Electronic Fund Transfer-

Pioneered by Citibank N.A, Bangladesh

With a history that dates back to 1902, the Asia Pacific region is one of the most important for Citigroup globally. Citi’s deep presence in this region spans across 16 markets with more than 55,000 employees in its Regional Consumer Banking (Retail Banking, Local Consumer Banking and Cards) and Institutional Clients Group (Corporate & Investment Banking, Markets and Securities Services. Treasury and Trade Solutions and Private Banking businesses. Citi’s deep presence in Asia covers Australia, Bangladesh, China, Hongkong, India, Macau, New Zealand, South Korea, SriLanka, Taiwan, and the ASEAN countries- Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam. Citi has established a strong presence in Bangladesh. It now has four branches, four service outlets and employs more than 180 people. Citi’s clients in Bangladesh comprise both public and private sector institutions. Citi has a well-developed Financial Institutions business supporting the cross-border transactions of nationalized and private sector banks in the country. Citi Transaction Services supports Bangladesh corporate, financial customers and public sector clients with its award winning cash management, trade services, agency & trust, and direct custody & clearing solutions. The corporation is also the leading book runner of capital-market solutions for our clients in Bangladesh. Citi’s Corporate and Commercial Bank, services local corporate and multinationals across several industries, providing vital linkage and an integrated perspective throughout the Bangladesh supply chain and business operation. Citi’s presence in Bangladesh has been since 1987. At present, the multinational corporation has 4 branches located in Motijheel, Gulshan, Dhanmondi, Chittagong and 2 service centers in Dhaka EPZ & Chittagong EPZ. The bank has a full spectrum of Corporate, Treasury, Investment and Cash Management Solutions. Citi Bangladesh has been a pioneer in:

-Structured Cash Management

-Payments Products (Managers Checks/Demand Draft)

-Transaction initiation from Internet Banking Platform

The financial institution has also been the Banker of Choice for Treasury & Trade Solutions across major industries like Telecom, FMCG, Oil & Gas, Pharmaceutical, Insurance & other local corporate. Citi was awarded the Best Corporate/Institutional Internet Bank in Bangladesh by ‘Global Finance’ for 7 consecutive years since 2008.

Citi has led the way in Bangladesh with its innovative landmark solutions. With the introduction of several ‘first-ever’ deals in Bangladesh, Citi has helped to further develop Bangladesh’s financial market. Some of Citi’s landmark achievements include:

- Citibank, N.A. Bangladesh was selected as the Sole Independent Advisor to the Government of Bangladesh for sovereign rating advisory.

- Citi Bangladesh arranged the world’s first AAA-rated micro-credit securitization transaction for US$180 MM for BRAC, the largest NGO in the world.

- Citibank Bangladesh successfully arranged the country’s largest-ever local currency amortizing senior secured bond offering of BDT 7, 070 million.

- Citi was the exclusive financial advisor, sole private placement agent, sole initial public offering (IPO) issue manager, lead IPO underwriter, main banker to the issue and escrow agent for the largest IPO and pre-IPO placement in Bangladesh for US$141 million for Grameenphone Ltd.

- Citibank, N.A. Bangladesh has successfully arranged the country’s first-ever syndicated agricultural term financing facility of BDT 1,500 million.

- Citi was the sole placement agent for the country’s first unsecured, non-convertible, subordinated Tier-II Bond issue of BDT 2,500 million by Prime Bank Ltd.

Objective of the Report

- Comprising working experiences of internship in a report

- Analyzing Electronic payment scenario of Citibank N A Bangladesh

- Describing the EFT system of Citibank N A Bangladesh

- Stating the pros of EFT & cons of traditional systems

- Findings feasible solutions to clients

Data Sources:

Primary sources:

Major Source of primary information was gained by actually working in the position of Intern at Citibank N.A Bangladesh.

Secondary sources:

Documents collected from Citibank N.A’s official website and articles published on Citibank N.A along with other authentic websites.

Scope of the report

The report is based on the Electronic Funds Transfer Network of Citibank N.A Bangladesh and the main purpose of this report is to enlighten on what is EFT, how does it work, what benefits it will bring, initiatives taken and progress etc. Apart from this there would be a brief discussion on the other activities which I had to carry out within the department. All relevant units are described in the report. This report is a mirror reflection of my observation which covers the real essence of the cash management teams operation in a global bank like Citibank N A Bangladesh.

Organization Overview

History:

Citigroup’s history dates back to the founding of Citibank in 1812. Citigroup’s original corporate predecessor was incorporated in 1988 under the laws of the State of Delaware. In 1811 the U.S. Congress refused to renew the charter of the First Bank of the United States, the country’s central bank, which had branches in such cities as New York. Thus on June 16, 1812, some of the First Bank’s New York shareholders and other investors secured state incorporation of the City Bank of New York, which was later established in the branch banking rooms of the old First Bank.

The bank grew as New York City became the nation’s commercial and financial capital, and in 1865 it was chartered under the National Bank Act and renamed the National City Bank of New York. In 1897 it became the first large American bank to open a foreign department, and in 1915 it became America’s leading international bank upon the purchase of International Banking Corporation(founded 1902), which had 21 overseas offices in 13 countries and territories.

Citibank was formerly (1967–74) known as First National City Corporation, American holding company incorporated in 1967, with the City Bank of New York, National Association (a bank tracing to 1812), as its principal subsidiary. The latter’s name changed successively to First National City Bank in 1968 and to Citibank, N.A. (i.e., National Association), in 1976. Citicorp was the holding company’s popular and trade name from its inception but became the legal name only in 1974.

Following a series of transactions over a number of years, Citigroup Inc, was formed in 1998 upon the merger of Citicorp and Travelers Group Inc. Citigroup is a global diversified financial services holding company, whose businesses provide consumers, corporations, governments and institutions with a broad range of financial products and services, including consumer banking and credit, corporate and investment banking, securities brokerage, transaction services and wealth management. In 1812, Citi had a capital of US$ 2,000,000, 22 employees and operated only in 1 country having a single branch. After 200 years of operations, Citi in 2012 having exceeded a capital of US$ 1,913,902,000,000, employees over 260,000 and operating in 117 countries with 4,598 branches. Citigroup currently operates, for management reporting purposes, via two primary business segments: Citicorp, consisting of Citi’s Global Consumer Banking businesses and Institutional Clients Group, and Citi Holdings, consisting of businesses and portfolios of assets that Citigroup has determined are not central to its core Citicorp business.

Citibank N.A. commenced its journey in Bangladesh during 1987, with the opening of a representative office. The Bank opened its first full-fletched branch in Dhaka, on 24th June 1995. During the last 19 years through dimensional services Citi has become one of the major international banks in Bangladesh.

Service Offering

The bank is structured according to the four product divisions: Corporate Banking, Financial Institutions, Cash Management and Treasury. There are also four other departments that can be termed as support and these are Operations, Credit Administration, Financial Control and Human Resource.

Corporate Banking

Corporate Banking in Citibank is divided into two main segments:

GRB (Global Relationship Banking): Relationship Managers basically deal with the clients (multinational companies operating in Bangladesh) with whom Citibank has global relationship.

There is a single Parent Account Manager (PAM) in the country of origin of that MNC who is responsible for looking into the credit relationship between Citibank and the company worldwide. Any credit extended to the company has to be approved by the PAM. TTLC (Top Tier Local Corporate), as the name suggests is the segment in which only the top performers (basically the first three ranked companies) of any industry approaches to be Citibank’s clients.

Citibank provides both deposit products and loan products to its corporate clients. The loan products are of varying tenor and purpose. Citibank N.A. Bangladesh also provides structured finance products.

The main activities involved in Corporate Banking division of the bank include: communication with customers and calls. The Relationship Managers (RM’s) try to establish contact with key CBG customers; know about the status of their capabilities. The next step is to collect customer information and make a detailed analysis of the needs of the client matched with what the bank can offer. After agreement of both parties, the bank gets approval from the lending unit. Once companies have become a client with credit relationship, the RMs then have to monitor the performance of the company and ensure that no complexity of credit occurs.

Financial Institutions

The Financial Institutions department caters for the need of various banks and non-bank financial institutions as well as NGOs, not-for-profit organizations and diplomatic missions. The core product is the correspondent banking services. Besides there are various electronic banking services, which enable FI, clients perform large domestic and international transactions efficiently and safely. FI department mainly facilitates international trade conducted by Citibank N.A., Bangladesh. Citibank does L/C advising, confirming, transferring, guarantying and negotiating and reimbursing. In order to do so the FI department of the bank provides the local banks direct facilities or credit lines that includes OSTBT (Ordinary Short-term Banking Transaction), Local bill discounting, CTC credit line etc. Credit line for treasury purpose includes PSR facilities. Like the CBG Department, the FI-RMs also try to establish contact with FI customers. After that, the RMs collects customer information and make a detailed analysis of the needs of the client matched with what the bank can offer. After agreement of both parties, the bank gets approval from the lending unit.

Project Summary:

In this part of the report, I would elaborate the whole process of Bangladesh Electronic Funds Transfer Network, participants in BEFTN and how the Electronic Funds Transfer Network of Citi operates. This section would basically include the learning which I had acquired while organizing the two up-country roadshow in Comilla & Mymensingh regarding Electronic payment. In addition to it, I had discussed the pros of electronic funds transfer and cons of traditional instruments, stakeholders associated with the electronic funds transfer process and the benefits they will have from the new technology. Limitations faced by Citi and suggested some recommendations based upon my observation and understanding on EFT.

Objectives of the Project:

Broad Objectives:

The main objective of the project is to give an overall idea of how EFT system works and the initiatives Citibank has taken to make its clients aware of this advanced technology.

Specific objectives:

- Introduction of EFT- a step for moving towards Real time Gross Settlement (RTGS)

- Places where the roadshow has been conducted/to be conducted

- Representing the benefits of EFT and limitations of old instruments

- Process flow of the EFT system and members associated

- Optimal recommendations through which Citi can make imperative changes

Methodology:

Primary Sources:

- Working side by side with project team members and observing them

- Attending the two up-country roadshows in Comilla & Mymensingh

- Different types of job responsibilities during internship period

- Face-to-Face interview and discussion with several line-managers

- Intranet of Citibank N.A

- TTS University- where managers elaborated the techniques and processes involved

Secondary Sources:

- Articles, journals, reports published on electronic funds transfer

- Pulling together resources from various authenticated websites

- Official website of Citibank N.A

- Previously published reports by other institutions

About Bangladesh Electronic Funds Transfer Network (BEFTN):

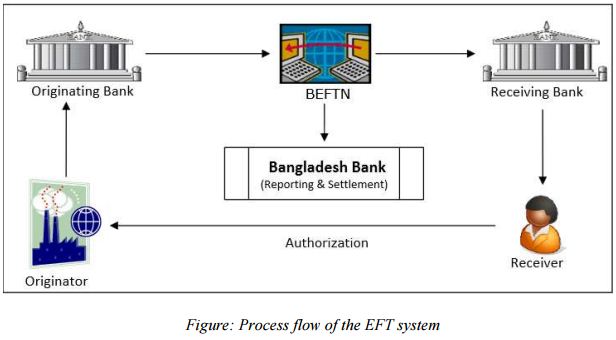

The Bangladesh Electronic Funds Transfer Network (BEFTN) functions as a processing and delivery centre providing support to the distribution and settlement of electronic credit and debit instruments among all participating banks. The Network operates in a real-time mode and for this the transaction files received from the banks during the day are processed as they are received to ensure the banking company gets a sufficient time to fix errors and resubmit the file if incase the file gets rejected for any reason. Final settlements of each bank take place using accounts that are maintained with the Central bank.

Participating banks with their own EFT Network and Bangladesh Electronic Funds Transfer Network (BEFTN) are interconnected through communication links. The use of electronic network facilitates the transfer of payments information faster, safer and in a more efficient manner of inter-bank clearing than existing paper-based mode. The Bangladesh Electronic Funds Transfer Network (BEFTN) offers a wide range of electronic products that improve payment services for the participating banks’ clients. BEFTN has been live from February 28, 2011 and Citibank was one of the first to initiate transaction using EFT.

Participants in BEFTN:

The participants involved in the network are:

a) Originator

b) Originating Bank (OB)

c) Bangladesh Electronic Funds Transfer Network (EFT Operator)

d) Receiving bank (RB)

e) Receiver

f) Corresponding Bank

Descriptions of Participants:

(a) Originator: The originator is the person or organization that agrees to initiate EFT into the network according to an agreement with a receiver. The originator is usually a company, government agency or an individual directing a transfer of funds to or from a consumer’s account or a company’s account. The originator initiates an EFT fund transfer entry through an Originating Bank (OB).

(b) Originating Bank (OB): The originating bank is the bank which gets payment instructions from its clients (the originator) and forwards the entry to the BEFTN. A bank can participate in the EFT system as a receiving bank without acting as an originating bank; however, if a bank decides to originate EFT entries, it must also agree to act as a receiving bank.

(c) Bangladesh Electronic Funds Transfer Network (BEFTN): This central clearing system is operated by Bangladesh Bank that receives entries from Originating Bank and distributes the entries to the appropriate Receiving Bank, and thus facilitates the settlement functions for the participating banks.

(d) Receiving Bank (RB): The receiving bank is the bank that receives EFT entries from BEFTN and posts the entries to the account of its depositors (receivers).

(e) Receiver: A receiver is a person or organization who has authorized an Originator to transfer/transmit an EFT entry to the account of the receiver maintained with the Receiving Bank (RB).

(f) Correspondent Bank: In some cases an Originator, Originating Bank or Receiving Bank may choose to use the services of a Correspondent Bank for all or part of the process of handling EFT entries. All Correspondent Banks must be approved by Bangladesh Bank before a bank enters into an agreement with the Correspondent Bank. Citibank N.A uses the services of Correspondent Bank’s since they only have four branches operating in Bangladesh.

Note: A written agreement must be signed between the receiver and the originator to allow payments processed through the EFT network to be deposited in or withdrawn from his/her account at a bank.

The Originator and the Originator’s Bank determine by agreement that how the information will be delivered from the originator to the Originating Bank. Typically, the originator or its bank would format the data in accordance with the BEFTN prescribed format and transmit the information to the originating bank through a communication channel. In case if a Receiver and the Originator both have accounts at the same bank then the transactions needs not to be transferred through the BEFTN but instead simply retained by the bank and posted to the designated accounts.

The BEFTN will sort the entries by Receiving Bank routing number which is unique for each and every bank branches and transfer the information to the appropriate receiving bank.

Flow of EFT Transaction (EFT Credit/EFT Debit):

Unlike a check, which is always a debit instrument, an Electronic Fund Transfer entry can either be a debit or credit entry. By looking on the receivers account, one can understand the difference between an EFT Debit and EFT Credit transaction. For example: If a receivers account is debited them there has been an EFT Debit entry and if a receivers account is credited then there has been an EFT Credit entry. On the other hand, an EFT Debit entry in a receivers account is a credit to the originators account and an EFT Credit entry in receivers account is a debit to the originators account.

EFT Credits (Pushing Funds):

EFT credit entries takes place when an Originator initiates a transfer of funds from his/her account to a Receiver’s account. For example: when a corporate uses a bank to disburse/pay salaries to its employees every month or when a distributor transfers funds from goods sold from his/her account to a corporate for which it works for. The originator originates the payment through the originating bank to transfer the money into the account of the receiver. EFT credit transactions include both consumer and corporate payments with distinct guidelines for each.

The most common type of consumer EFT application is Direct Deposit of salary. Other common credit applications are: Vendor Payments, Dividend Payments, Interest Payments and Government tax payments.

Since Citibank does not have any consumer banking operations in Bangladesh, they provide EFT credit services to its corporate clients.

Example of EFT Credit relating to Citibank N.A:

Suppose “A” is a client of IFIC Bank and Citibank N.A. “A” has a distributor in Mymensingh named “X Enterprise” who after the sale of goods sends back payments to “A”. So, the originator here in this scenario is “X Enterprise” and the Receiver is “A”, while the originating bank is IFIC and the Receiving Bank is Citibank N.A. Now let’s assume “X Enterprise” wants to initiate an EFT credit to make payments to “A”. So, “X Enterprise” originates the payment through the originating bank (IFIC Bank) to transfer the money which passes through the BEFTN to Citibank N.A which Citibank N.A then credits to the account of “A”. The whole process of EFT Credit is illustrated below:

As according to the example mentioned above, the following participants of the EFT Credit are:

a) Originator: X Enterprise, Mymensingh (Originator’s account Debited)

b) Originating Bank: IFIC Bank, Mymensingh

c) BEFTN Network- maintained by Bangladesh Bank

d) Receiving Bank- Citibank N.A, Dhaka

e) Receiver: A (Receiver’s account Credited)

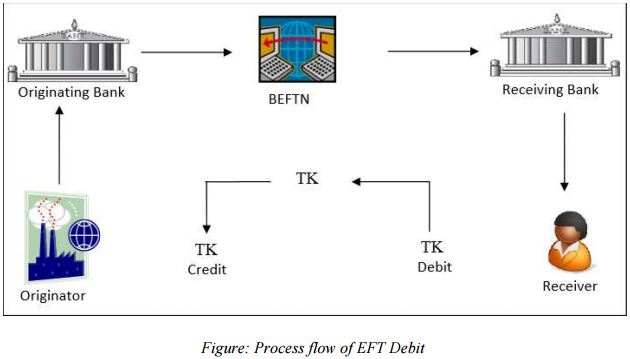

EFT Debit (Pooling Funds):

EFT Debit is simply the opposite of EFT Credit. EFT Debit takes place when funds are collected or pooled from the Receiver’s account and transferred to the originators account even though the originator initiates the entry. For example: When a corporate uses a bank to pool funds from a receiver. The corporate originates the payment through the originating bank to pool the money from the receiver’s account into its own account. Some of the common uses of EFT Debit are: Utility bill payments, Installments, Mortgage Payments and Insurance Premiums.

Example of EFT Debit relating to Citibank N.A:

Suppose Corporate “A” has an account with Citibank N.A for paying of electricity bills to DESCO. So, the Originator here is DESCO and the Receiver is corporate “A” while the Receiving bank is Citibank N.A and the Originating Bank is Sonali Bank. Now let’s assume Desco wants to collect electricity bill from Corporate “A”. So, Desco as an originator originates the collection through the originating bank (Sonali Bank) to pool the money through the BEFTN which passes from the Receiver’s account with Citibank N.A and thus Citibank N.A debits the receiver’s account. The whole process of EFT Debit is illustrated below:

As according to the example mentioned above, the following participants of the EFT Debit are:

a) Originator: DESCO (Originator’s account Credited)

b) Originating Bank: Sonali Bank

c) BEFTN Network- maintained by Bangladesh Bank

d) Receiving Bank- Citibank N.A, Dhaka

e) Receiver: A (Receiver’s account Debited)

Advantages of EFT to stakeholders:

Advantages to Distributors:

1) Utilize bank’s Internet Banking System

2) Avoid physical hassles of going to the bank

3) Shorter waiting queue for EFT

4) EFT keeps you ahead of competition once RTGS is launched

5) Able to use any EFT enabled bank, no need to find designated correspondent bank

6) Faster release of goods

7) No cost incurred by Distributor

Advantages to Sending Banks:

1) Option to save branch space and human resource (since clients are no longer using checks/pay orders/Demand Drafts), increased straight through processing rate and reduced processing time.

2) Lower chances of error during data entry by bank officials (due to unique routing code of each bank branch)

3) Less Paperwork and no deposit slips for EFT

4) Minimum chances of fraud

5) Avoids clearing processes of returning/honoring

Advantages to Client:

1) Faster fund realization

2) Able to utilize cleared funds

3) Greater visibility on information through BEFTN system

4) No need to rely on third party information to know the status of fund, minimum fraud possibility

5) Elimination of Paper at client end

6) No cost incurred by the dealer , hence no question of reimbursement

7) Any bank in any location can be used

Advantages to Receiving Banks:

1) Elimination of paper based processes in handling checks

2) Elimination of additional time-bound activities involved in return process

3) Faster fund receipt compared to checks and pay-order, especially from remote locations

4) Guaranteed funding once the transaction hits Bangladesh Bank system. Bank can provide early alert to client for incoming funds.

5) Automated MIS and reports for clients- no manual MIS dependency.

Economic Benefits:

1) No Paper

2) No queue

3) No extra charge

4) Deeper market penetration as Citi can serve remote areas

5) Greater economic activity

6) Efficiency in Banks and client centers

7) More money in Banking channel

8) Up scaling to international standards

Limitations of Current Bangladesh Electronic Fund Transfer Network:

(1) Inconsistency in information provided in EFT transactions by different banks: It is mandatory to provide some information while initiating EFT. At Citi, I often noticed my line managers receiving complaints from clients due to some inconvenience which occurred in between banks while providing information in EFT transactions. These are the mandatory information which one must provide:

- a) Beneficiary Account Number

- b) Beneficiary Name

- c) Beneficiary Account type

- d) Beneficiary Banks Routing Number: (e.g: Citibank N.A, Motijheel routing number is 075270007)

- e) Transaction Amount

Any wrong input of the above criteria’s will result in failure of appropriate transaction.

(2) Settlement issue: Settlement is made by Bangladesh Bank on the next day at 10am.

Thus, inefficiency remains.

Future Initiatives:

Bangladesh Bank has proposed to make Real-time Gross Settlement (RTGS) live within the first quarter of 2016. Citi being a front runner in the electronic payment landscape has already visited Reserve Bank of India to understand, design and develop an effective business model for RTGS system and relevant legal and regulatory framework. Moreover, Citi has already started their discussion with stakeholders regarding RTGS through their nation-wide roadshow in Bangladesh. Real time Gross Settlement (RTGS) is a funds transfer system that provides continuous intra-day settlements for individual transfers. It takes place in real time. Once it is activated, it will limit payment system risks, credit risk, systematic risk, reduce settlement risk in forex and securities market. On the top of it, RTGS will save clients time and provide better fund management. It will reduce clearing cost (administrative cost like printing) and most importantly reduce fraud as well as increase efficiency and productivity.

Recommendations:

(1) Banks are yet to fully embrace the electronic fund transfer (EFT) services even four years after its launch due to the lack of awareness among bankers about the cost effective, quicker and secure system. Only 5% of all bank transactions are cleared through the electronic system while the rest are still being done using the traditional paper based system. Citi fails to reach customers who want to initiate EFT but cannot due to the lack of infrastructure in the corresponding bank branches (mostly in remote areas) and for this reason the customers are bound to use the existing inefficient instruments like checks, pay-orders and demand drafts. Thus, all banks in their every branch need to provide full fledged internet banking facility to allow clients to initiate EFT transactions.

(2) Major branches of banks in major locations need to be connected with PBM server (maintained by BBK) to facilitate information flow.

(3) Banks need to pass the transactions into the PBM server within certain cutoff from receiving an instruction.

(4) All banks should use a consistent and uniform format as prescribed by Bangladesh Bank while sending ant EFT transactions. Moreover, BEFTN operating standards should be adhered with strict compliance such that entire industry can speak the same language.

(5) Charges and fees should be eliminated from the system as per the directives of Bangladesh Bank. There are some banks who are charging their clients for EFT initiation which is completely against the rules of Bangladesh Bank. This illegal activity must be monitored and restricted by the Central Bank or else customers will not use EFT.

(6) Citibank N.A must establish new branches outside Dhaka and Chittagong in order to minimize dependency on corresponding banks. There will be conflicts and disagreements between banks and the ideal way to avoid this is to set up own branches.

(7) Needs to start operating in the retail banking sector to maximize market share. By operating in the retail banking sector, Citibank will be able to capture even a greater share of the financial resources like HSBC and Standard Chartered Bank (SCB). If they do not intervene into the local market soon, competing with already established multinational giants and local banks will become difficult and hard to survive.

Conclusion:

Citi Bangladesh has been a front runner in promoting Electronic Funds Transfer to its clients and their payers since the inception of the system. Currently, it processes approximately BDT 260 Crore of payment through EFT every month and receives BDT 240 Crore of incoming EFT in favor of its clients. All such payments are part of the business to business cycle of the economy and contribute directly towards faster fund realization and release of goods. Citi has already conducted three workshops regarding electronic payment in Dhaka, Comilla and Mymensingh and plans to conduct two more in the country’s major collection and payment centers to raise awareness and to influence clients across the country and distinct level branches of banks to perform their financial transactions through electronic mode. With these initiatives Citi hopes to stimulate further utilization of the EFT system across the country in conjunction with the digital initiatives of Bangladesh Bank. The global giant has been the pioneer in EFT landscape and with its award winning online banking platform ‘Citidirect’ and expertise in EFT payments; Citibank N.A provides the best solution in the BEFTN landscape of Bangladesh. While a leader leads others follow and that is what Citibank has shown to other banks in Bangladesh. I believe, Citibank N.A will continue its trend of being one of the leading MNCs in Bangladesh by continuously driving its growth year after year.