB. It also needs Internal Transfer of Shares (ITS).

- The newly formed Business Development Cell contemplates to undertake the following additional functions:

i) Introduction of “Best Efforts” underwriting system whereby ICB will only sell a public issue without the obligation of take up.

ii) Management of portfolios of other institutions or funds for predetermined Fee or commission.

iii) Floatation of close-end Mutual Fund exclusively for the wage earners living abroad.

- Security is one of the reasons that investors interested to invest in the Capital Market. But it was found that some investors do not get their dividend properly. So, it should improve the dividend distribution policy.

- The corporation may redeem one or two mutual funds which are lease profitable in order to reduce the work load of the Mutual Fund Department or it can employ a few employees to address the same problem. Anyone of these steps may lead to more profitability of the funds.

- The corporation should place greater emphases on recovery of its dues or over dues from the projects financed by Unit Fund, unrealized dividend or interest on investment in securities along with the recovery of project loan.

- For project appraisal purpose ICB depends mainly on the appraisal report of the prime financier i.e. BSB or BSRS etc. They should scrutinize research and investigate the real features of the company.

- The ICB should posses a good team of technical personnel to carry out the appraisal task. At least the Corporation should appoint some expertise that has the ability to evaluate supplied appraisal report which are now lacking.

Some MOre Parts-